Dorin Puha/iStock via Getty Images

A Quick Take On The Honest Company

The Honest Company, Inc. (NASDAQ:HNST) went public in May 2021, raising approximately $413 million in gross proceeds from an IPO that was priced at $16.00 per share.

The firm sells ecologically conscious products to consumers in the U.S. and overseas.

I’m on Hold for HNST until it can show revenue growth and meaningful progress toward operating breakeven.

HNST Overview

Los Angeles, California-based Honest Company was founded to develop an omnichannel system for the sales of eco-friendly products to consumers.

Management is headed by CEO Nikolaos Vlahos, who has been with the firm since 2017 and was previously EVP and COO – Household, Lifestyle and Core Global Functions of The Clorox Company.

The company’s primary offerings include:

-

Skin and Personal Care

-

Baby, Diapers & Wipes

-

Household Products

- Bath & Body

The firm sells its products through retail and digital channels as well as direct-to-consumers (DTC) via its website.

Market & Competition

According to a 2019 market research report by Food Business News, the U.S. market for sustainable products of all types was an estimated $125.4 billion in 2017.

This figure represented a CAGR of 3.5% from 2014 to 2017.

The main drivers for this expected growth are increasing younger generation demographic buyers with strong preferences for sustainable products.

Also, a Nielsen survey ‘found 48% of I.S. consumers said they are definitely or probably changing their consumption habits to reduce the impact on the environment. Millennials, at 75%, are more likely than baby boomers, at 34%, to say they are definitely or probably changing their habits to reduce impact on the environment.’

Major competitive or other industry participants include:

-

Kimberly-Clark (KMB)

-

Procter & Gamble (PG)

-

WaterWipes UC

-

Johnson & Johnson Consumer (JNJ)

-

Unilever (UL, OTCPK:UNLYF)

-

LVMH Moet Hennessy Louis Vuitton (OTCPK:LVMHF)

-

L’Oreal (OTCPK:LRLCF, OTCPK:LRLCY)

-

Pacifica Beauty

-

Estee Lauder (EL)

-

The Clorox Company (CLX)

-

Reckitt Benckiser Group (OTCPK:RBGPF, OTCPK:RBGLY)

HNST’s Recent Financial Performance

-

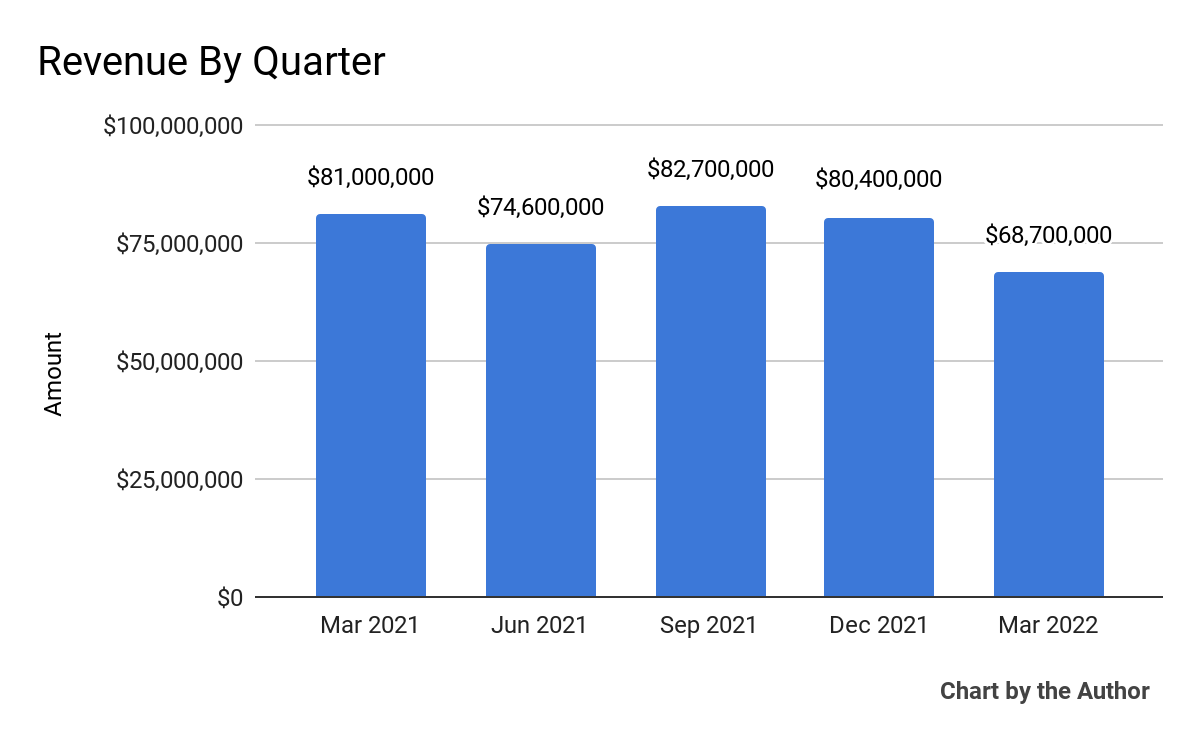

Total revenue by quarter has been largely flat or lower over the past several quarters:

5 Quarter Total Revenue (Seeking Alpha)

-

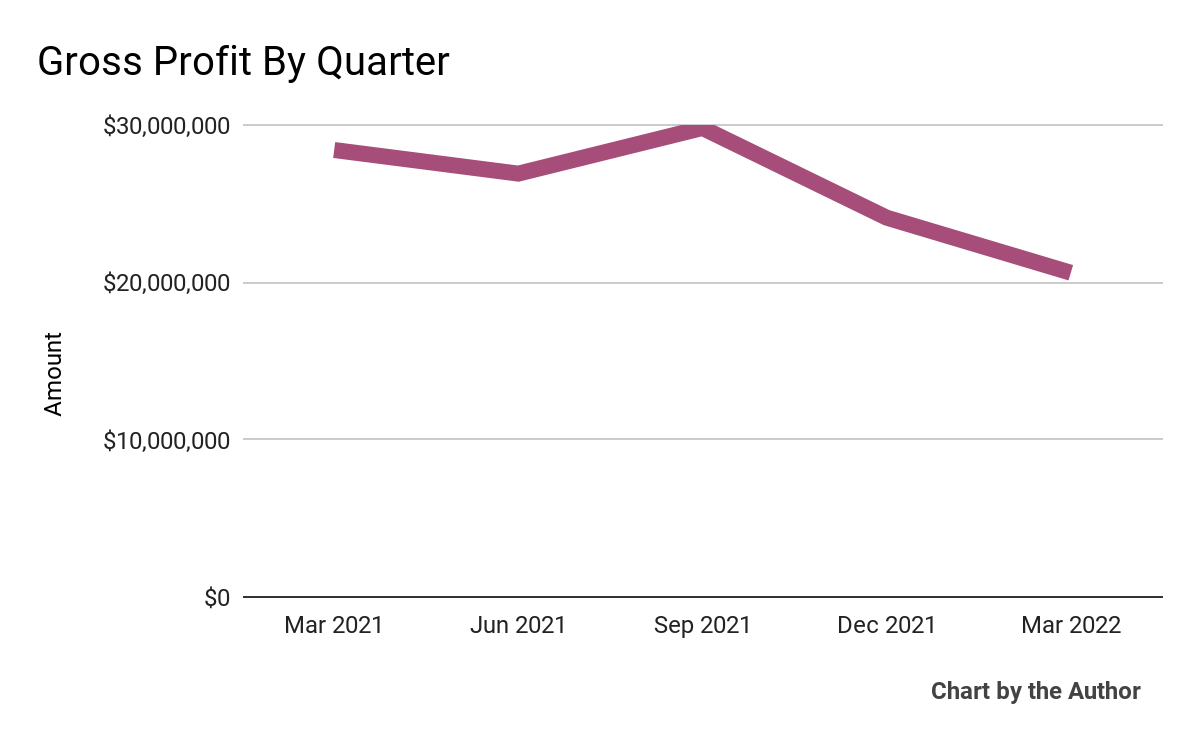

Gross profit by quarter has trended flat or lower:

5 Quarter Gross Profit (Seeking Alpha)

-

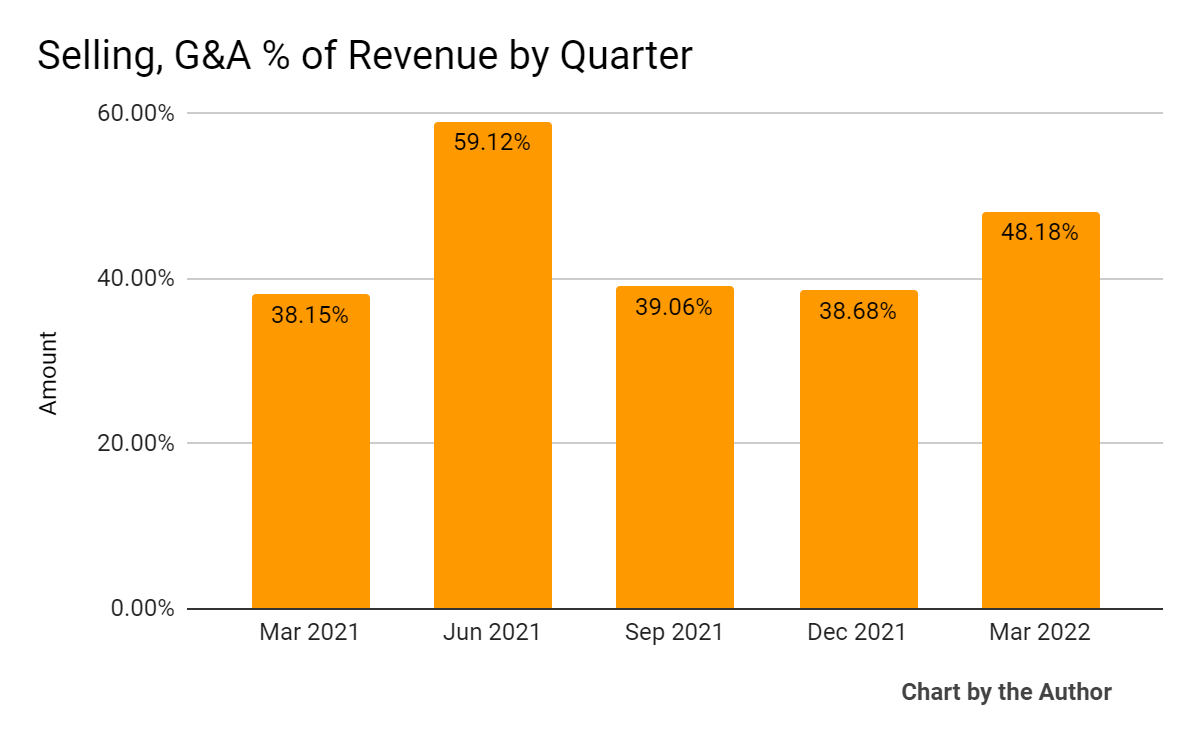

Selling, G&A expenses as a percentage of total revenue by quarter have fluctuated with no clear trend:

5 Quarter Selling, G&A % of Revenue (Seeking Alpha)

-

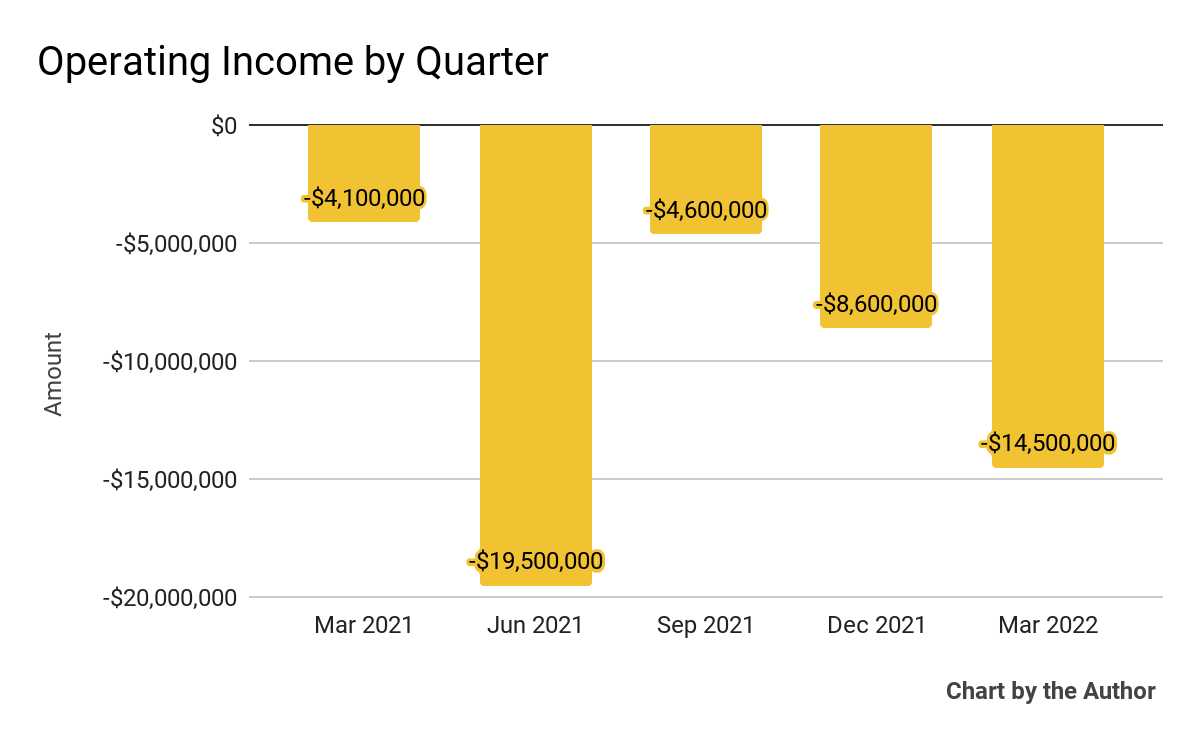

Operating income by quarter has remained negative and worsened in recent quarters:

5 Quarter Operating Income (Seeking Alpha)

-

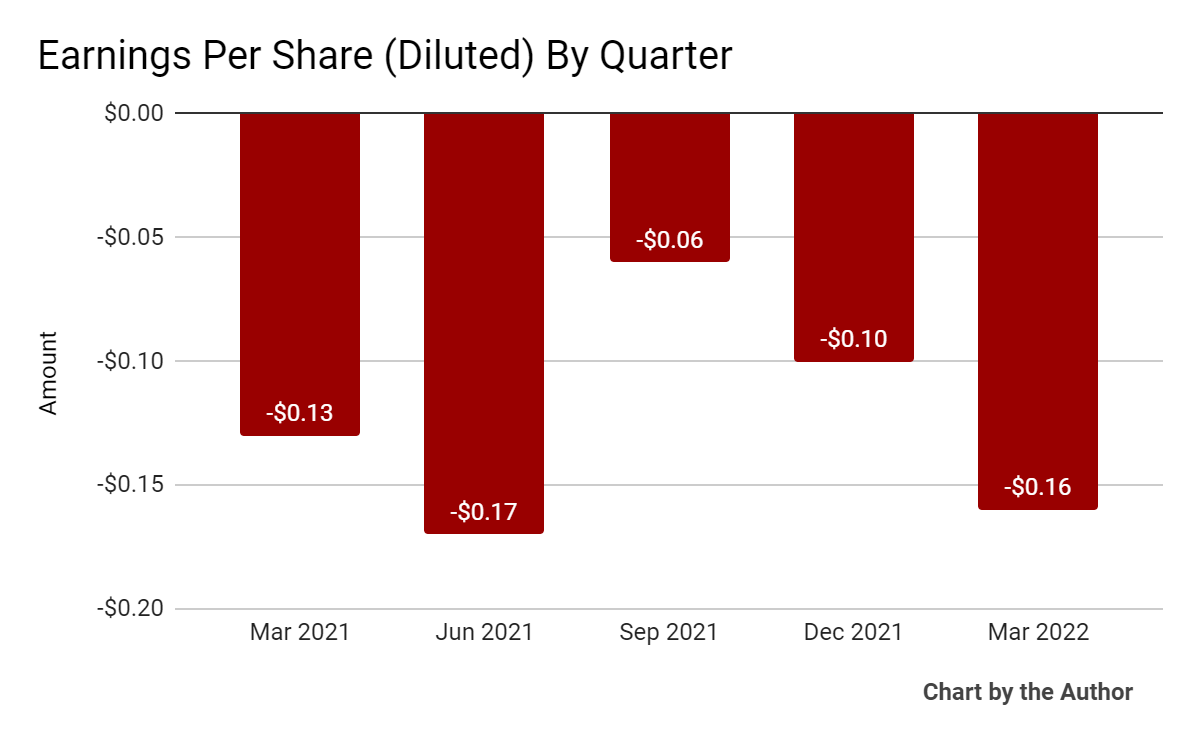

Earnings per share (Diluted) have also remained negative and worsened over the past several quarters:

5 Quarter Earnings Per Share (Seeking Alpha)

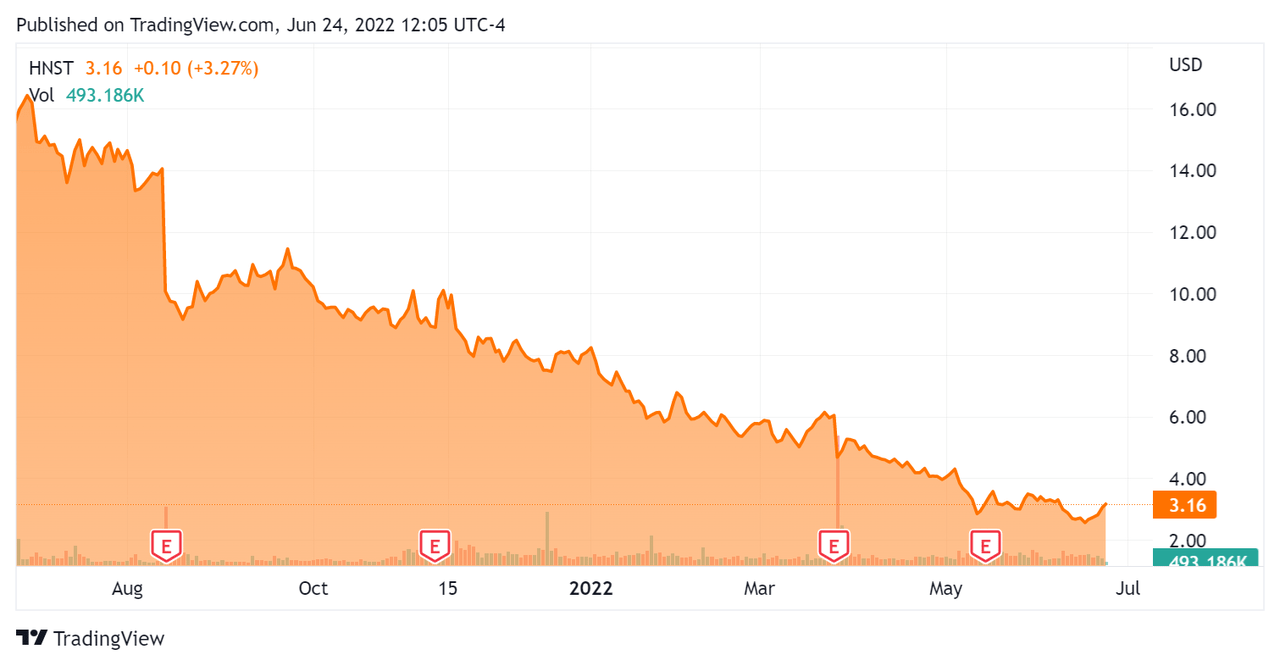

In the past 12 months, HNST’s stock price has dropped 79 percent vs. the U.S. S&P 500 index’ (SPY) fall of around 8.9 percent, as the chart below indicates:

52 Week Stock Price (Seeking Alpha)

Valuation Metrics For The Honest Company

Below is a table of relevant capitalization and valuation figures for the company:

|

Measure |

Amount |

|

Market Capitalization |

$281,910,000 |

|

Enterprise Value |

$247,150,000 |

|

Price/Sales (TTM) |

0.85 |

|

Enterprise Value/Sales (TTM) |

0.81 |

|

Operating Cash Flow (TTM) |

-$40,890,000 |

|

Revenue Growth Rate (TTM) |

-0.92% |

|

Earnings Per Share |

-$0.49 |

(Source – Seeking Alpha)

Commentary On HNST

In its last earnings call, covering Q1 2022’s results, management highlighted the reduction in consumer demand via the online channel as the pandemic has waned.

The firm plans to expand its retail footprint in response in order to tap greater consumer demand for in-store purchasing, post-pandemic.

As to its financial results, total revenue has been largely flat despite significant inflation “affecting every part of the P&L,” including labor, administrative, products, logistics and warehousing.

In response, the company has instituted mid to high single-digit price increases across its product portfolio.

As a result, the firm has seen a ‘modest decline in volume,’ but management expects volume to increase over time.

Looking ahead, management reconfirmed its full-year guidance ‘with mid-single-digit growth over the remainder of the year’ as it increased its strategic retail partner footprint.

Regarding valuation, the market is currently valuing HNST at an EV/Revenue multiple of around 0.8x.

This 0.8x valuation is significantly lower than the average of top U.S. publicly held Consumer Staples stocks with market capitalizations under $1.0 billion in size, which is currently around 2.3x EV/Revenue multiple.

The primary risks to the company’s outlook are whether it will be able to quickly ramp up its rebalance to retail, the impacts of continued inflation or if a recession occurs, the impact on volume and product substitutions.

An upside catalyst would be a “soft landing” for the U.S. economy, with stronger purchase volume later in 2022.

While the market is valuing HNST well below its consumer staple industry peers, for the time being, this valuation may be warranted.

However, for investors with a patient time horizon and an optimistic view of the U.S. economy’s ability to avoid a recession, HNST may be a candidate for “nibbling on” with a small position.

I’m more conservative, so I’m on Hold for HNST until it can show revenue growth and meaningful progress toward operating breakeven.

Be the first to comment