Andrew Burton

Market players were treated to a rough 2022 with war, soaring inflation, and aggressive rate hikes turning the previous trends on their heads. The S&P500 (SP500) heads for 2023 with a loss of around 18.6%. Despite a slowdown in the pace of Federal Reserve rate hikes, I believe the stock market has further to drop, and will outline my reasons in this article.

BlackRock warns investors of mispriced recession risk

BlackRock (BLK), the world’s largest asset manager, sent a stark warning to investors recently that the Federal Reserve won’t “ride to the rescue” in 2023, and that equity valuations “don’t yet reflect the damage ahead.”

Investors should have already realized that with the misguided expectations for a Fed “pivot” that were recently shot down by Chairman Jerome Powell. Powell stated that although the pace of interest rate hikes may slow, borrowing rates will remain “higher for longer”.

Investors should apply some investment psychology to this scenario and realize that central banks were already under fire for missing the inflationary surge and having to commit to a sharp U-turn. There was a very small chance that policymakers would then make another abrupt reversal, especially if it led to a further jump in inflation. Central bankers were facing chaos and hiked rates to slam the brakes on inflation. The economy was an afterthought, and it also had another silver lining for the Fed- it popped the valuation bubble in stocks and removed any criticism that they were fostering exuberance in the stock market.

“History cautions strongly against prematurely loosening policy,” Powell said. Despite the slower pace of rate hikes, there may be no respite for stocks, as Blackrock said in its 2023 global outlook report:

“Recession is foretold as central banks race to try to tame inflation. It’s the opposite of past recessions. Central bankers won’t ride to the rescue when growth slows in this new regime, contrary to what investors have come to expect. Equity valuations don’t yet reflect the damage ahead.”

“We don’t think equities are fully priced for recession,” the report added. “Corporate earnings expectations have yet to fully reflect even a modest recession. This keeps us tactically underweight developed market equities.”

Two analysts at Goldman Sachs said late last month that their model implies a 39% probability of a US growth slowdown in the next 12 months, while risk assets were only pricing in an 11% chance.

Corporate profits showed strength despite runaway inflation in 2022, but they’re expected to get hurt next year as margin pressure grows, and weaker demand increases the risk of stagflation.

China is the real pivot that investors should consider

If investors are looking for a pivot in 2023 then China is where they should look. The country has been caught up in economic turmoil due to the government’s Zero-COVID policy, but investors are prepared for an end. The Chinese stock market has rallied recently and is shrugging off another surge in cases.

In its China 2023 Outlook, Goldman Sachs said:

“After a very challenging 2022, Goldman Sachs Research economists expect China GDP growth to accelerate from 3.0% this year to 4.5% next year on the back of China’s potential exit from its zero-Covid policy, which they assume will start shortly after the ‘Two Sessions’ in March.”

Chinese stocks underperformed in 2022 with the MSCI China Index losing 26%, compared to a decline of 19% drop for the MSCI all-country index. However, the iShares MSCI Emerging Markets ex-China ETF attracted a record $577 million in November, one month after President Xi Jinping secured another term at the Party Congress.

That trend has the potential to continue in the new year as developed economies head for recession and Asian central banks, such as Japan and China, continue to chart a path of stimulus and support.

In 2023, money could start shifting back to China and the trend would be exacerbated by a peak in the U.S. dollar. Recent sharp losses in the dollar followed the Federal Reserve’s decision to slow the path of rates and the greenback has been sliding against other major pairs. That could force overseas investors to cash out their U.S. stocks on currency concerns and bring them back to Asian markets.

A closer look at corporate earnings in 2023

Estimates have continued to drop for S&P 500 fourth-quarter 2022 earnings and are expected to decline 1.1% year-on-year, which would mark the first quarterly earnings drop since Q3 2020, according to Refinitiv.

Morgan Stanley Chief stock strategist, Mike Wilson, thinks earnings are 20% overvalued, but predicts that a first-quarter move lower will provide a strong buying opportunity.

The 12-month forward earnings per share estimate on the S&P 500 was recently $235.34 which is 7% above the full-year 2022 forecast of $219.38. Analysts may be pricing in earnings that are unrealistic and do not account for any Ukraine-related market shocks, or similar events. In the latest batch of third-quarter earnings, companies have been vocal about margin pressures, with wages and stubborn commodity prices being a headwind.

Fitch has predicted U.S. GDP will be 0.9% in 2023, down from 1.6%, but the constantly downgraded forecasts over the last year from various sources give rise to caution.

If the U.S. dollar does start to decline, it will add support to corporate earnings, but reduce purchasing power abroad and hurt GDP.

My price prediction for the S&P500 and thesis risk

I agree that the market rally in recent months is optimistic. The Federal Reserve showed that the pivot idea is misguided, and corporations will be left to market forces in the near term.

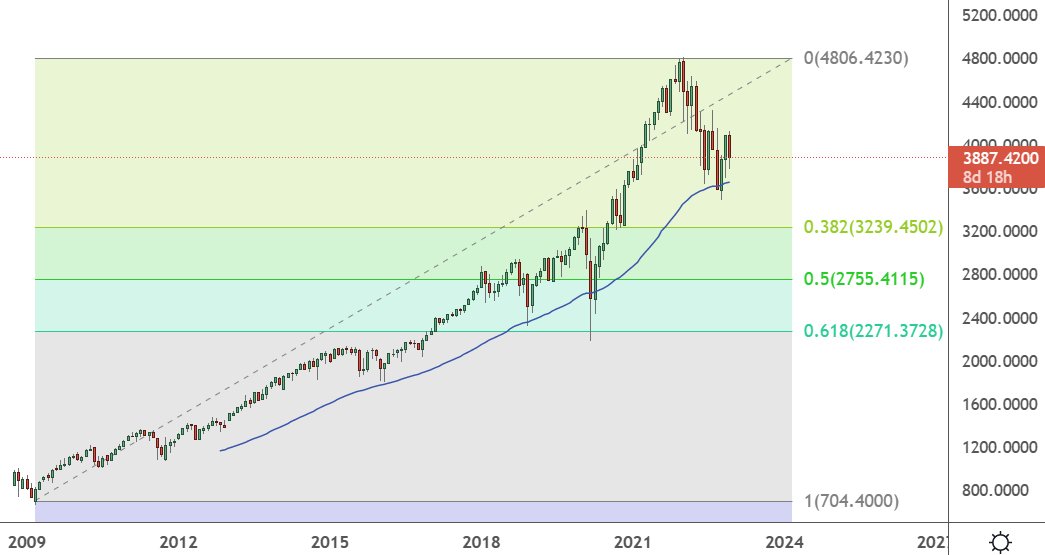

If we look at the S&P500 from the lows of 2009 with Fibonacci levels, we can see that even a 38% pullback in the index would bring the market to 3,200. The real support would be at the 2,270 or 2,755 levels and that would still mark a technical correction.

SP500 (M) (Trading View)

My price prediction for the S&P500 is a dump towards the 2,500-2,800 technical levels in the first half of the year. Following that, a rally could repair some of the damage and the 2023 closing could be around 3,600.

The risk to the bearish thesis would come from the Ukraine and Russia situation. If the tensions escalate then Europe would find itself in the crosshairs and investment capital could flee the Euro area.

Conclusion

The stock market was turned on its head in 2022 as long-held assumptions and trends were brought to an abrupt halt. Pandemic-related inflation met with the Ukraine war and sharp commodity price increases and central banks turned aggressively hawkish. The valuation bubble has popped and now there are warnings that corporate earnings are still being inflated, while a decline in the U.S. dollar could hurt overseas investment. Another push lower is possible in the S&P500 which would provide a good buying opportunity in the right companies and a second-half rebound would then be possible.

This article was submitted as part of Seeking Alpha’s 2023 Market Prediction contest. Do you have a conviction view for the S&P 500 next year? If so, click here to find out more and submit your article today!

Be the first to comment