Meinzahn

Here at the Lab, we positively view the EU Diversified Financials sector. Within our coverage, we have multiple buy ratings on Euronext (Clean Q4 Results) and the London Stock Exchange Group (Microsoft deal is a Game Changer). To update our readers, today we are back to comment on Deutsche Börse (OTCPK:DBOEY) (OTCPK:DBOEF). Since our last coverage, VIX Is A 2023 Key, the company has almost reached our target price. That said, we believe there is much positive news to price in. In addition, the company’s top-line sales, EBITDA, and earnings per share have reached new records every year. However, despite a solid track record, Deutsche Börse’s valuation has steadily derated in the last four years.

Positive View

Before going to the numbers, it is vital to report why we are optimistic about the company.

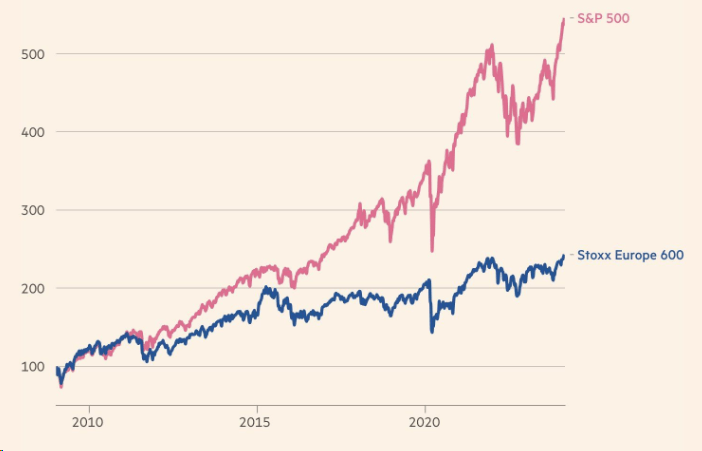

Firstly, allocating part of the portfolio to low-beta companies is essential. This is also true during times of macroeconomic and geopolitical uncertainty. Here at the Lab, we still view EU companies’ valuation at a steep discount compared to the US ones. Therefore, we expect higher asset allocation in EU-depressed assets. This might support the Diversified Financials Trading & Clearing division.

S&P 500 vs Stoxx Europe 600

Source: FT – The unfulfilled potential of Europe’s stock markets

Taking advantage of our sub-sector expertise, in our view, Deutsche Börse trading & clearing businesses are not correctly valued. The company has a strong market position and is a high-margin division. In addition, recurring revenue generation has significantly increased. Looking back, in 2020, they generated less than 50%, while in 2023, recurring revenue accounted for more than 60%. Thereby, Deutsche Börse is not far from the London Stock Exchange Group results, the EU industry benchmark.

Last year, the company acquired SimCorp for a total consideration of €4 billion. Many investors perceived this transaction as expensive with almost no synergies. Here at the Lab, we have a different view. SimCorp is a Danish player that engages its activities in providing services and software to financial institutions. Again, we see analogies to the Refinitiv deal performed by the London Stock Exchange Group. At first, this was viewed as far from LSEG’s strategic activities, but later on, this proved to be a successful bolt-on acquisition. Going back to the Deutsche Börse analysis, the combination of SimCorp and Axioma (Deutsche Börse software solution division) is complementary. The CEO has already reported strong growth with US client wins, and looking at the Q4 results, the software solutions’ annual recurring revenue has already reached a +14% increase compared to last year.

Business-wise, despite lower derivative activities, cash market trading volumes were up. Derivative volume decline is mainly driven by seasonality. This is because volumes typically spike in December due to the contract rollover.

2024 Earnings Projection

Looking at the Deutsche Börse numbers, we now incorporate the SimCorp acquisition and the company’s latest strategy called “Horizon 2026.”

Cross-checking Wall Street analyst consensus, the company reported Q4 sales at €1.43 billion, up 5% year-on-year. SimCorp’s organic growth supported this. Sell-side analysts were forecasting a plus 0.4%turnover.

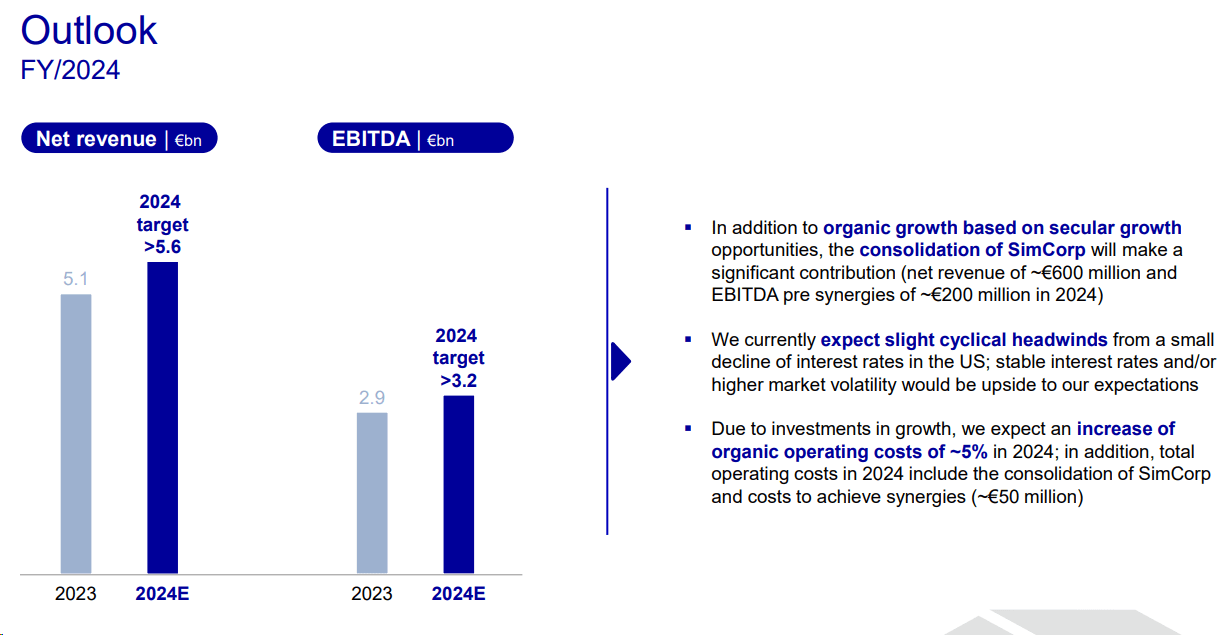

The company guided a full-year 2024 revenue and EBITDA of €5.6 billion and €3.2 billion, respectively (Fig 1). That said, given Deutsche Börse’s tendency to issue a conservative outlook, we might anticipate higher guidance as the year progresses. With the new strategy, the company guide double-digit revenue and profit growth by 2026. SimCorp will likely contribute to a further 3% growth per year. Incorporating the SimCorp deal, we now forecast 2024 top-line sales of €5.8 billion (above the company’s target) with an EBIT of €2.85 billion. We guide €600 million in sales from SimCorp and an EBITDA step-up of €220 million, including conservative lower costs from consolidation. Considering a higher debt due to the deal (and an ongoing deleverage), we arrive at a 2024 EPS of €10.5.

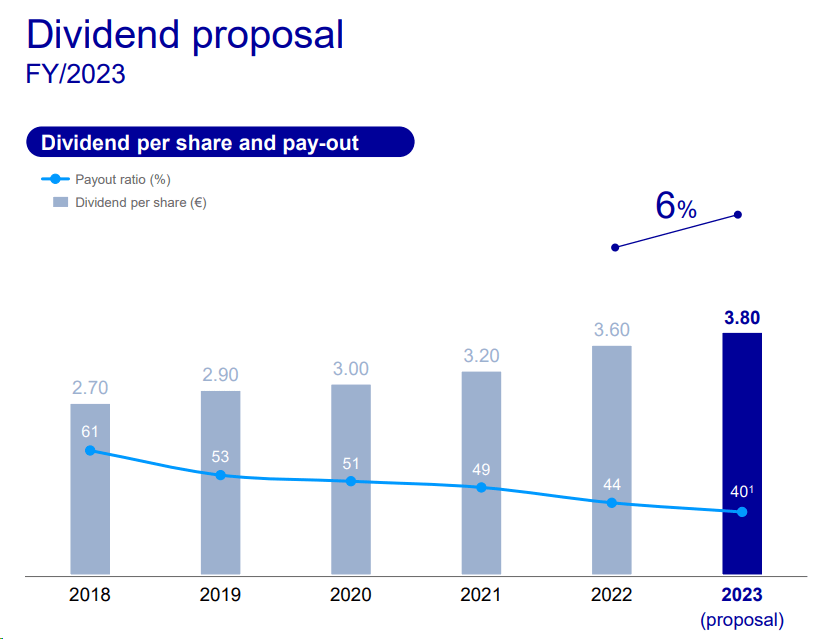

To support our buy rating, Deutsche Börse proposed a dividend payment of €3.80 per share, a 6% uplift from last year (Fig 2). The company has a payout ratio target between 30-40% and intends to complement the DPS with buybacks. In detail, the company has an approximately €150 million share repurchase program to complete. A lower payout ratio and higher dividend per share are supportive company trends that cannot go unnoticed.

Deutsche Börse 2024 Outlook

Source: Deutsche Börse Results presentation – Fig 1

Deutsche Börse DPS proposal

Fig 2

Valuation

In our estimates, the company trades at a P/E of 18.5x, but we see scope for a re-rating above 20x. Indeed, Deutsche Börse’s historical 5-year P/E ratio was around 20.4x, which we believe is a good benchmark for value infrastructure companies. Players such as Deutsche Börse are supported by secular growth trends such as the expansion of repo offerings and new products like crypto trading. With our 2024 EPS and applying our 20x P/E target multiple, we arrive at a valuation of €210 per share. We reiterate our Buy rating target, which is also supported by a 5Y monthly beta average of 0.62.

Risks

Our downside risks include 1) lower derivatives and trading volume, 2) regulatory risks, 3) lower IPO activities, and 3) inflationary pressures with wage inflation. Deutsche Börse faces new competitive risks from alternative trading venues. In addition, given the stock exchange location, an EU macroeconomic deterioration could impact the company’s earnings due to lower trading volumes.

Conclusion

Despite a positive earnings trajectory, the Deutsche Börse P/E ratio is lower than its historical 5-year average. The payout ratio allows the company to increase its DPS year over year while investing in growth activities. Key to the report is Deutsche Börse aims to increase its recurring revenue line towards the LSEG benchmark. For this reason, we believe that Deutsche Börse is a safe investment that combines earnings growth and low market correlation.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment