bymuratdeniz

It turns out that the weaker dollar is indeed helping to lift commodity prices. Add to that the euphoria over a China reopening will keep inflation rates elevated and much slower to come down than the market is currently pricing in.

Bloomberg

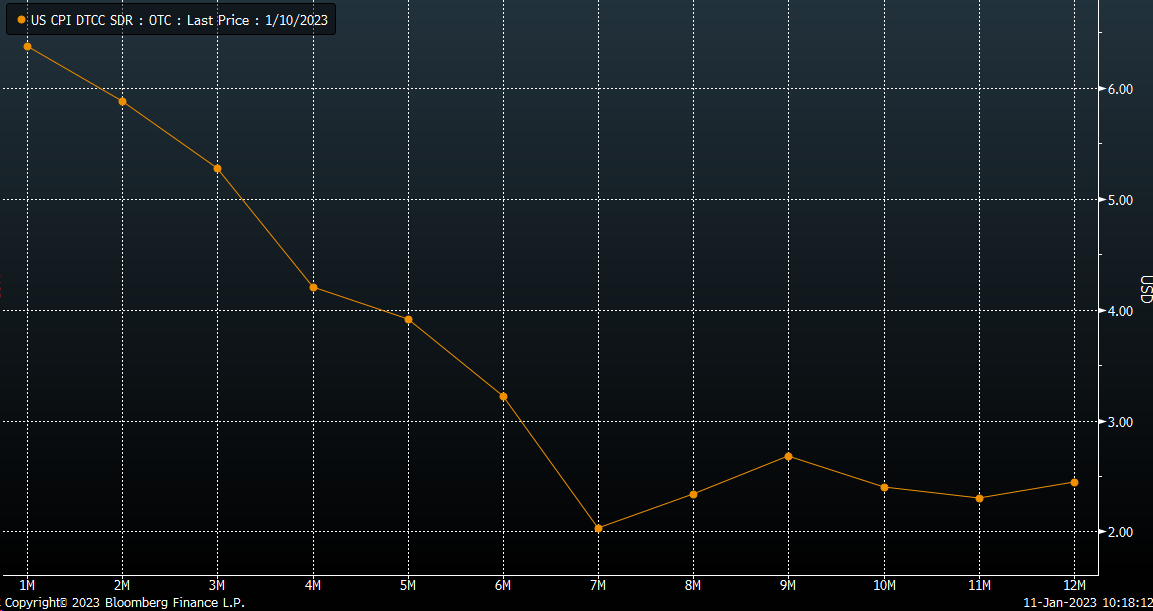

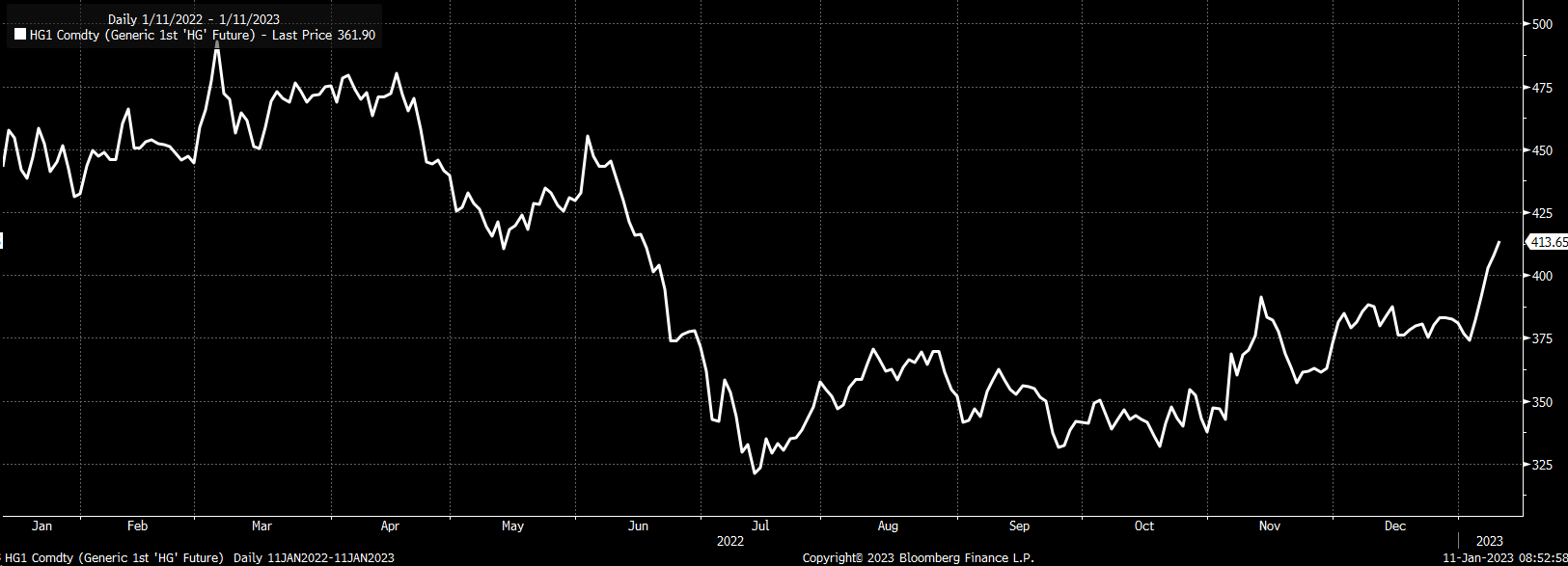

Inflation swaps see the CPI falling to just 2.0% by June, and that may be not only optimistic but unrealistically optimistic. As the dollar has weakened and financial conditions have eased, and commodity prices have been ripping higher. Copper prices are now up more than 30% since mid-July. On top of that, copper prices have now risen 8.4% this month alone.

Bloomberg

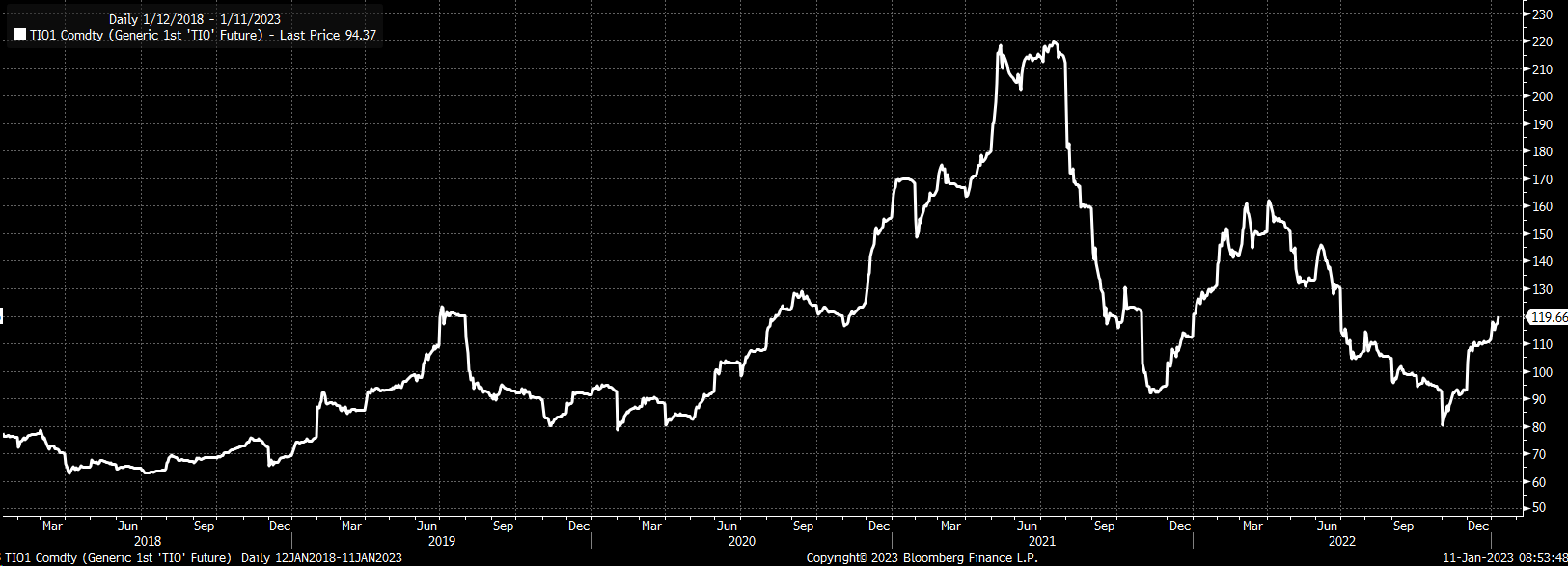

It isn’t only copper. We’re now seeing iron ore prices rise sharply as traders and investors begin to anticipate China coming back online. Since the Oct. 31 low, iron ore prices are up almost 62%, and while they’re still down sharply, it’s a big move, and if they continue to rise, it brings a slew of higher prices with it.

Bloomberg

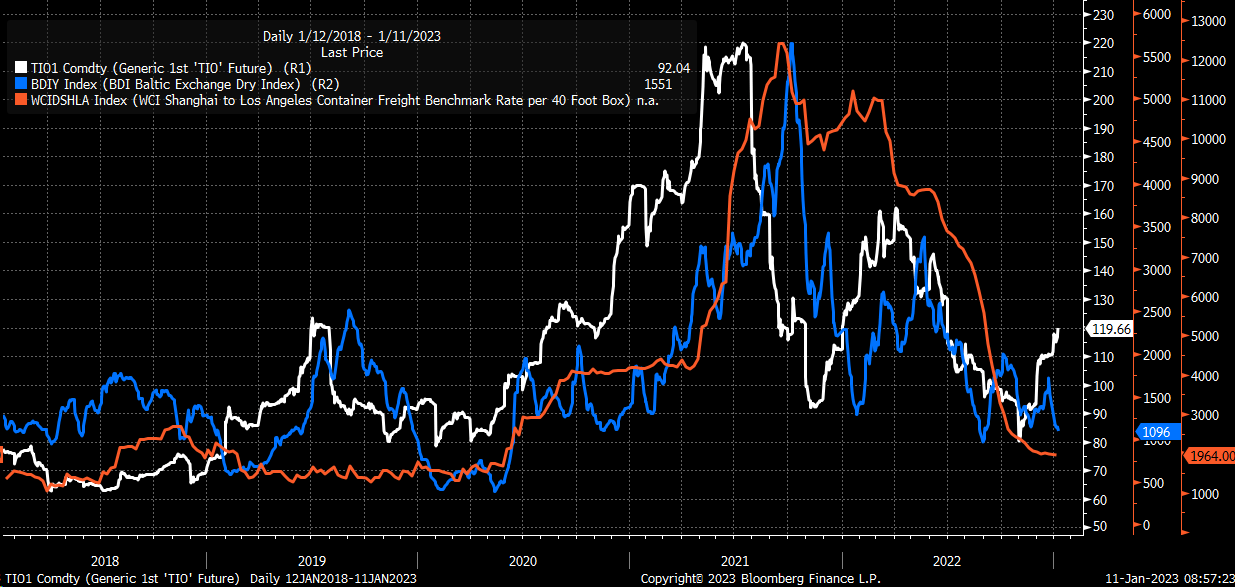

Base metals like copper and iron ore are significant components in construction and are shipped to China from places like South America, Africa, and Australia. With more demand for these metals and other commodities, shipping rates will begin to rise.

Bloomberg

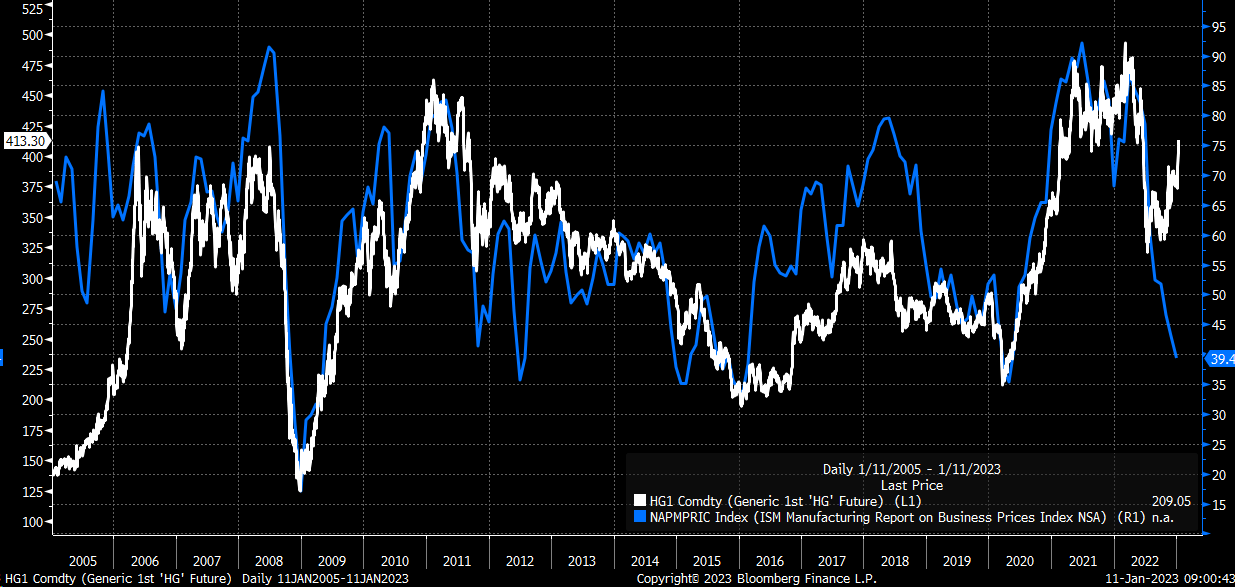

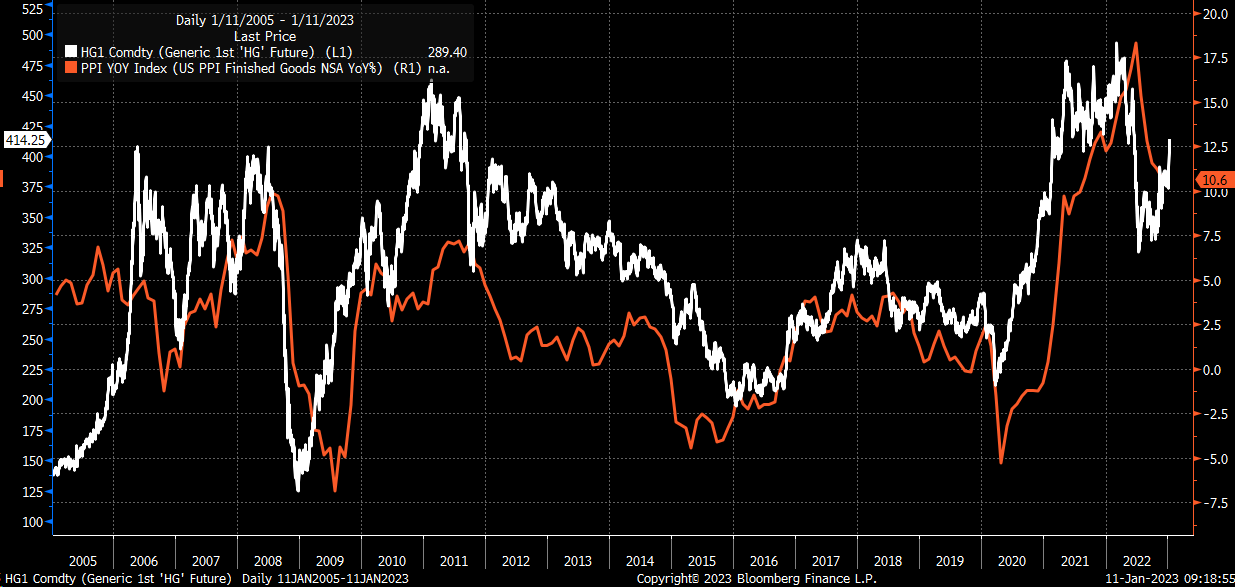

Higher commodities like copper also are highly correlated to producer prices and surveys like the ISM manufacturing prices paid index. With copper prices rising, manufacturing costs may be higher after the most recent increase in copper.

Bloomberg

But on top of that, producer prices also often follow commodity prices. So while inflation can slow, the idea that inflation is just going to melt away seems unlikely to happen.

Bloomberg

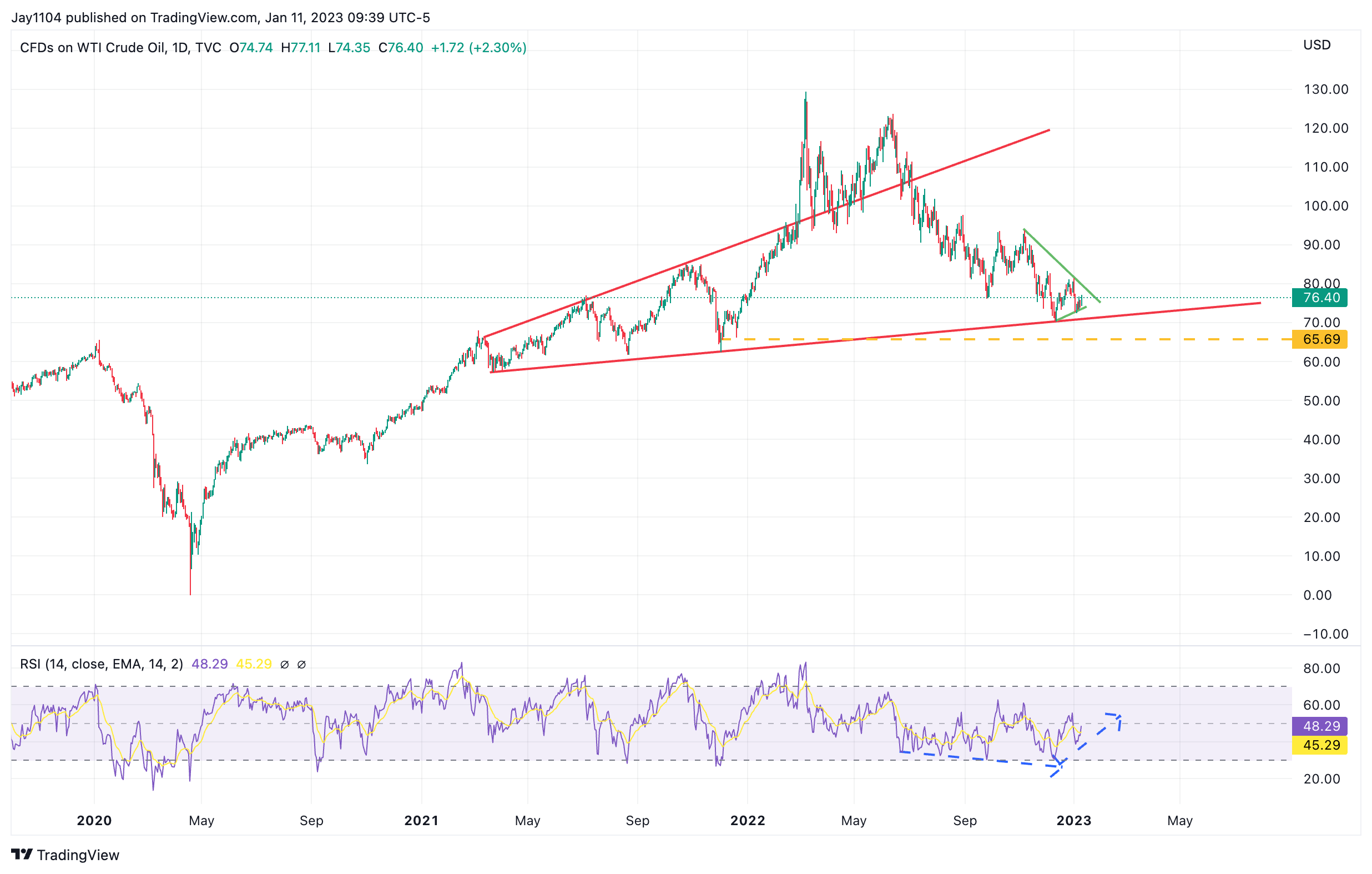

Mind you, oil prices have hardly even moved yet, and those prices are likely to rise as China comes online, and the US begins to refill its strategic petroleum reserve. The technical chart of oil has been improving with an RSI that’s reversed from falling to rising, a bullish divergence from the current lower trending price. It would take a move above $80 for oil prices to break out and potentially run back to $90.

TradingView

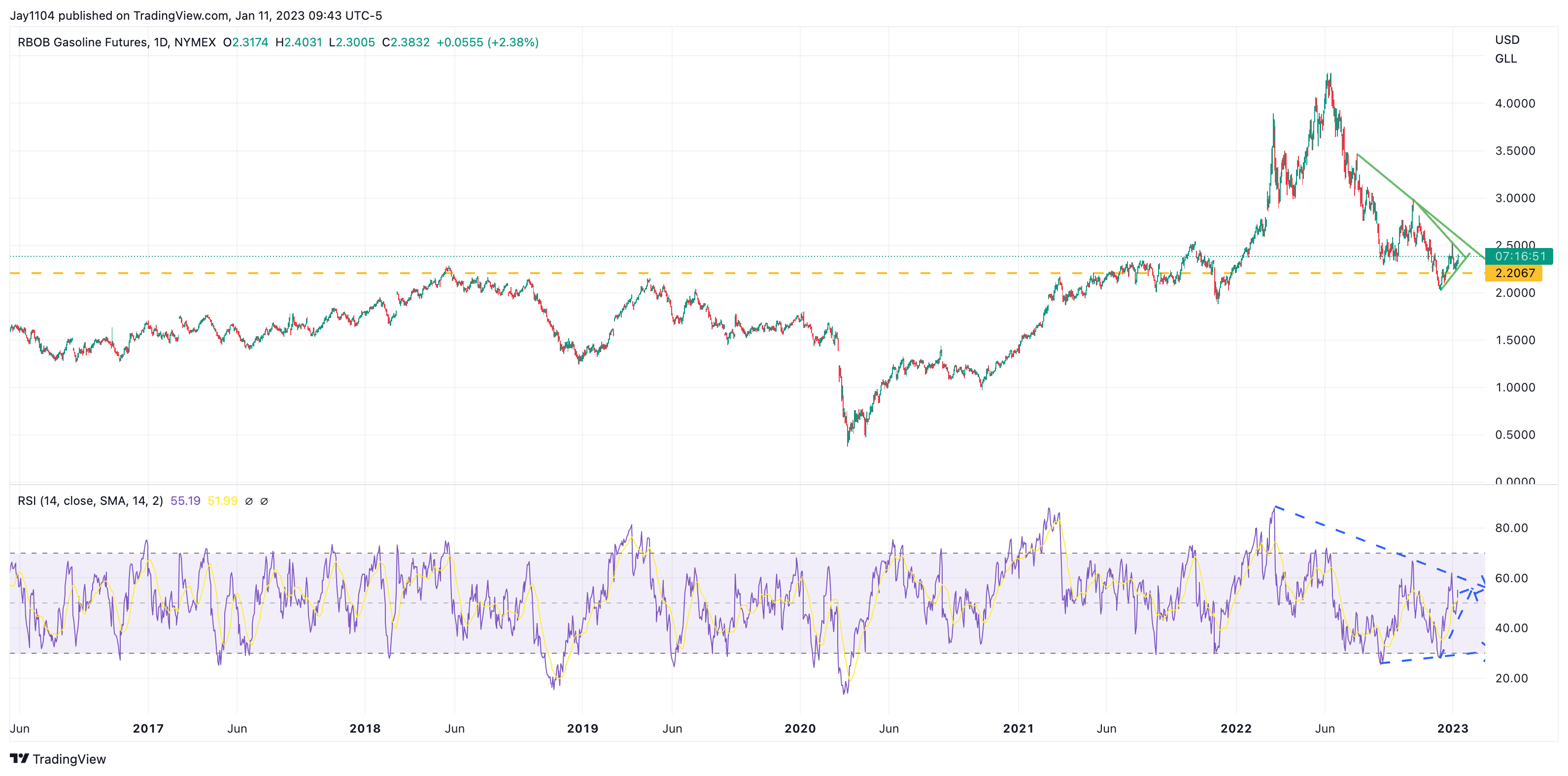

Higher oil prices can feed into higher gasoline prices, which also show signs of turning higher. While the cost of RBOB gasoline prices has been steadily declining, the RSI has now made a higher low, while the price of gasoline made a lower low, which can signal that gasoline has put in a bottom with momentum turning from bearish to bullish.

TradingView

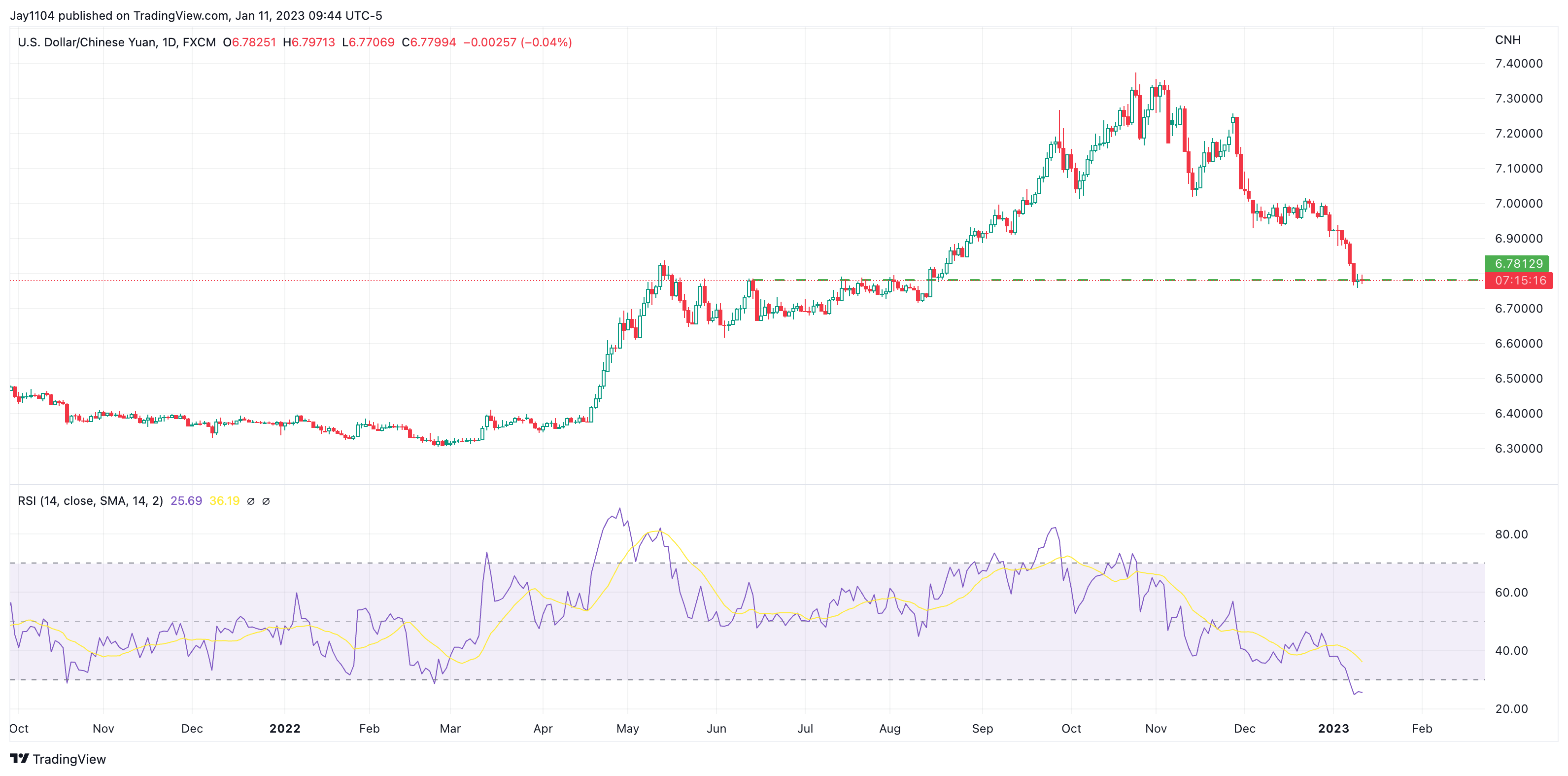

On top of this, we have seen the Chinese RMB strengthen dramatically against the dollar. When the RMB falls, it indicates strengthening against the dollar as it takes fewer RMB to buy a dollar. Should the RMB continue to strengthen, that will likely add to inflationary pressures on imported goods.

TradingView

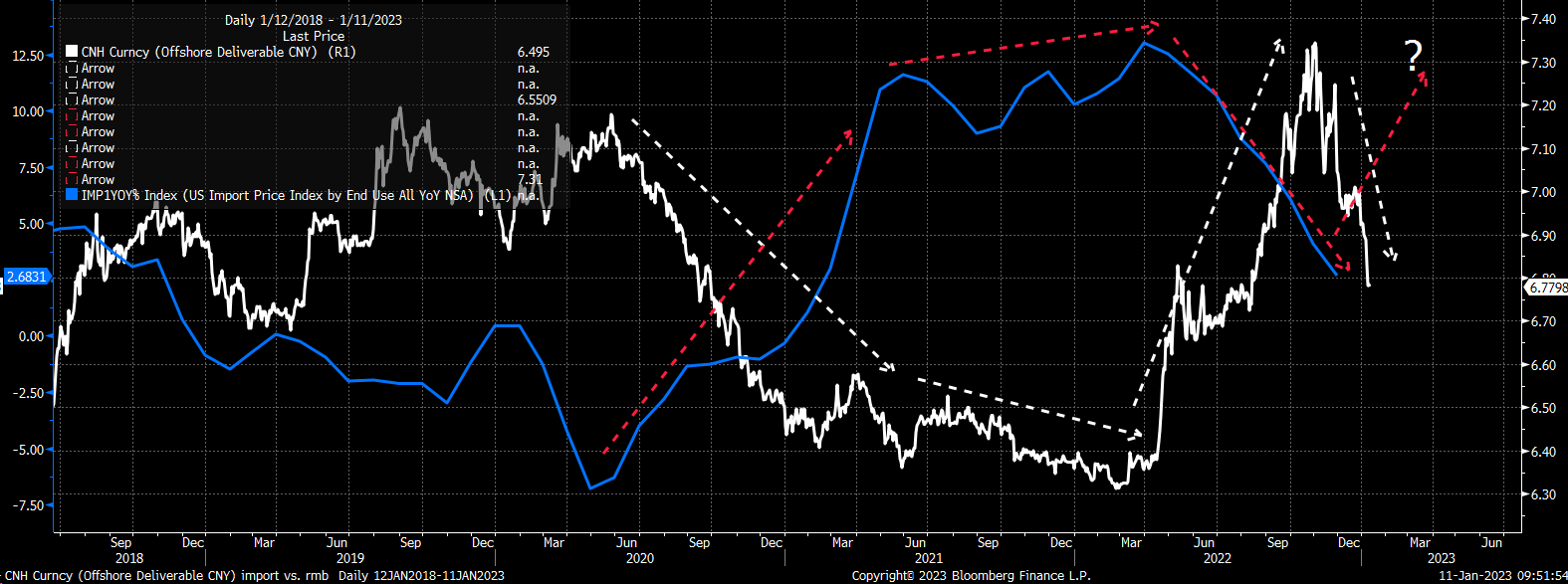

When the RMB has strengthened, it has boosted import prices, and when the RMB began to weaken, it resulted in import prices falling. With the RMB strengthening again, one needs to wonder if import prices will surge again.

Bloomberg

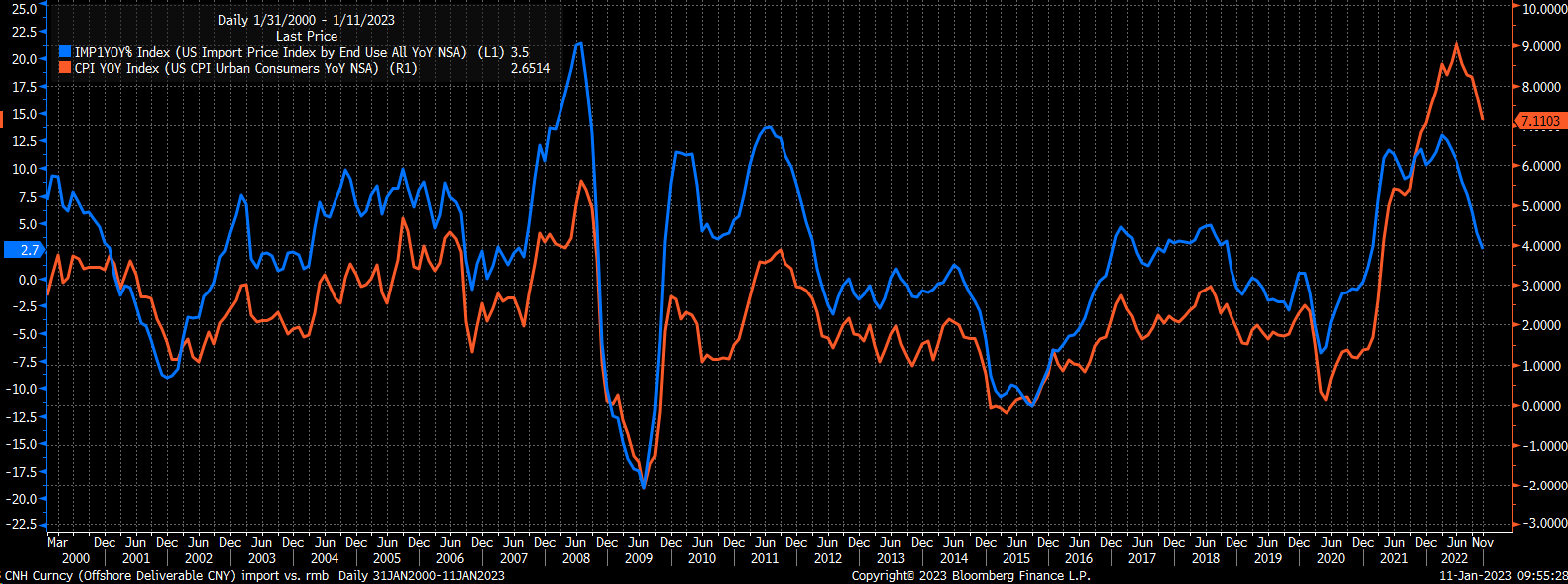

Import prices over time tend to lead to changes in the CPI index and the year-over-year rate of change. So if these current trends continue, then inflation may subside for a month or two, or maybe even three, but is either likely to surge higher again or get stuck somewhere in the middle.

Bloomberg

If the ISM data from last week indicates a weakening US economy, causing the dollar to weaken as China comes back online and commodity prices rise along with shipping and import prices. In that case, it could lead to slowing economic growth and high prices.

Be the first to comment