RichHobson

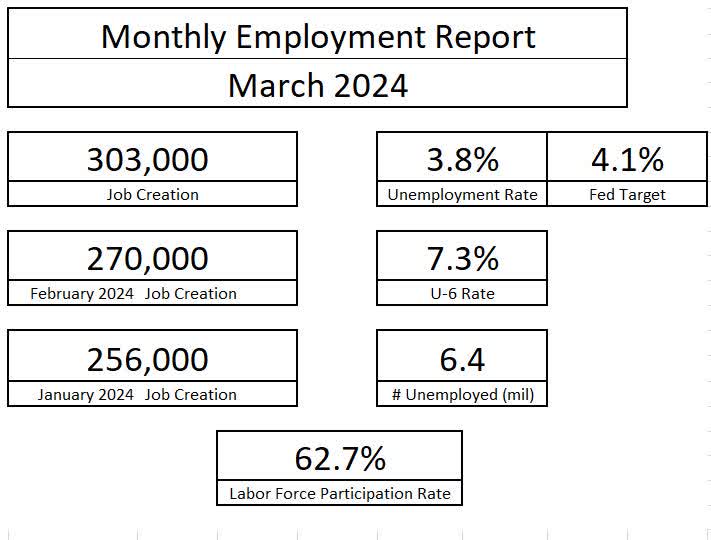

Earlier today, the Bureau of Labor Statistics released the March employment report which showed that the economy created 303,000 jobs in the month of March, well above consensus estimates. While the headline number isn’t everything when it comes to assessing the strength of the labor market and the overall economy, nothing in the March jobs report points to a need to lower interest rates.

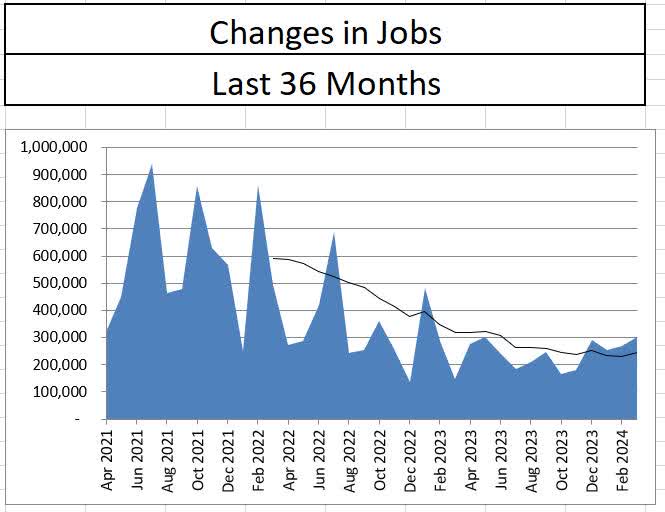

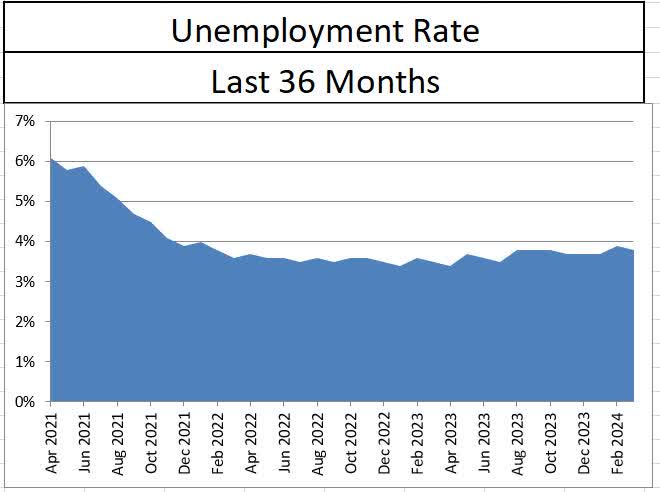

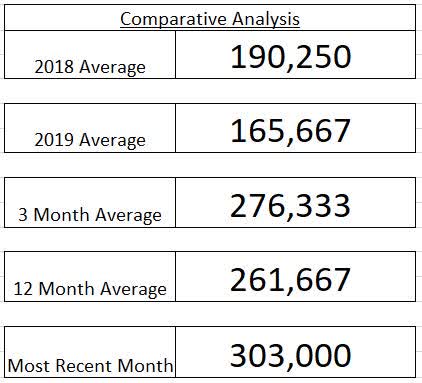

The March employment report, combined with the revisions for January and February, show a trend reversal in job creation with employment gains growing. The unemployment rate also reversed downward from 3.9% to 3.8%, which moves it away from the Fed’s 2024 target. Additionally, the average monthly job creation over the last 12 months remains obnoxiously higher than the pre-pandemic levels.

Bureau of Labor Statistics

Bureau of Labor Statistics

Bureau of Labor Statistics

Bureau of Labor Statistics

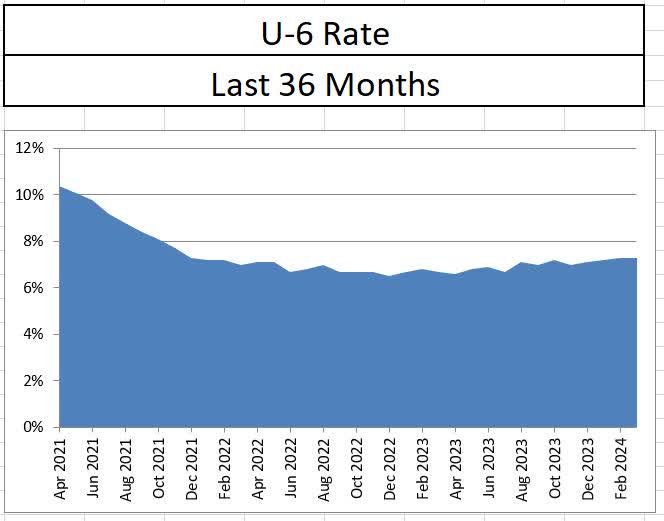

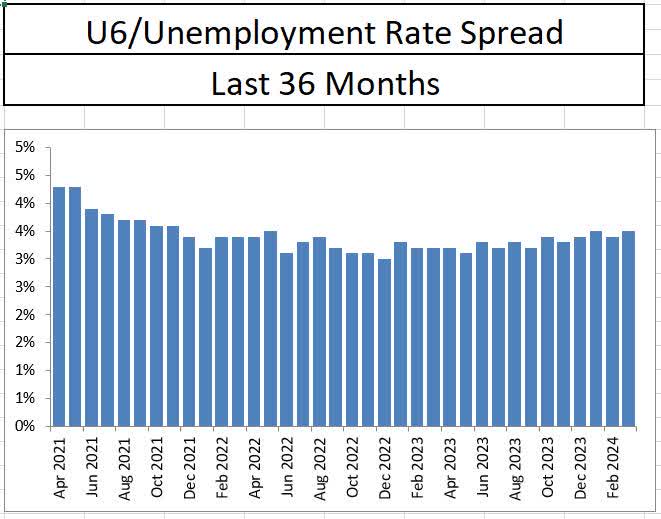

Not all the data represented in the March report showed a strengthening of the labor force. The U6 rate, or broadest measure of unemployment, which includes workers who are underemployed, remained at 7.3% in March. These levels are the highest since December 2021. The spread between U6 and U3 grew one tenth to 3.5% in March. This ties the highest level going back to November of 2021, meaning while jobs are being created, a larger group of the employed are still seeking more hours.

Bureau of Labor Statistics

Bureau of Labor Statistics

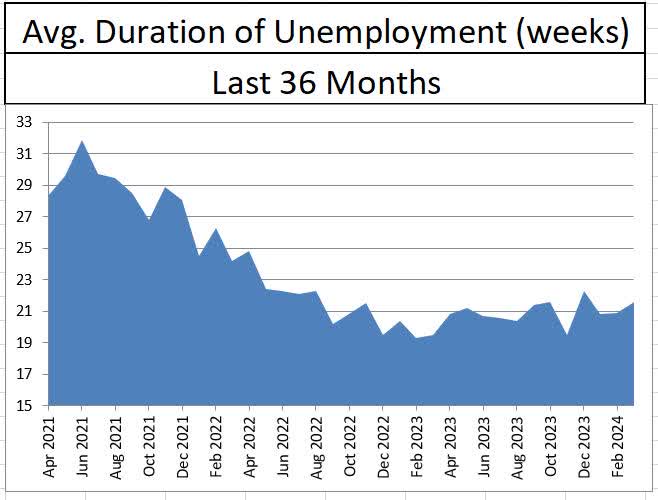

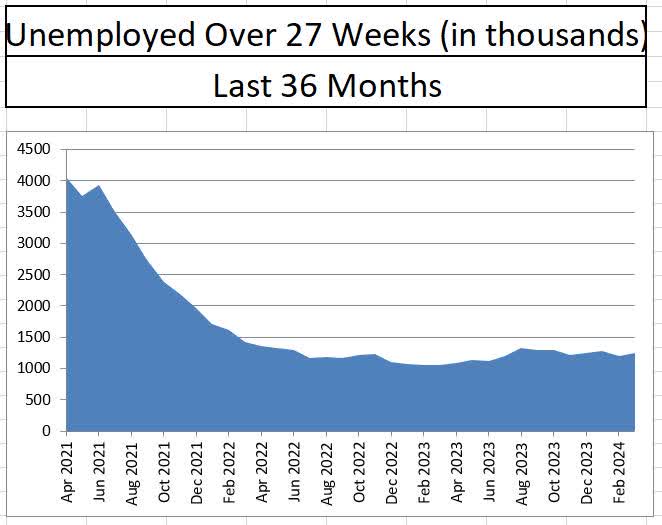

In addition to U6 data, the average duration of unemployment has ticked up to 21.6 weeks, which is within range of pre-pandemic levels. The number of unemployed over 27 weeks also ticked up to 1.25 million, which is slightly below pre-pandemic levels, but edging very close. Unemployment duration, while choppy, is slowing beginning to show signs of normalization.

Bureau of Labor Statistics

Bureau of Labor Statistics

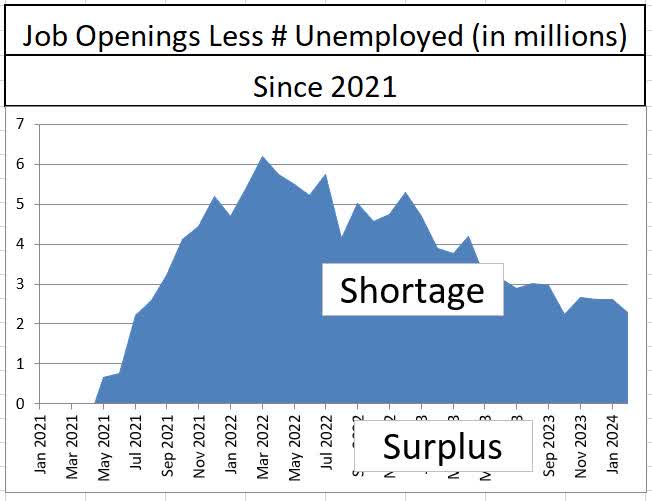

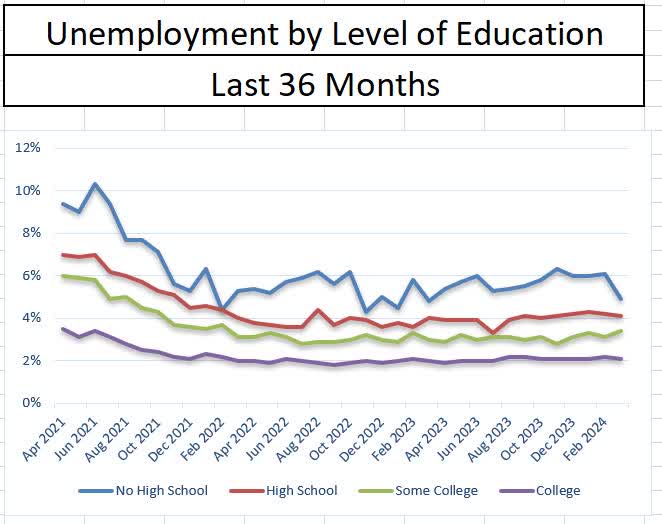

While normalization is promising, it does not necessarily indicate weakness in the labor market. For example, there are still 2 million more open jobs in the economy than the number of unemployed, which exceeds any levels seen prior to the pandemic and still underlines a labor shortage. Additionally, the unemployment rate among those without a high school education dropped below 5% in March, more than a full percentage point. The labor force is still pulling out anyone willing and able to work.

Bureau of Labor Statistics

Bureau of Labor Statistics

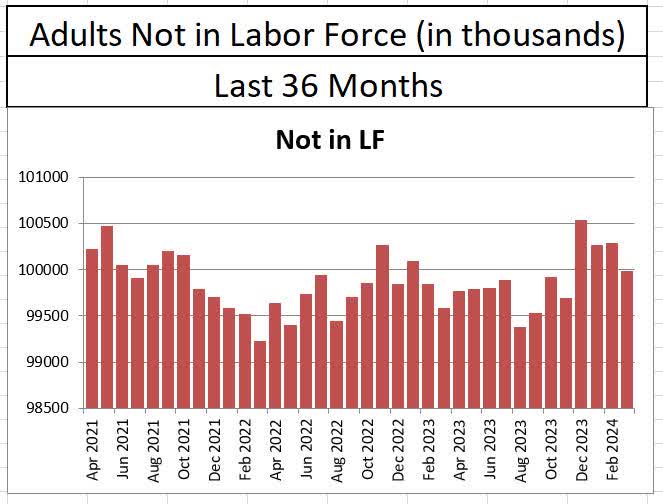

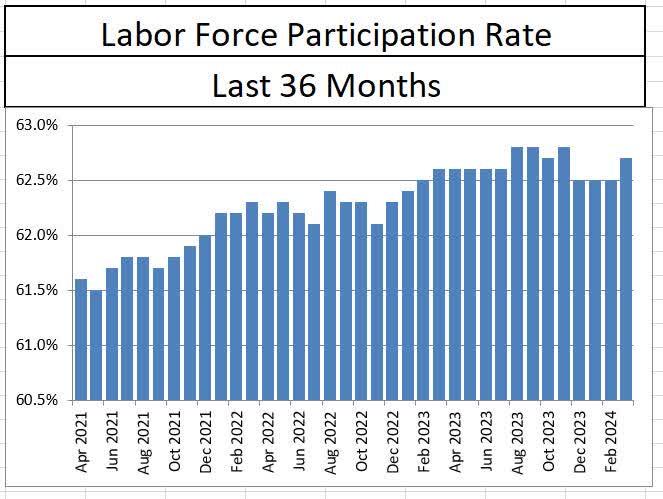

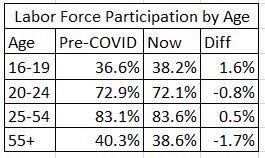

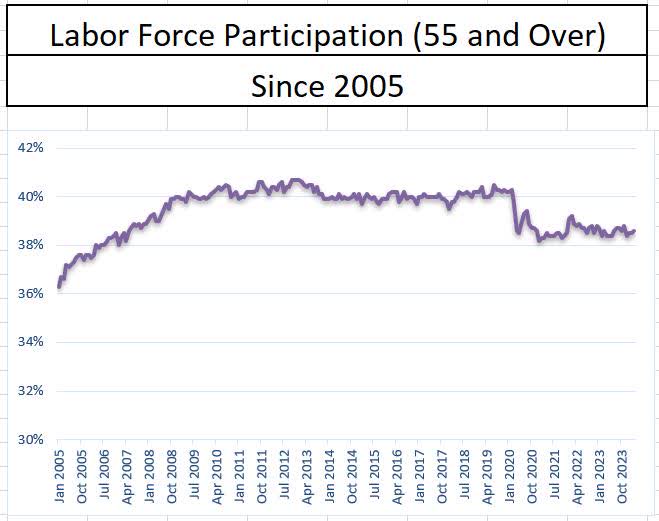

Another impressive strength in the March jobs report comes from labor force participation. The number of adults not in the labor force declined in March, which helped drive up the labor force participation rate. Usually when these flows occur, unemployment ticks up because the newly entered labor force participants start as unemployed. That relationship did not happen last month as it appears new entrants to the labor force jumped into employment at a much quicker rate than past reports. It’s important to note that the largest laggard in labor force participation remains the group aged 55 and over. Prime age employees are working at a higher participation rate than pre-pandemic and it appears the labor force strains are being caused more by demographics (ie retirements) than anything else.

Bureau of Labor Statistics

Bureau of Labor Statistics

Bureau of Labor Statistics

Bureau of Labor Statistics

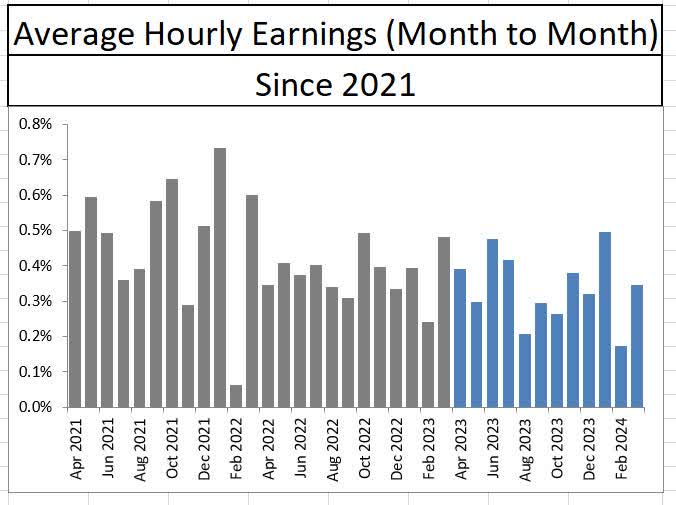

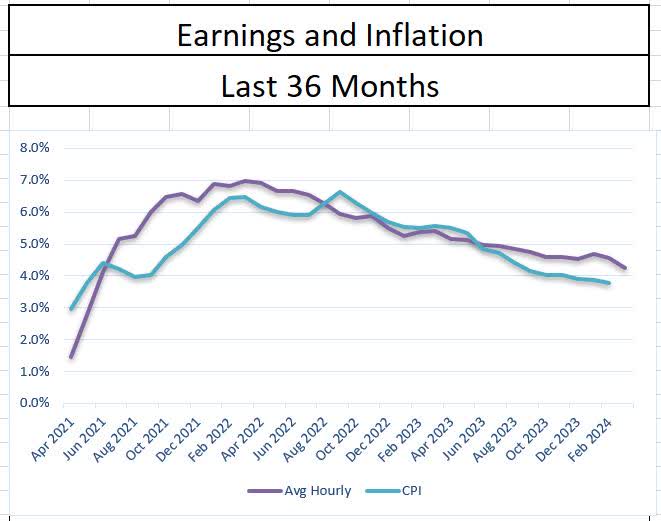

While many may argue that the quality of jobs being created does not match with what exists in the labor force, the average hourly earnings growth paints a different picture. On a month-over-month basis, it appears as if average hourly earnings are on the verge of stalling, but when looking at things from a year over year point of view, there’s a slow and steady easing occurring. Despite the disinflationary trend in wages, wage growth is still far above what will be needed to support a sustained 2% price growth target.

Bureau of Labor Statistics

Bureau of Labor Statistics

Overall, nothing in the March employment report indicates a level of weakness that justifies interest rate cuts. The drop in unemployment rate, increase in wages, and increase in labor force participation are all indicative of a strong employment market that is contributing heavily to price inflation. Stimulating this area through rate cuts could have unintended consequences including stronger labor shortages, higher wages leading to higher inflation, and ultimately even higher than current interest rates to correct the reversal.

Be the first to comment