William_Potter

This article reviews the 2022 second quarter earnings and 2022 YTD performance of The Good Business Portfolio (My IRA portfolio). So far, this year is a bad year, down 14%: 0.62% below the Dow average. Good companies are coming back as their workforce returns. Earnings data for some of the top positions in the portfolio and recent changes to the portfolio are included in the earnings and company comments section. At present, it looks like the Republicans will take control of Congress, allowing them to reverse some of the economic policies of the present administration, giving the market an up movement in the next two-three months.

Guidelines (Company Selection)

The Good Business Portfolio guidelines are used to create a portfolio that is a large-cap balanced portfolio between the different styles of investing. Income investors take too much risk to get their high yields. Bottom-fishing investors get catfish. Value investors have to have the foresight to see the future. Over many years, I have codified 11 guidelines for company selection. These are guidelines and are not rules. For a complete set of guidelines, please see my article, “The Good Business Portfolio: Update to Guidelines, March 2020.” They are meant to be used as filters to get to a few companies on which further analysis is done before adding them to the portfolio. So, it’s all right to break a guideline if the other guidelines indicate a Good Company Business. I’m sure this eliminates some really good companies, but it gets me a shortlist to review. There are too many companies to even look at 10% of them.

You see from the portfolio below that I want a defensive portfolio that provides income and does not take significant risks. I limit the portfolio to 25 companies, as more than this is almost impossible to follow. I have 21 companies in the portfolio, so the portfolio has four open slots. I have not added any new companies during the last quarter and will most likely not add any for this year as I dint have enough cash right now.

Portfolio Performance

The performance of the portfolio created by the guidelines has, in most years, beat the Dow average for over 30 years, giving me steady retirement income and growth. The table below shows the portfolio performance for 2012 through 2021 and 2022 YTD. The chart data is after the close on September 2, 2022.

|

Year |

DOW Gain/Loss |

Good Business |

Beat Difference |

|

Portfolio |

|||

|

2,012 |

8.70% |

16.92% |

8.22% |

|

2,013 |

27.00% |

39.70% |

12.70% |

|

2,014 |

6.04% |

8.67% |

2.63% |

|

2,015 |

-2.29% |

5.68% |

7.97% |

|

2,016 |

13.38% |

8.68% |

-4.70% |

|

2,017 |

25.10% |

21.28% |

-3.82% |

|

2,018 |

-5.63% |

-4.33% |

1.30% |

|

2,019 |

22.33% |

24.19% |

1.86% |

|

2,020 |

7.25% |

10.72% |

3.47% |

|

2,021 |

18.73% |

19.49% |

0.76% |

|

2022 YTD |

-13.81% |

-14.44% |

-0.62% |

Source: Authors Chart

In a great year like 2013, the portfolio did fantastically. In a normal year like 2020, it beat the Dow by 3.47%. So far this year, the portfolio is behind the Dow by 0.62% total return below the Dow average loss of 13.81%, for a total portfolio loss of -14.44%, which is not good. With four months to go in the year and earnings increasing for the portfolio companies, there is the hope of a recovery in November. Also, the mid-term elections will be over to help stabilize the market. Boeing and General Electric have begun to recover some as the 787 is flying again, but BA missed expected earnings for the last quarter. This quarter we have another company that missed its earnings by 10%, and that is Freeport-McMoRan Inc. (FCX). FCX follows the price of copper, and right now, China and World politics are hurting copper demand. I believe that China will again grow at a projected rate of 6%, with copper should recover nicely within a year. The other good business companies are doing well, beating company earnings estimates, with HD, JNJ, and ADP leading the pack. Fundamentals will continue to shine this year and for years to come for the portfolio of good businesses to return to normal as the COVID virus continues to be controlled by the present vaccines, with new vaccines expected within a week tailored to the present dominant strain of the COVID virus (BA.4 and BA.5).

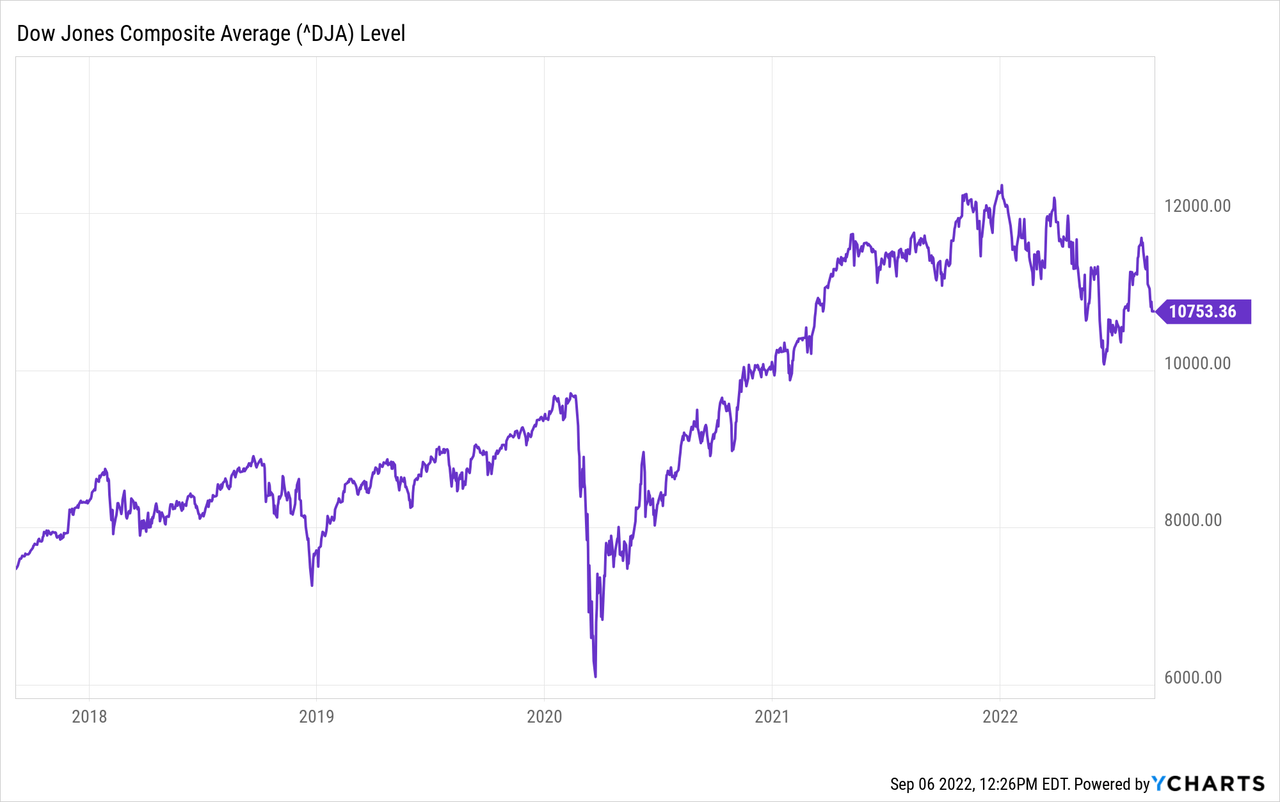

The graphic below shows the Dow average with some ups and downs. The Good Business Portfolio has some income companies and some stable low beta companies that balance the portfolio in down times and growth companies that fly in good times.

The graphic above shows the Dow average for the past five years, a good chart with nice gains as the United States economy was growing again until the war on fossil fuels was started. I have one question, what powers aircraft without fossil fuels, and where does the electricity come from to power all the electric cars and industry? California just announced that they are curbing the charging of electric cars since they don’t have enough capacity right now. How will it be in 2035 with almost all-electric cars in California?

Companies in the Portfolio

The 21 companies and their percentage in the portfolio and total return over an 80-month test (starting January 1, 2016, to 2022 YTD) period are shown in the table below. This time frame was chosen since it included the great years of 2017, 2019, and the average year of 2020, with other years that had a fair and bad performance. The Dow baseline for this period is 74.51%, and 14 of the positions beat or matched that baseline. There are seven companies that missed the Dow baseline by more than 10% but are still great businesses and will come back as the United States economy grows and the COVID virus is further controlled. I limit the portfolio to 25 companies and generally let the winners grow until they reach 8%-9% of the portfolio, and then I trim the position. The three companies in trim position are Home Depot (HD) at 10.1% of the portfolio and Johnson & Johnson (JNJ) at 9.10% of the portfolio, and ADP at 9.34% of the portfolio. I have been trimming HD and JNJ down to the 10% range of the portfolio to maintain diversification. I also have to sell at least 2% of my portfolio to cover my RMD for the year, and in a down year so far, this gives me very hard decisions.

|

DOW Baseline |

74.51% |

|||

|

Company |

Total Return 80 Months |

Difference From Baseline |

Percentage of Portfolio |

Cumulative Total Percentage of Portfolio |

|

Home Depot (HD) |

156.11% |

81.60% |

10.10% |

10.10% |

|

Automatic Data Processing (ADP) |

232.93% |

158.42% |

9.34% |

19.44% |

|

Johnson & Johnson (JNJ) |

85.53% |

11.02% |

9.10% |

28.54% |

|

McDonald’s Corp. (MCD) |

147.52% |

73.00% |

7.95% |

36.48% |

|

Texas Instruments (TXN) |

248.68% |

174.17% |

7.72% |

44.21% |

|

Eaton Vance Enhanced Equity Income Fund II (EOS) |

88.00% |

13.48% |

7.20% |

51.41% |

|

Walt Disney (DIS) |

32.28% |

-42.23% |

5.97% |

57.38% |

|

Trane (TT) |

290.24% |

215.72% |

6.73% |

64.11% |

|

Boeing (BA) |

53.53% |

-20.98% |

5.28% |

69.39% |

|

Omega Health Inv. (OHI) |

35.14% |

-39.38% |

6.87% |

76.27% |

|

Altria Group Inc. (MO) |

13.05% |

-61.47% |

4.57% |

80.84% |

|

Philip Morris INTL INC. (PM) |

41.73% |

-32.78% |

4.90% |

85.73% |

|

Digital Realty Trust (DLR) |

88.19% |

13.68% |

3.66% |

89.39% |

|

Freeport McMoRan (FCX) |

384.78% |

310.26% |

3.50% |

92.89% |

|

General Electric (GE) |

-68.54% |

-143.05% |

1.33% |

94.21% |

|

Danaher Corp. (DHR) |

303.42% |

228.91% |

1.67% |

95.88% |

|

American Tower (AMT) |

197.92% |

123.41% |

1.04% |

96.92% |

|

Realty Investors (O) |

57.88% |

-16.63% |

0.80% |

97.72% |

|

Lockheed Martin (LMT) |

124.29% |

49.77% |

0.86% |

98.58% |

|

Visa (V) |

172.78% |

98.27% |

0.41% |

98.99% |

|

PepsiCo Co. (PEP) |

101.33% |

26.82% |

0.80% |

99.79% |

|

Average Above Dow |

58.19% |

Source: Authors Chart

Therefore JNJ, ADP, and Home Depot are now in a trim position, but I am letting JNJ run a bit to 10% of the portfolio since it is a great defensive medical supply business. I start the companies at a base percentage of the portfolio of close to 1% and add to the position if they perform well during the next six months. At 4% of the portfolio, I stop buying and let the company percentage of the portfolio grow until it hits 8%; then, it is time to consider trimming (reducing position by 0.5% of the portfolio) the position.

The above is the full list of my 21 Good Business positions. I have written individual articles on all these businesses.

Earnings and Company Comments

For the second quarter earnings season, the 21 portfolio companies did very well, considering the conditions created by the virus and the government. Eighteen companies beat or met earnings estimates and three below estimates (BA, FCX, LMT). The good businesses are holding up well, and many have had increases in their target prices. Now on to some of the companies that beat earnings and three that missed earnings.

On 8/16/2022, Home Depot earnings were expected at $4.97 and came in at $5.05, and compared to last year at $4.53, a great quarter Y/Y. Revenue beat compared with expected by $460 million. Total revenue was $43.79 billion, up 6.5% Y/Y. HD had a great report, showing growth even in this pandemic environment. HD has been trimmed to 10% of the portfolio to maintain diversification. HD is a great business, but it must start to expand its foreign business to get good growth going forward. They held up well during the COVID-19 virus slowdown, and the company is a solid investment long term. S&P CFRA one year price target on HD is $375. Home Depot is a buy as the market dip gives us a buying opportunity at a low bargain price and a 31% increase to the target.

A SWAN-type company I have in the portfolio is JNJ, with 61 years of dividend increases. On 4/19/22, Johnson & Johnson’s earnings were above expected at $2.59 compared to last year at $2.48 and expected at $2.57. Revenue beat expected revenue by $180 million, with total revenue up 3% to $24 Billion. They are still growing and have plenty of cash to buy companies and continue their growth. JNJ will be pressed to 10% of the portfolio because they’re so defensive in this COVID-19 Virus world. JNJ is not a trading stock but a hold forever a SWAN. If you want a hold forever top-notch medical supply company with a growing 2.6% dividend (61 years of increases), JNJ is a buy.

ADP is not an exciting investment, but it is a growing company with 47 years of increasing dividends. On 7/27/22, Automatic Data Processing earnings were above expected at $1.50 compared to last year at $1.20 and expected at $1.46. Revenue beat expected revenue by $80 million, with total revenue up 11.6% at $4.13 Billion. Automatic Data Processing’s total return outperformed the Dow average for my 80-month test period by 158.42%, which is great, and the present entry point is fair for a buy by the conservative growth and income investor, with a 1% year gain to the S&P CFRA price target of $242. ADP is 9.43% of the portfolio, and it may be trimmed to 8% to help me pay my RMD this year.

An interesting company I have as an income producer is OHI, a REIT in the nursing home business. They are good at managing the selling and buying of nursing home properties. The COVID virus has hurt OHI for the last two years, and the dividend increases have stopped because the virus is hurting their business. The company’s last quarter’s earnings, released on August 1, were fair at $0.76 FFO, beating expected by $0.02 and compared to last year at $0.75. The dividend is $0.67/Qtr. and the management is fixing the tenants that are having financial problems. OHI has taken steps to fix the losing operators by selling properties, moving properties, or changing the rental agreement. OHI has been there before and has shown they can fix this problem but may need a few more quarters. For me, OHI is a buy as the COVID virus is controlled in their business, and the senior citizen population will grow for many years as you collect an 8.3% yield. The vaccination rate in nursing homes is high, but there is always the possibility that a new strain of COVID that could hit. I think the pressure from COVID presents a buying opportunity to buy an income company at a fair price in a growing business for the investor that has patience and can take some risks.

Boeing is having the worst spell of incidents in many years between the COVID dip and problems with the 737 and 787 planes. Boeing has dropped from over $400 to around $150 today. It’s hard to believe that just about 2.5 years ago, I sold some BA at over $400. My position now is a buy as we watch the great Boeing business return to normal over the next two years as the pilots start to return and airlines need new planes. The 787 has started shipping and should really help the bottom line and cash flow, with 79 planes expected to ship in the next few months. On July 27, Boeing’s earnings were -$0.37, below the expected of -$0.05, and revenue was down 1.8% YOY at $16.7 billion and missed expected revenue by $830 million. This was a bad report, but the business is getting better with many new orders and demand for new planes increasing. S&P CFRA has a one-year target price of $252 or a gain of 67%. The commercial airline business is on the mend giving a value play on a great business at a bargain price.

Lockheed Martin, the largest manufacturer of military defense systems and other non-defense government systems, is a buy for the dividend income and future total return growth investor. Lockheed Martin has a good cash flow, and the company uses some of the cash to expand its product line. The remainder of the cash is used to increase dividends each year and buy back shares raising the stock price. Lockheed Martin’s dividend yield is above average at 2.7% and has been increased for 20 years in a row. A solid dividend income company. The five-year dividend growth rate is 9%, which grows your income each year. On July 19, LMT reported earnings of $6.32 compared to expected of $6.39, a slight miss, and last year at $6.52. Revenue was $15.4 billion, down 9.3%, and missed expected by $570 million. They have recently received a $7.6 billion dollar order for 129 F-35 fighter jets, which should keep LMT healthy for many years. Lockheed Martin’s total return outperformed the Dow average for my 80-month test period by 49.77%, which is great, and the present price presents a nice entry point with a solid F-35 backlog.

The third company to miss expected earnings is Freeport-McMoRan, which engages in the mining of mineral properties in North America, South America, and Indonesia. The company primarily explores copper, gold, molybdenum, silver, and other metals. FCX follows the copper price up and down, and right now, China, which is the major user of copper, has COVID lockdowns that are causing the price of copper to drop. The long-term need for copper will be driven by electric cars and trucks and other infrastructure development that need a good supply of copper. I rate FCX as a buy during this downturn for the investor that wants a large gain as COVID BA.5, and BA.4 vaccines start to control the present majority of the cases. On July 21, FCX reported a bad earnings report. FCX reported earnings of $0.58, missing expected by $0.08, and compared to last year at $0.77, a strong drop YOY. Revenue was also lower at $542 million, down from last year by 5.7% and missed expected by $720 million. Now is the time to be brave and buy FCX at a low price.

Portfolio Management Comments

I did not sell during the COVID decline and watched the market recover as the United States economy started to grow again. The good businesses in my portfolio have gone up with the increase in the economy and the excellent reported earnings of the portfolio companies. The market has recovered from the COVID-19 virus dip, with the future looking good with people returning to work and school. We now have three vaccines that allow the United States to have a vaccine shot for all who want it. The big pharma companies have developed a vaccine tailored to the BA.4 and BA.5 strain that is presently spreading around the world and is about 90% of the cases in the United States. As herd immunity starts, the spread of the virus will strongly decrease, allowing the remaining workers to go back to work, which has started as shown by the labor increase in jobs added each month. Each quarter after the earnings season, I write an article giving a complete portfolio list and performance like this article.

Conclusion

The 11 guidelines referenced in the article give me a balanced portfolio of good companies that are large-cap and can grow their revenues, earnings, and dividends for years. They have the staying power to fix whatever goes wrong. In each case, the company has the size and good management to fix the problem. The portfolio has growth companies, defensive companies, income companies, and companies with international exposure, giving it what I call balance. Of the 21 companies in the portfolio, seven are underperforming the Dow average in total return by more than 10% over my 80-month test period, but the total return for the complete portfolio has beaten the market in 8 of the last 11 years by a good amount (see table above).

The portfolio is 0.62% lower than the Dow average YTD, with increases in earnings expected in the third quarter for almost all the portfolio companies. When the FED rate increases stop, I believe my great portfolio businesses will rocket ahead as they have done in previous good years. I intend to continue writing separate comparison articles on individual companies. I have written articles on all of the companies in the portfolio and others, and you can read them in my list of previous articles if you are interested. If you would like me to do a review of a company you like, please comment, and I will try to do it.

Be the first to comment