ArLawKa AungTun

Sometimes one likes foolish people for their folly, better than wise people for their wisdom.”― Elizabeth Gaskell

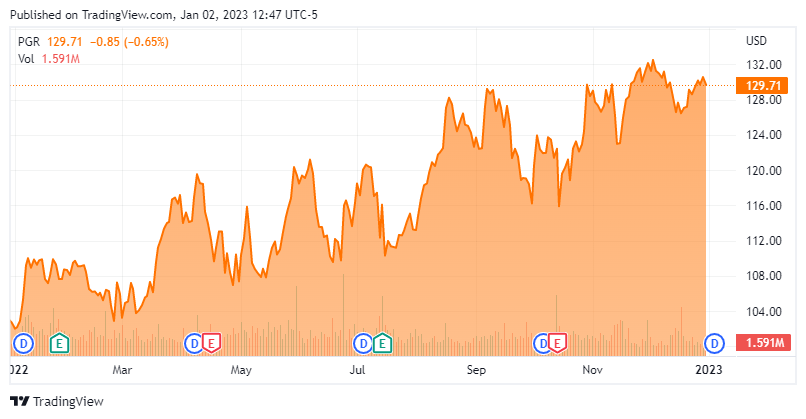

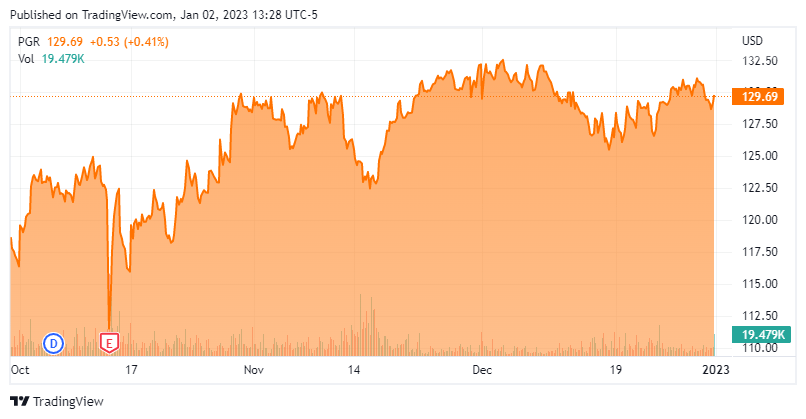

Today, we dive into The Progressive Corporation (NYSE:PGR), an insurance giant that was one of the few in the S&P 500 to fare well in the markets in 2022. However, insiders are selling shares, valuations seem stretched and the stock is unloved by the analyst community at the moment. Time to book gains in these shares or will they continue to outperform the overall market in 2023? An analysis follows below.

Seeking Alpha

Company Overview:

The Progressive Corporation is based just outside of Cleveland and the company provides personal and commercial auto, personal residential and commercial property, general liability, and other specialty property-casualty insurance products and related services in the United States. The stock currently trades just below $130 a share and sports an approximate market capitalization of $76 billion.

Third Quarter Results:

On October 13th, the company posted third quarter numbers. The company earned 20 cents a share on a non-GAAP basis. Net premiums written rose over 18% on a year-over-year basis to just north of $13 billion even as policies in force rose just one percent. Sales were just over $350 million shy of consensus estimates.

Analyst Commentary & Balance Sheet:

The analyst community is not sanguine of the company’s prospects at the moment. Since third quarter results posted, both Bank of America ($143 price target) and Jefferies ($147 price target) have reiterated Buy ratings. Citigroup ($104 price target), Wells Fargo ($100 price target) and Barclays ($109 price target) have reissued Hold/Neutral ratings on the equity.

Less than one percent of the outstanding float in the shares is currently held short. Numerous insiders were consistent and frequent sellers of the shares in 2022. In the fourth quarter, they disposed of just north of $12 million worth of equity in aggregate. The last insider purchase of over $20,000 was in 2016 when the shares traded at just over $30.

The company’s investment portfolio is just north of $50 billion. Progressive has just over $6 billion in long-term debt, $17 billion in unearned premiums and $30 billion in unpaid claims as of the end of the third quarter. The company’s debt to total capital ratio was a conservative 30.2% as of the end of the quarter.

Verdict:

The current analyst firm consensus has Progressive earning just over four bucks a share in FY2022 as revenues rise 10% to nearly $51 billion. Slightly faster revenue growth is seen for FY2023 as earnings per share come in around $6.30. It should be noted there is wide variance in the 18 analyst firms that have posted projections ($3.68 to $7.70 a share).

The company did me a solid in 2022, providing a much lower auto insurance premium than my longtime carrier Geico. That said, I find that policy much more attractive than the stock right now. The stock sells for 20 times forward earnings and 1.5 times revenues. In comparison, competitor The Allstate Corporation (ALL) trades for under 15 times forward earnings and under .8 times revenues. While it is true slower sales growth (6% versus 11%) is projected for FY2023 for Allstate, the stock provides a higher dividend yield (2.51% versus 1.46%).

Insurers should benefit from higher interest rates helping their bond portfolio returns in 2023. Premium increases as the result of Hurricane Ian should also be a tailwind. Progressive lowered the estimates for its losses from that storm event two weeks ago. Average auto insurance rates have risen 12% YTD at the company through the third quarter, which seem unsustainable. The stock also seems to be topping out in recent months, the analyst community is hardly positive on the shares and insiders are frequent sellers of the equity as well.

Seeking Alpha

The bottom line is after a better than 25% return in the market in 2022, positive tailwinds seem fully priced into the stock as current trading levels.

The problem is that the people with the most ridiculous ideas are always the people who are most certain of them.” – Bill Maher

Be the first to comment