We Are

In another positive sign for January, the major market averages logged healthy gains for the first five trading days of the year. Yet institutional and retail investors have been net sellers of stocks every day in what was the largest weekly outflow since November for Bank of America’s clients. They must be listening to the hawkish commentary from Fed governors in recent days, who continue to preach higher for longer when it comes to short-term interest rates. JPMorgan’s CEO Jamie Dimon joined the fray again yesterday, asserting that rates might have to rise higher than what investors expect. In my opinion, stocks are grinding higher on data that points to a faster deceleration in the rate of inflation than the consensus expects.

finviz

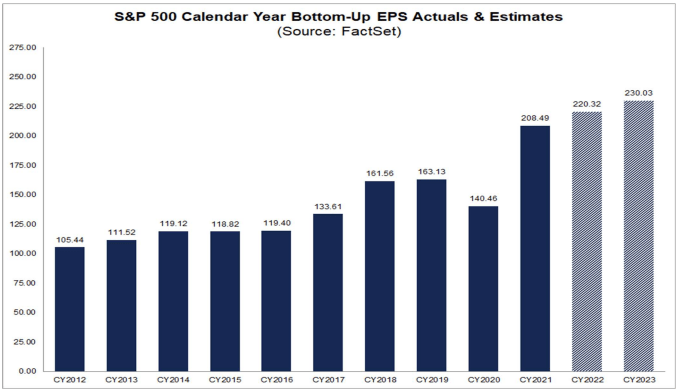

We will find out who is right tomorrow morning with the arrival of the Consumer Price Index report for December. Then the focus will swing to corporate earnings reports on Friday when several big names are scheduled to announce numbers. Analysts have been reducing estimates for several months to what is now expected to be approximately $220 for the S&P 500 in the year just ended and $230 in 2023, which implies a growth rate of 4.5%.

FactSet

That results in a forward multiple of 16.9 times, which is slightly below the 10-year average of 17.1. Given that long-term interest rates, as measured by the 10-year Treasury yield, are well above a 10-year average that was below 3%, I’d say the S&P 500 is fairly valued here at best. That said, the opportunities for investors are in sectors and stocks rather than the broad index. I do not see significant upside for the index as money continues to flow from growth to value, but there is still room for modest upside as the year progresses. Consider the possibility that Europe does not go through a recession this year, as Goldman Sachs now projects, and that China emerges from its Covid restrictions with better growth in the second half of this year than the consensus expects.

Bloomberg

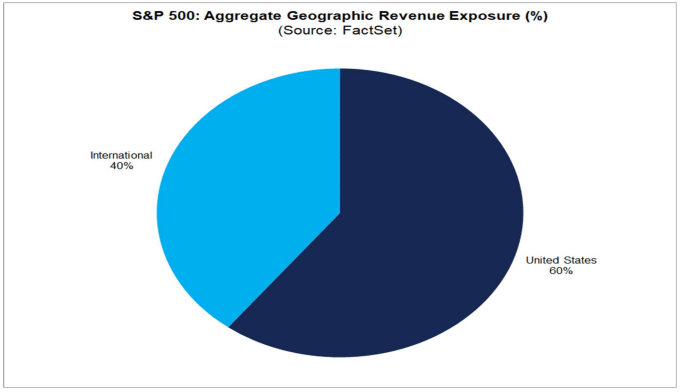

Better growth out of Europe and China should give the 40% of S&P 500 revenues that come from outside the US a significant boost.

FactSet

Then there is the benefit of a weaker dollar, which will show up in the second half of this year provided the dollar remains stable, or continues to weaken, which is my expectation. The dollar was up 8.8% in the quarter just ended on a year-over-year basis, which will be a stiff headwind for companies that derive a meaningful percentage of revenue from overseas. That reverts to a tailwind when the year-over-year increase becomes a year-over-year decrease.

Stockcharts

Lastly, most companies in the S&P 500 took meaningful cost-cutting steps in 2022 to head off the inflation that ravaged their bottom lines in expectations that price increases would remain higher for longer. Those cost cuts should pay dividends in 2023, especially if the rate of inflation falls more rapidly than most expect, which could result in better margins. These would all be very positive developments that the market is likely to reflect well before the market strategists on Wall Street factor them into their outlooks. The market is the best leading indicator, which is why I continue to listen to the market.

Lots of services offer investment ideas, but few offer a comprehensive top-down investment strategy that helps you tactically shift your asset allocation between offense and defense. That is how The Portfolio Architect compliments other services that focus on the bottom-ups security analysis of REITs, CEFs, ETFs, dividend-paying stocks and other securities.

Be the first to comment