Win McNamee

After several attempts to rein in the stock market, the Fed may have figured it out. The message was clear enough for a golden retriever (I have two) to understand. There was nothing cryptic or reading of the tea leaves to understand it.

Powell struck the point again, reiterating his stance at Jackson Hole about his commitment to reining in inflation, which would create below-trend growth rates and higher unemployment. What solidified this commentary was the FOMC summary of economic projections, which laid it all out very nicely.

There was nothing the equity market could cling to that it could twist and turn to make up some bullish narrative. It was what the Fed needed to deliver for financial conditions to tighten adequately and for the Fed to start to bring inflation down.

Federal Reserve

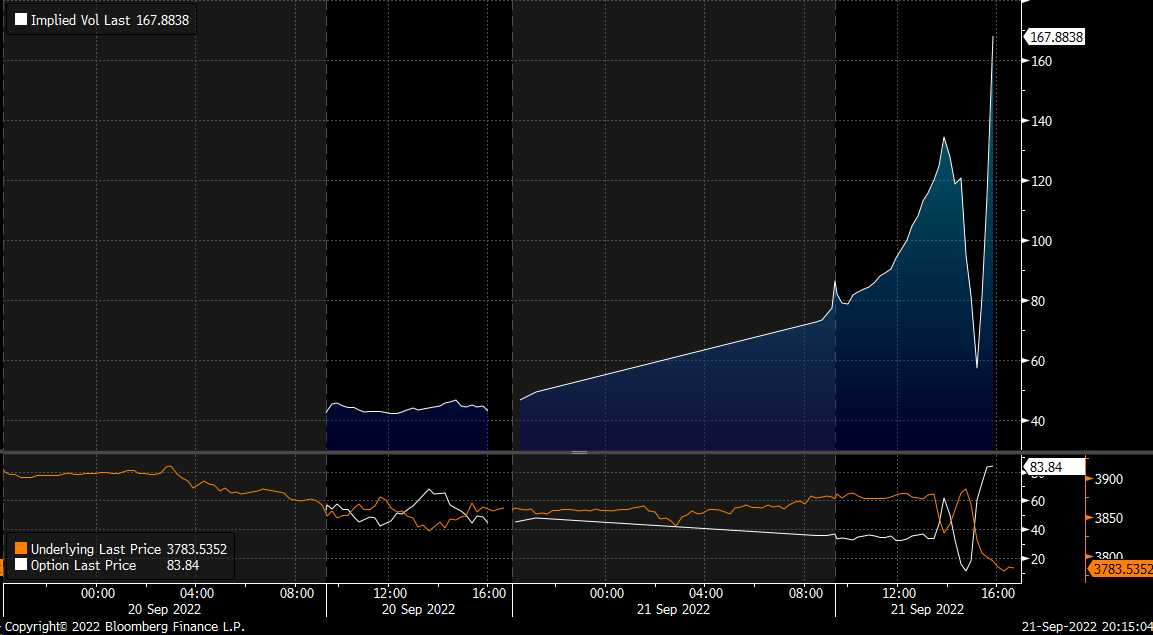

Old Games Didn’t Work

Of course, the equity market tried to play its implied volatility melt in the middle of the trading session game, with the S&P 500 managing to rally by more than 2% off its post-FOMC lows. But still, what became clear was that sellers were in the market, and they could offset that usually implied volatility melt and sink stocks.

Bloomberg

Rates Will Go Much Higher

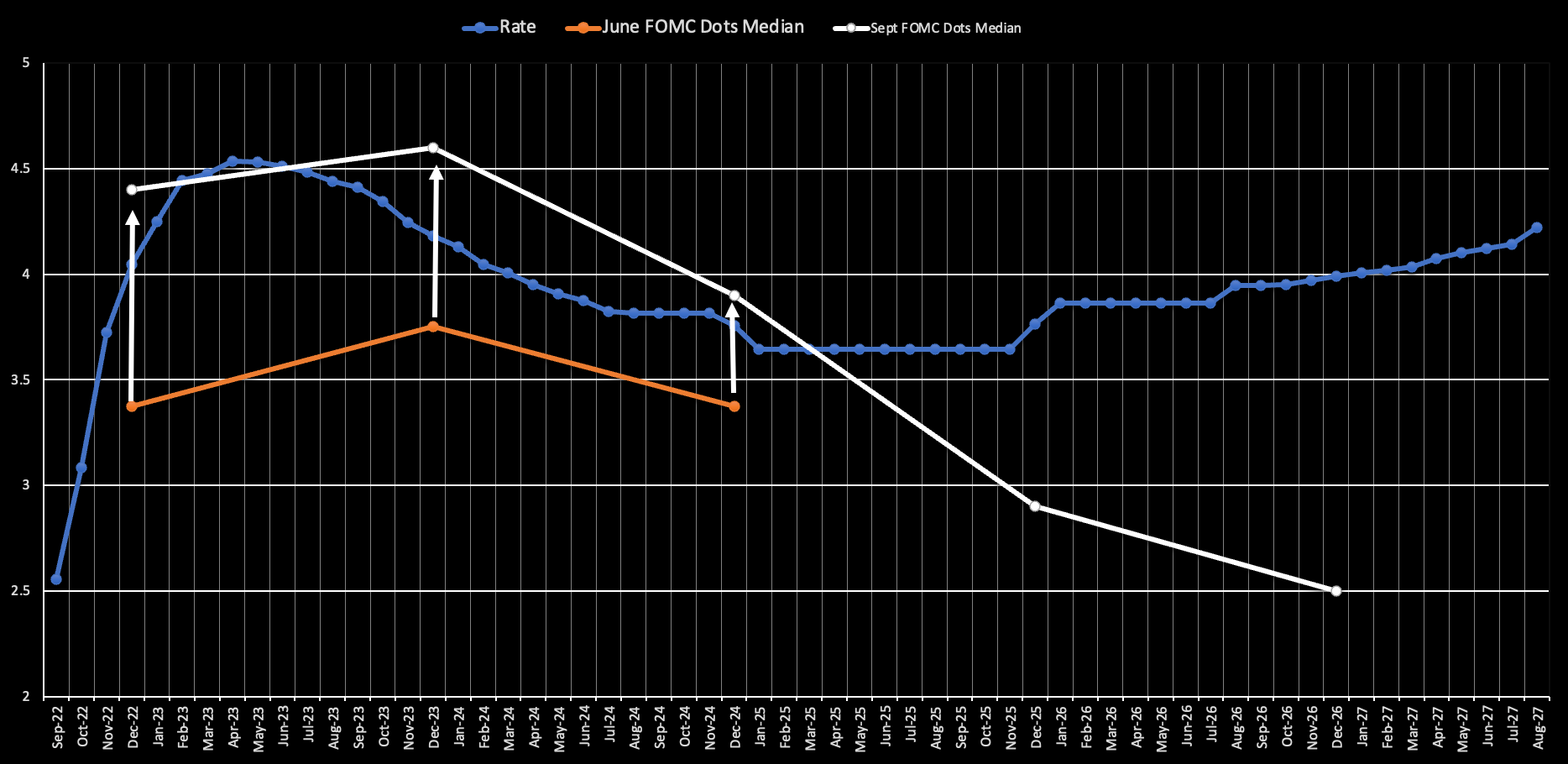

The Fed’s plan to get rates to 4.4% this year was just too much for the stock market and not expected. Fed Fund Futures were only looking at 4% rates by December 2022. The Fed’s projections were 40 bps higher than the market and about 1.25% higher than the Fed Fund Rate following today’s 75 BPS rate hike. That means the market will need to price two additional rate hikes for the rest of 2022.

The Fed’s projections for 4.6% for 2023 have also shifted the Fed Funds Futures peak terminal rate to 4.62% from 4.48% yesterday. Additionally, that peak rate is expected to come in May 2023 instead of April. But more importantly, as time passes, we should see those Fed Funds Futures begin to take the shape of the Fed’s expected path.

Mott Capital

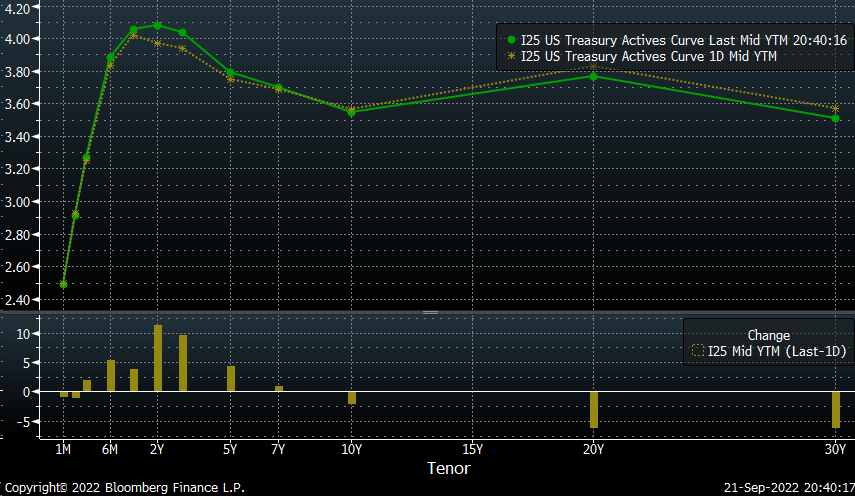

The shift in the futures market should feed through to the Treasury curve. Treasuries are already beginning to rise further with the 2-Yr and 3-Yr gaining and now above 4%. Based on the Fed projections, they would suggest we’re likely to see the two and three-year Treasuries not only stay above 4% but well above 4%, potentially matching those peak terminal rates of 4.6% the Fed is forecasting.

Bloomberg

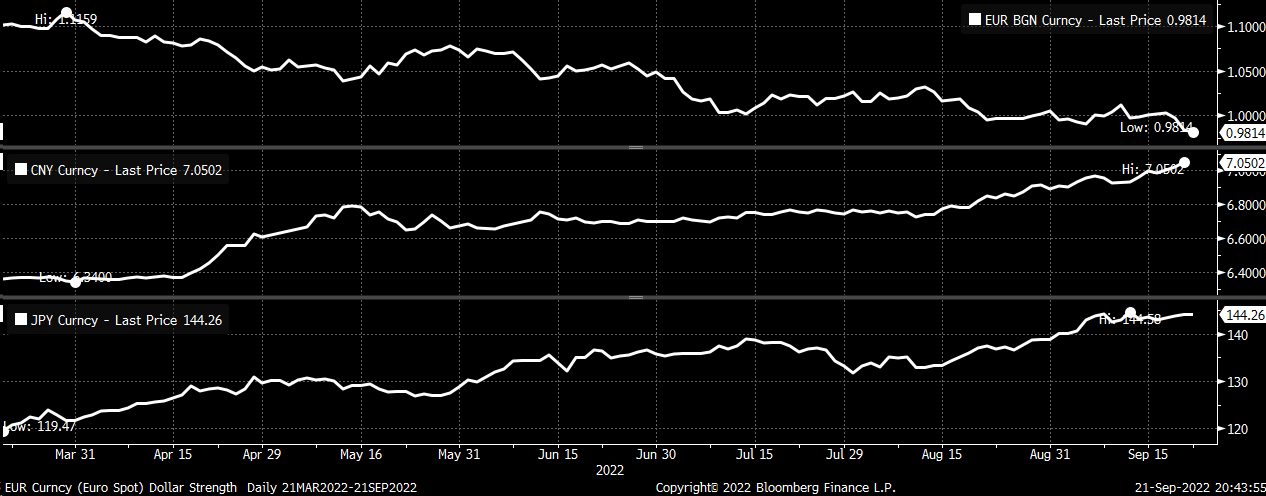

The higher rates will help strengthen the dollar index, especially against Japan and China, which are clearly in much easier monetary policy positions. Additionally, with Europe’s energy crisis and on the brink of recession, the dollar is likely to strengthen further against the euro.

Bloomberg

Tighter Financial Conditions

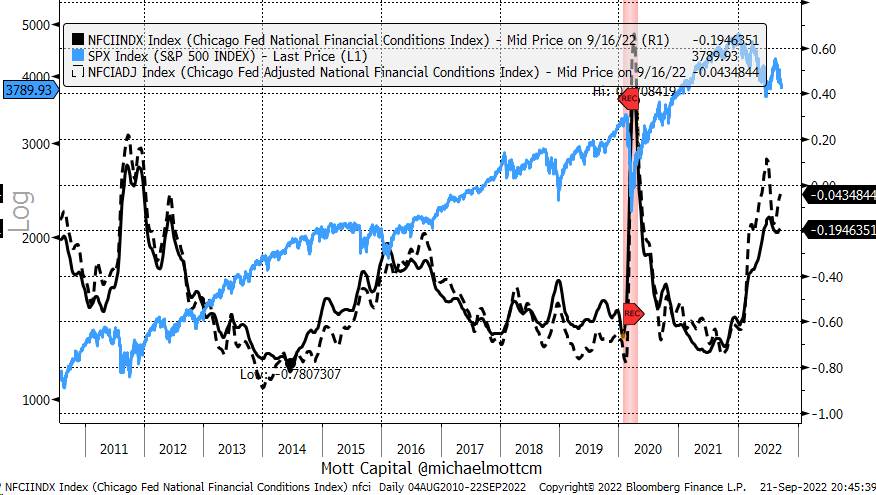

Rising rates and a stronger dollar also will help real yield rise, and together all of these things will work to tighten financial conditions even more in the coming weeks. While the Chicago Fed’s National Financial Conditions (NFCI) and Adjusted NFCI tightened some this week, they still need to see their index value get above zero. Tightening financial conditions will work to sink stocks as they usually do.

Bloomberg

Wider Spreads

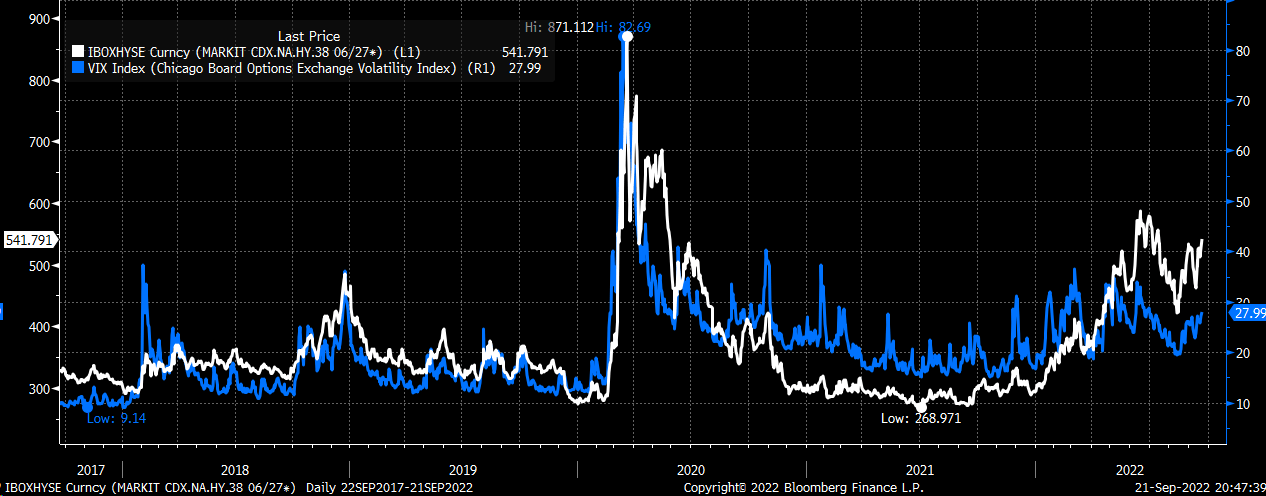

Additionally, corporate and high-yield credit spreads should widen further, which historically is directly tied to changes in the stock market volatility as measured by the VIX index. Plus, now that the VIX options expiration occurred on Sept. 21, the VIX will be able to move higher more freely and will not be tied to the lower levels due to option positioning.

Bloomberg

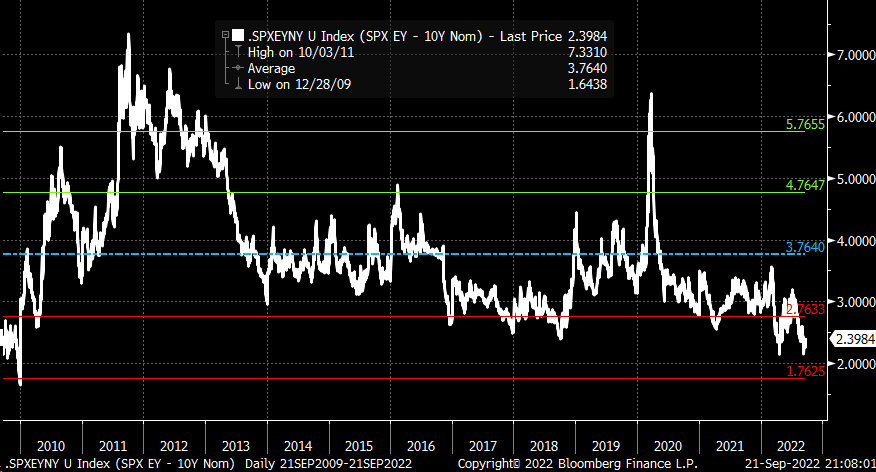

All of this is bad for stocks because, on a relative basis, the S&P 500 already is expensive, with an equity risk premium over the 10-Yr of just 2.4%. That’s a historically low level since 2010 and 135 bps below the historical average of 3.76%. An increase of 135 bps in the S&P 500 earnings yield would send it to roughly 7.25% from around 5.9%. That would take the S&P 500 PE ratio of 16.9 to approximately 13.8, or an S&P 500 value of roughly 3,100. That would be an additional 18% lower than its closing price of about 3,790 on Sept. 21.

Bloomberg

But that’s the thing – it all depends on where rates go because if rates do rise as the Fed suggests, and the 2-yr gets to around 4.5% and assuming the curve remains inverted by 50 bps, the 10-Yr would trade with a 4% yield, and then, of course, that would imply an even higher earnings yield for the S&P 500, and lower PE ratio.

Very Serious

The Fed is dead serious about raising rates. I have been warning about the end of QE and rate hikes and the consequence for about a year. As I also explained, the July and August 2022 rally was a giant head-fake, and it got many investors on the wrong side of things, believing the Fed would cave and pivot. This time is different; the Fed has a serious inflation problem for the first time in about 40 years. During the 2010s, the Fed only had to worry about the unemployment rate because inflation was nonexistent, so that it could pivot at the first signs of slowing growth.

But now inflation is job number one for the Fed, and everything else is a distant second.

Be the first to comment