RachelMcCloudPhotography/iStock via Getty Images

This was originally published for subscribers of Reading The Markets, an SA Marketplace service, on January 22, 2022.

This week will be the all-important FOMC meeting, and while stocks are oversold, it is important to remember they can grow more oversold. So, these are tricky times. The S&P 500’s RSI fell below 30 this week for the first time since the March 2020 sell-off. But it is important to remember that the S&P 500 also lost nearly 30% after reaching oversold conditions and traded below its lower Bollinger bands throughout most of the process.

I’m not trying to suggest we face a 30% decline here, in the same manner as in March 2020. I am just trying to stress that markets can fall sharply despite being oversold.

TradiingView

Here We Are

Additionally, markets are used to getting their way like any 2-year-old child. But as any parent knows, by constantly caving into your child, you are conditioning them and making the situation worse. The Fed has conditioned the stock market in the same way, but this time, the Fed won’t be able to give the baby its bottle just because it is having a literal meltdown.

We have been talking about it for months, and more recently, how the stock market was digging its own grave by endlessly rising since the Fed first announced QE was ending at Jackson Hole. That slowing GDP growth and earnings growth could not support the high multiples of the stock market. That tighter monetary policy would tighten financial conditions, reduce leverage, and cause multiples to contract. Well, here we are.

The Fed Put Is Dead

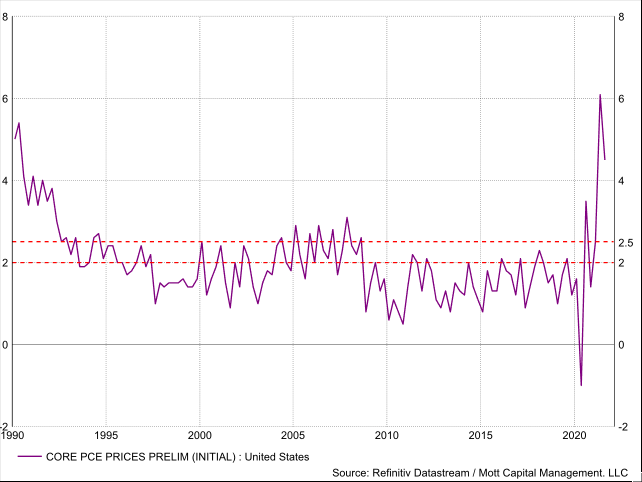

Investing based on the Fed saving the stock market is not investing at all. It is essential to realize that this time the Fed cannot just rush to the aid of the stock market. This time is different. Since the great financial crisis, this is the first time that core PCE is running above the 2 to 2.5% band. It is the first time the core PCE has been running meaningfully above the 2 to 2.5% inflation band since 1992. That means the Greenspan put is essentially dead.

Datastream/Mott Capital

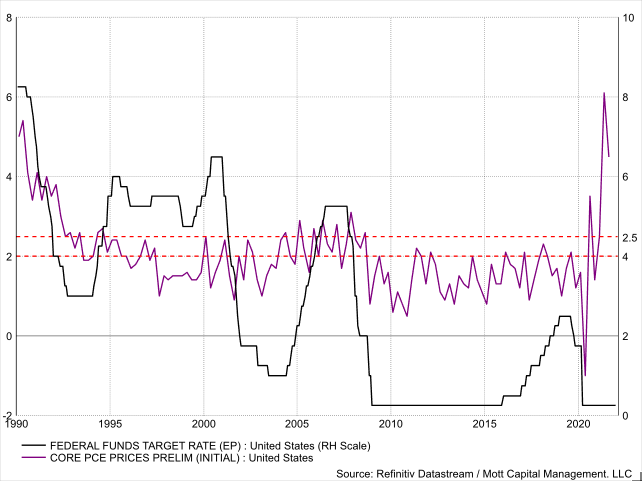

The Fed put has always worked because inflation was never an issue, which meant the Fed could always lean on slowing economic growth and the potential harm it could cause its other mandate – full employment. But now that employment is full and prices aren’t stable, the Fed needs to act on that price stability mandate. The Fed can’t hide behind global growth concerns to pivot. Every time the Fed has gone through a rate hike cycle, inflation was never the underlying issue.

Datastream/Mott Capital

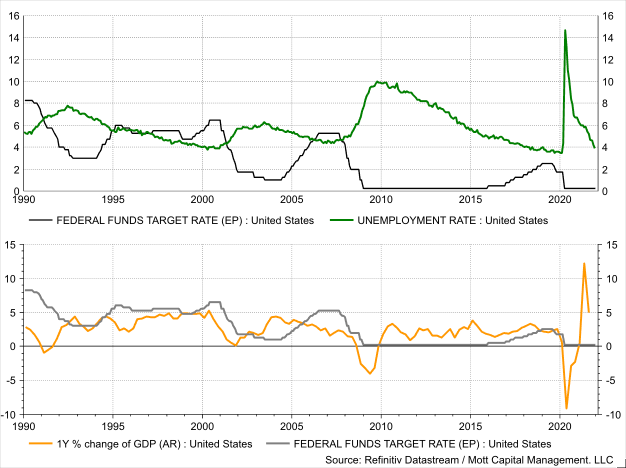

In prior cycles, rate hikes could be delayed due to the fear that the stock market was picking up on slowing growth or rising recession risks. Slowing GDP growth and recessions have a direct impact on unemployment rates. So, it would only make sense for the Fed to hold back or reverse course when markets were falling. But again, this time is different because we have full-employment and solid GDP growth.

Datastream/Mott Capital

But the only way to control inflation is to decrease demand and slow the economy, outside of the supply-chain suddenly improving. The Fed can do that by raising rates and tightening financial conditions; the two things that will kill the equity market.

Don’t Expect A Pivot

It is important to realize that the Fed will not suddenly pivot at January’s FOMC meeting and walk back its now aggressive stance on inflation because the S&P 500 is down 8%. It will take a much further drop in the market to get the Fed to back off its rate hike plans.

Perhaps that is what the Fed ultimately wants. The Fed has a way of getting the markets to do what it wants without even changing monetary policy, just by the threat of acting. Talking up the tapering of QE resulted in nominal rates rising and the dollar strengthening. The talk of raising rates has helped to push the front end of the yield curve even higher, but the long end of the curve is low, flattening the curve. Meanwhile, the threat of rolling off the balance sheet now has real rates rising. The rise in real rates is repricing riskier assets, specifically equity prices.

May Not Need To Raise Rates Even Once

We know the Fed intends to tame inflation and pull it down, well if it can get the markets to do all the dirty work for it, it may ultimately be what the Fed wants and may end up not having to raise rates one time to do it.

So don’t be so sure the Fed is going to be less hawkish this week and just rush to the aid of the stock market. It may be the case that stocks will need to fall much further first, with the pivot not happening until the March meeting. Especially, if the Fed can accomplish what it really wants, lower asset prices.

Be the first to comment