gustavofrazao/iStock via Getty Images

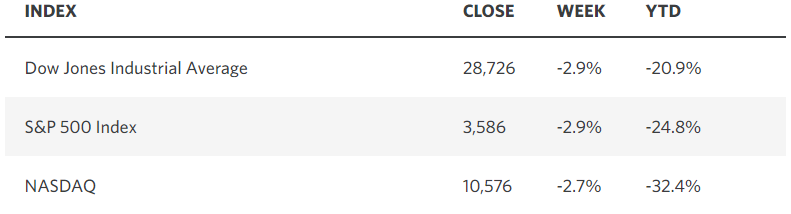

September has historically been the poorest performing month of the year for the stock market, and the one just ended didn’t disappoint on that front with the worst decline since 2008. The fear of higher interest rates has turned into full blown recession fears, driving the major market averages back into bear-market territory. The S&P 500 has now declined for three consecutive quarters, which is its longest losing streak since 2009. Fed officials have indicated that they are willing to sacrifice the ongoing expansion by choking off economic growth in order to bring the rate of inflation down to their target rate of 2%. In that effort, they see short-term rates rising as high as 4.4% this year and 4.6% in 2023 with no expectations for rate cuts. If that forecast comes to fruition, it is highly likely that it would result in a recession, but I see a very low probability of that happening. While the Fed’s track record for economic projections is extremely poor, as I’ve noted repeatedly, the primary reason I see a more dovish monetary policy outcome is that the wheels are already in motion for lower prices moving forward.

Edward Jones

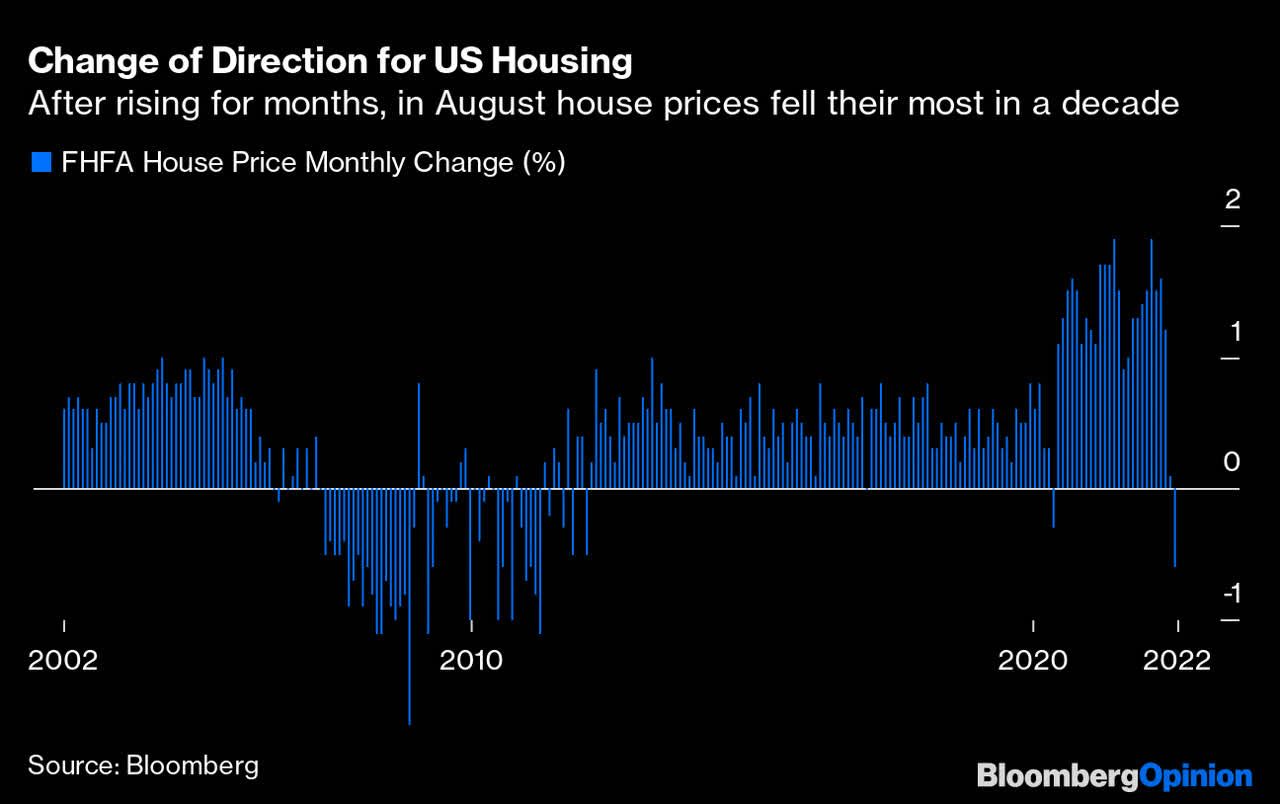

Oil, gasoline, and most other commodity prices have been moving lower since June. Shipping freight rates are back to pre-crisis levels, while trucking rates are well off their May peak. The Purchasing Managers Index for both the service and manufacturing sectors shows prices paid well below their peaks and falling. Most importantly, home prices have clearly peaked with the Case-Shiller index declining in July for the first time in a decade, and the FHFA survey realizing the same in August. September is bound to be even worse.

Bloomberg

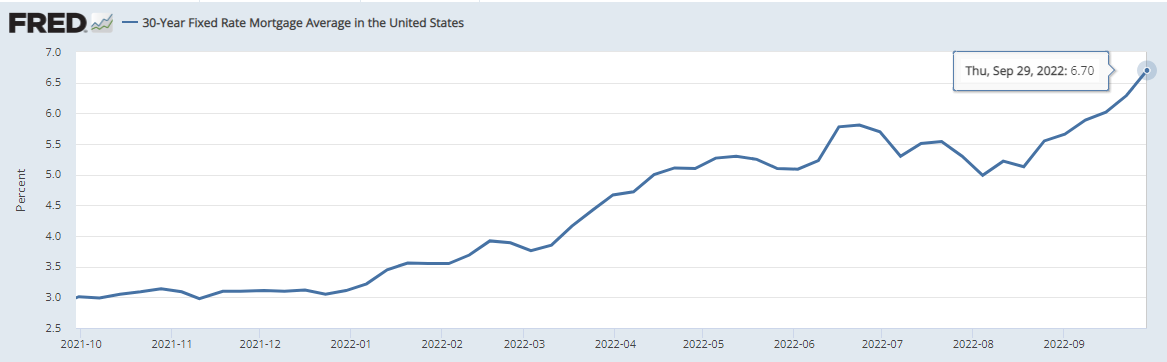

These declines are a result of the surge in 30-year fixed rate mortgages to 5.7%, but during the month of September the rate surged even higher to 6.7%. That should portend even greater monthly declines in prices in the months ahead, ultimately resulting in modest year-over-year declines next year. Lower home prices suggest that home owners would not pay as much to rent their own homes, which will weigh heavily on owners’ equivalent rent (OER). OER represents approximately 25% of the Consumer Price Index and 12% of the personal consumption expenditures price index (PCE). Again, the stage has been set for a rapid decline in the rate of inflation over the coming months. I think the Fed will be forced to recognize this before year end, pivoting from its extremely restrictive rate outlook and the rhetoric that has accompanied it, which will set the stage for a market recovery.

FRED

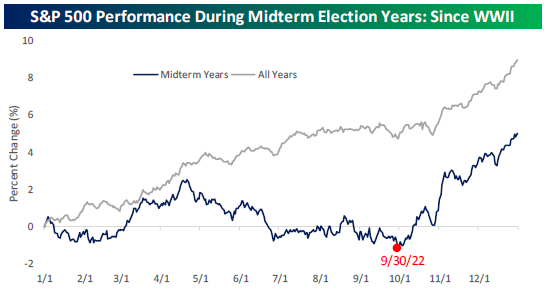

While some may be discouraged that Friday’s close for the S&P 500 was its low for the year, that is consistent with a precedent that has a bullish outcome. Bespoke Investment Group noted over the weekend that September 30 has been the absolute low point on average for all mid-term election years since WWII. What has followed after the election, on average, is very strong market performance. Not only is there uncertainty leading up to a midterm, but half the country typically prefers to see the market and economy perform poorly in hopes of regaining a majority in Congress. That is no longer an issue after November 8.

Bespoke

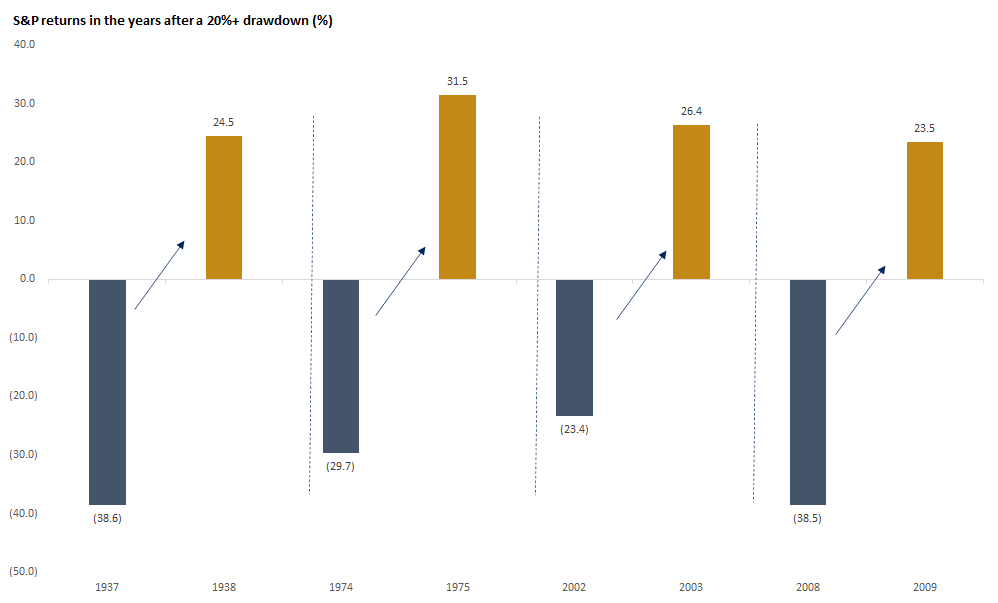

In addition to the favorable market conditions following a midterm, the returns in years that follow a drawdown of 20% or more have averaged a gain of better than 25%. The Nasdaq Composite and Russell 2000 have both held their June lows this year, but the S&P 500 broke below its June low last week, which I did not expect. Regardless, I think the broad market finds its bottom between now and November 8. An improvement in the fundamental outlook and investor sentiment should help the stock market follow the precedents I have just described.

Edward Jones

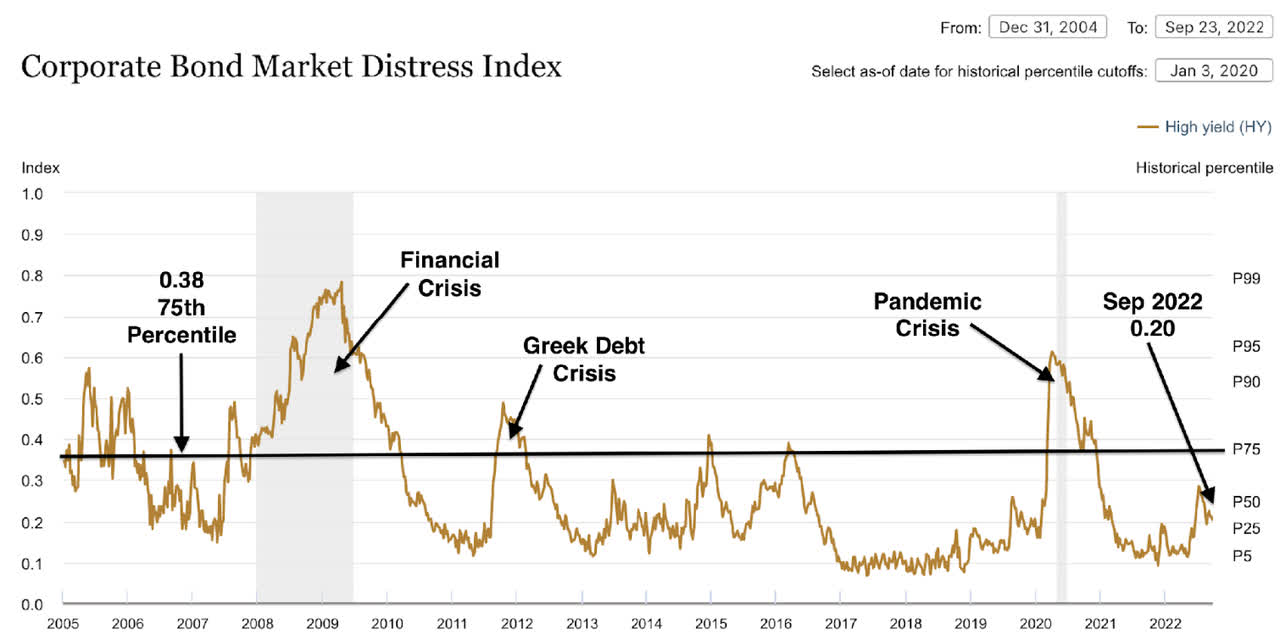

While the stock market has priced in a recession over the coming year, the bond market has given no indication that one is on the horizon. Bonds tend to be a lot smarter than stocks when it comes to the economy, because bond investors focus on credit. Credit spreads do not indicate the kind of stress that we see during economic contractions. To the contrary, they indicate very little stress at all, despite tightening financial conditions.

DataTrek

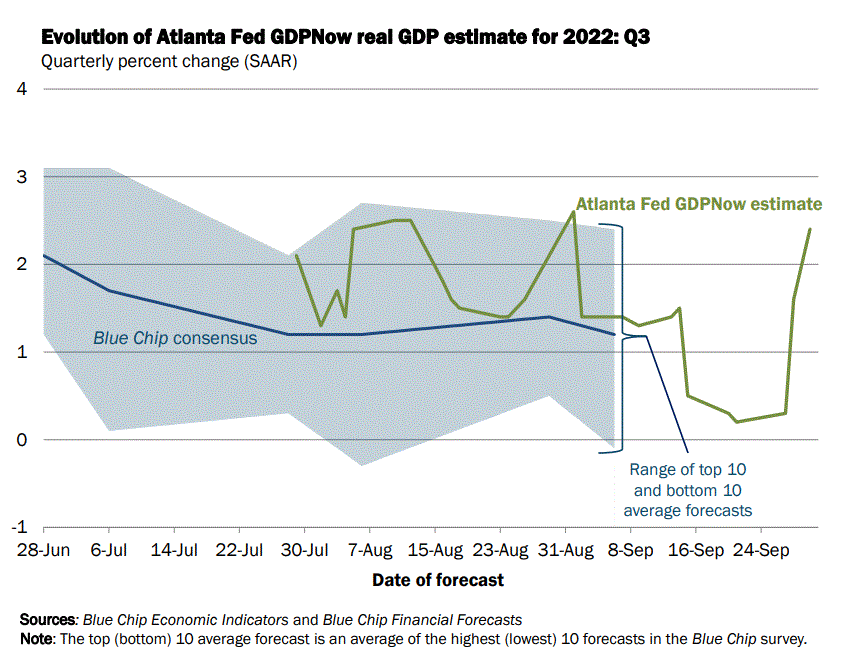

I have been steadfast in my assertion that we will avoid a recession this year and next, based on the strength of the consumer. Unlike prior cycles, the economy emerged from the last recession from the bottom up. The lowest quartile of incomes reaped the largest percentage increase in both wages and net worth since the pandemic. That bore out again in Friday’s consumer spending data for August, which showed a modest increase after accounting for inflation. It also led the Atlanta Fed to increase its estimate for the rate of economic growth in the third quarter from 0.3% to 2.4%.

Atlanta Fed

The importance of averting a recession is that bear markets tend to be shorter and shallower when not accompanied by one. In fact, their length and degree of loss are consistent with what we have already endured to date. That is why I think we are in a U-shaped bottoming process now. It is abundantly clear that the rate of inflation has peaked. The Fed should have plenty of data during the fourth quarter to recognize that, as well as conclude that a downtrend is firmly entrenched. Expectations for short-term rate increases should moderate, which should also halt the dollar’s ascent. I expect both to translate into less volatility and higher risk asset prices as we end this year and begin 2023.

Economic Data

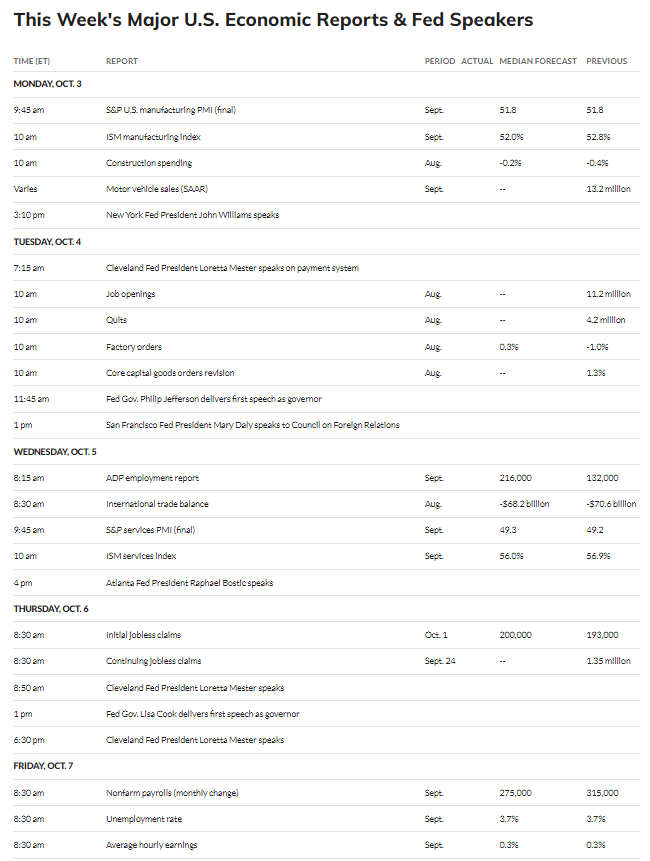

We have another week packed with data, but Friday’s payroll report will be the most important news. If we see a further softening in the labor market with fewer job additions and a more modest increase in wages, markets should respond well.

MarketWatch

Technical Picture

I am going to repeat what I said last week, as it relates to the S&P 500, since we broke below the June low at 3,636. The next significant level of support comes into play at the 50% retracement level from the bull market that started in March 2020 at 3,505. That’s not a meaningful decline from current levels.

Stockcharts

Be the first to comment