24K-Production

The end of 2021 had bittersweet aspects. On the one hand, it was the year of a lifetime for me as an investor. Up 50%, as discussed here, and I’m not investing mainly in growth stocks.

On the other hand, nearly all my REITs seemed more or less fully valued. And while the surge in energy investments had contributed to my gains in 2021, it was unclear how much further they would have to run.

Then in early 2022 the broad markets started crashing hard. We’ve had a sequence of three lower lows after the first one and we may see another one or two this year. Pretty much a classic bear market pattern.

As an active investor who is a retiree with no new savings coming in, my job in these circumstances is well-defined. It is to sell securities that remain relatively high in order to buy securities that have crashed far harder than makes any sense.

In addition, permanent losses of capital would threaten the comfort of my retirement. So it makes sense for me to focus primarily on blue-chip stocks.

This article shares some of my decisions and where things stand now.

Overall Results

None of my investment decisions are based on beating the S&P 500 index. But it is nice when it happens.

Here are the index values and the value of the portfolio I actively manage, from Fidelity, as of December 28. To make the graphic, I scaled the vertical heights so that the curves shown are on proportional scales.

RP Drake, Seeking Alpha, Fidelity

My portfolio value is shown by the dark curve. The index is shown in orange.

In context, doing that well is a good result. But a better result is the positioning of the portfolio today.

[There are a few issues in comparing values from Fidelity to my assessment of after-tax value, which is what I care about. But these days those have a small impact. In addition, I trimmed the first couple of days off my values to exclude the impact of a withdrawal for a tax payment associated with a Roth conversion.]

While the enormous gains from 2021 are missing, the after-tax value of my full portfolio was down only 1% for the full year. That seems pretty good. It is certainly a lot better than the index, which was down 18%.

My outperformance for 2022 is almost entirely from my energy investments, which did after all run hard until early June (more details below). Since then my holdings have more or less moved with the index.

Now let’s look deeper, by sector.

Energy

It turned out that the energy markets had a lot further to run. I continued to ride the upward fluctuations in early 2022. This was made possible by the research, price targets, and chat room discussions at Michael Boyd’s Energy Income Authority.

The first five months of the year were quite a flurry. I closed the 16 positions shown in rows shaded blue in this table:

RP Drake

These positions were generally sized at 2% to 3% of the portfolio. When I took a gain, the proceeds were reinvested quickly. Overall, my weighted average gain on the closed positions was 25%.

Sometimes, the proceeds went into the next energy investment. But as the energy portfolio appreciated and some REITs crashed, I began to increasingly move some funds from energy to REITs.

Then in June the energy markets went flat or down. That made it time to hold what I had. Since I only buy companies I am willing to hold long-term, this created no angst.

In November I decided to increase my focus on dividends, as discussed here. That led me to sell Chord Energy (CHRD) and redeploy that capital.

My primary goal has been to own companies who will have significant upsides as we come out of the bear market. An additional goal has become to own companies who will sustain and grow their dividends, purchased at a high dividend yield.

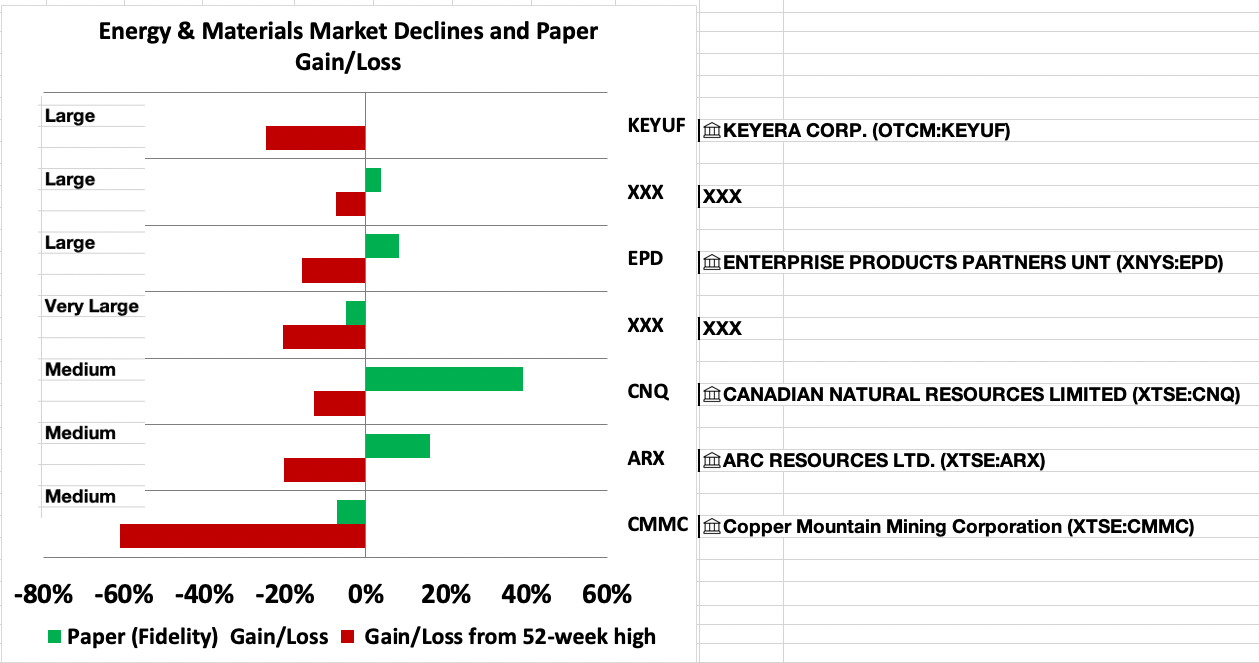

I display this below for my current holdings.

RP Drake

The green bars show my paper gain or loss on the position, as of December 31. The red bars show how far down the position is from its 2022 high.

Prices may or may not recover to those highs. But they are likely to move up from where they are now when we come out of this bear market.

[An aside here: participating in several marketplace services, I felt a need for some standard of when I would discuss positions found from any one service outside their chat room.

My standard is this. If the position has been discussed recently in a public article by the market place leader or me, then I disclose it freely. Most of them have been. But at the moment, two in energy have not. Hence the “XXX” labels above.]

In more detail, the top four positions are income positions. I don’t care much what their price does.

The bottom three are all positions I generated, with good input from that chat room. I’ve written articles on them here, here, and here.

I describe Canadian Natural Resources (CNQ) as my only dividend growth investment. Their 21% CAGR of dividend growth over the past 23 years is likely unmatched anywhere.

Canadian and ARC Resources (OTCPK:AETUF) are low-cost producers of mainly oil and gas, respectively. Both have resources that will support decades of production. I am positive on the ability of both companies to produce growing returns in nearly any pricing environment.

Copper Mountain Mining Corporation (OTCPK:CPPMF) owns a mountain that should make them good money across its lifetime. I discussed and evaluated that in the linked article and its predecessor.

I believe CPPMF to be substantially underpriced compared to peers. But there have been some new developments. As usual, commenters are very negative. I’m waiting for Q4 2022 results before digging in on that one again.

Going forward, my hope is that the upside of these last three positions lets me spin off some cash to increase the income positions. We will see.

REITs

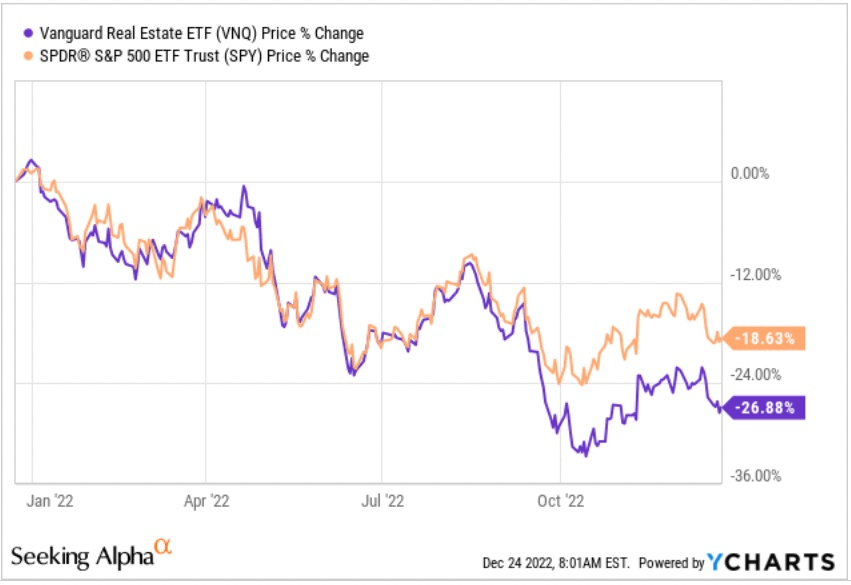

There was not a lot of money to be made in 2022 by buying REITs low and selling them high, unless one was a very adept trader. On average REIT prices followed the bear.

YCHARTS

It is worth noting that the dividend yields from VNQ are larger than those from SPY.

What could be done this year was positioning. Various REITs fell by various amounts at various times. By selling REITs that had fallen less (if at all), one could raise funds to invest in REITs that had fallen to unreasonable lows.

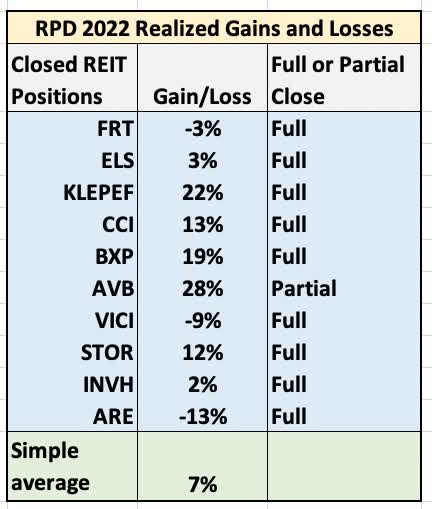

This was my approach. Here are the REIT positions I closed during 2022. The weighted average gain is 6.3%. All but STORE Capital (STOR) and Alexandria Real Estate (ARE) were sold early in the year to raise capital to exploit the bear market.

RP Drake

In addition, as the energy sector ran hard, I pulled funds out of it and put them in REIT stocks that had crashed. The ratio of my portfolio fractions in REITs/Energy changed from 33%/40% in January to 45%/32% at year-end. My money seeking upside is where the it seems the upside is.

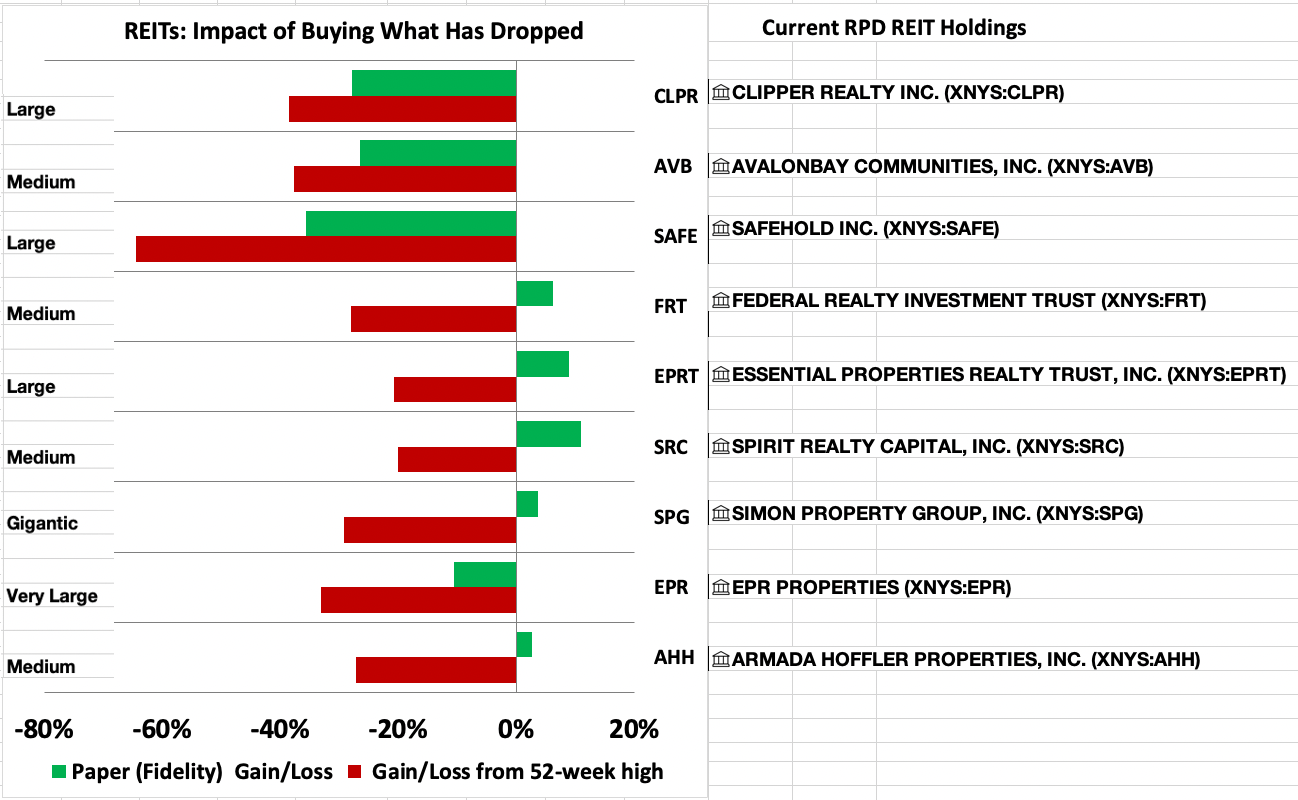

Here are my current REIT holdings, displayed using a similar graphic to the one above for energy. For six of these I have a paper gain near 10% and 25% upside to the 2021 high.

RP Drake

The other three have larger paper losses but much larger upside. These three are positions held for upside. All were down substantially before 2022.

Other Stuff

Influenced by Howard Marks’ memo Something of Value, I invested 12% of the portfolio in six MegaCap Tech firms during 2021. I wrote an article explaining why, published in early 2022.

Despite the bear market, that article still makes sense to me. I’m curious whether we will see a permanent reduction in advertising expenditures globally. This would reduce the growth of some of these firms, but does not derail the theses laid out in the article.

My initial investment was 2% of the portfolio in each of the six firms. Early in 2022 I used capital to sustain those fractions, but later there was nothing I was willing to sell for that purpose. At this point, the total fraction has dropped from 12% to 10.8%.

The relative winner at the moment is Oracle (ORCL). The power of their massive rewrite of their software suite to make it cloud native, combined with their implementation of Remote Direct Memory Access, has begun to have its impact. The analogy to Microsoft (MSFT) in the 2010s remains very compelling to me.

I also hold a 2% position in Ares Capital (ARCC) for income and as a store of value. Had it not dropped quickly in early 2022, it would have been sold to enable other investments.

There is not much to say about the 10% of the portfolio in private equity investments. I carry them at the value of the invested cash in my accounting, although in my view present value is quite a bit higher. I’m hopeful for very strong returns, but time will tell there too.

There are a few tiny positions with tiny chances of huge gains from here. Those are not an area of emphasis for me now, though. Nearly all of their cost basis dates from 2019 and 2020. Their combined paper losses amount to less than 5% of the portfolio market value.

Insignificant Losses

I did some modeling of losses and discussed it in an article for members of High Yield Landlord last June. The bottom line was that large losses of principal are just plain devastating to long-term gains in a portfolio.

To my eyes the losses are more devastating than might seem intuitive. This enhanced my appreciation of avoiding such losses.

This year went well from that perspective. My only large loss was a tax loss taken in my cryptocurrency investments (a minimum position when purchased). But since I immediately reinvested the proceeds back into crypto, I don’t count this as a permanent loss of principal.

Otherwise I took few losses and none that were large. In the energy investments, I took an 8% loss on Keyera (OTCPK:KEYUF) early in the year to invest in positions with very large upside. Ironically, late in the year I went back in, for very different reasons as discussed here.

In REITs, there were only two losses above 3% on any positions other than tiny ones. I sold VICI Properties (VICI) at a 9% loss to raise money for investments with upsides far larger than 9%.

I also sold ARE at a 13% loss in support of my transition to a higher-yield portfolio. I am very positive on ARE long-term. But my view became that appreciation there just depended too much on market valuation of earnings growth, which might not happen on my timescale.

In sum, that makes two years in a row with few and insignificant permanent losses of capital. We will see if I can make it three.

Takeaways

Investing in undervalued sectors sometimes gets you periods when they outperform the market. Making good selections of securities to purchase can enhance this.

In 2022 this worked out for me in the energy sector. My REITs did not produce big gains but seem quite undervalued now. And my MegaCap Techs, amazingly, almost seem like value investments.

The fraction of the portfolio in income positions increased to just over 50% at year-end. These are invested in firms that I believe to have good businesses that will grow earnings and dividends going forward. Their average yield at year-end was 8%.

That said, the upside positions seem likely to produce larger gains coming out of the bear market, for various reasons. At present, my thinking is to split those gains with half going into income positions and half going to (perhaps new) positions seeking upside.

More broadly, if you are retired then you need a clear picture of where your funds for spending will come from. If it will be covered by income sources in place already and you are investing to increase your legacy, then you probably have not read this far.

In contrast, if you require gains from your investments to provide those funds, then finding an investment approach that works for you matters. Perhaps it will involve some mix of income and upside positions like my portfolio.

As to me for 2023, my positioning for the end of the bear market is good. I just have to patiently wait for it to happen.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment