Adam Gault/OJO Images via Getty Images

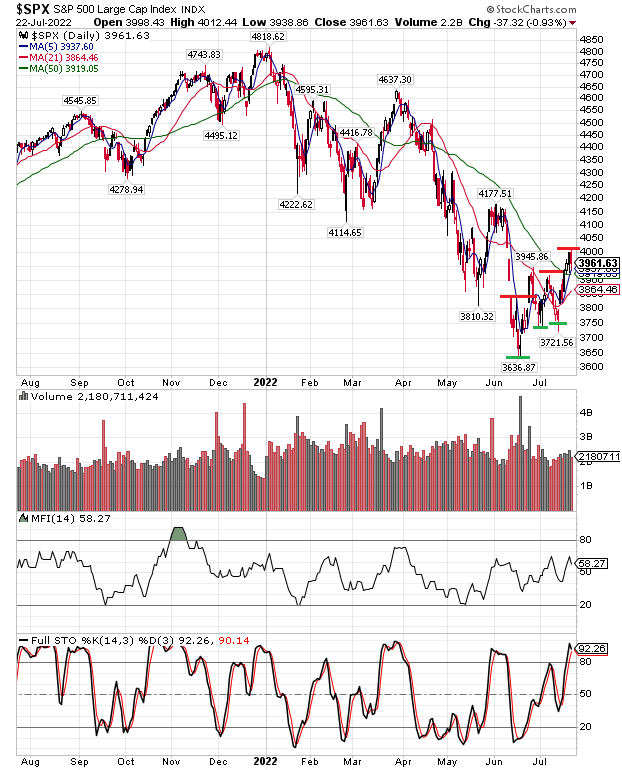

The S&P 500 Index closed out the week ending July 22 with a gain of 2.57%. Since mid-June, the weekly return for the market has alternated between a positive and negative result. During this back and forth though, the Index has been making higher lows followed by higher highs since mid-June. This followed my article dated June 21, “Might An Equity Market Bottom Be Near“, and since that time, the Index is up nearly 8%.

S&P 500 Large Cap Index (StockCharts.com)

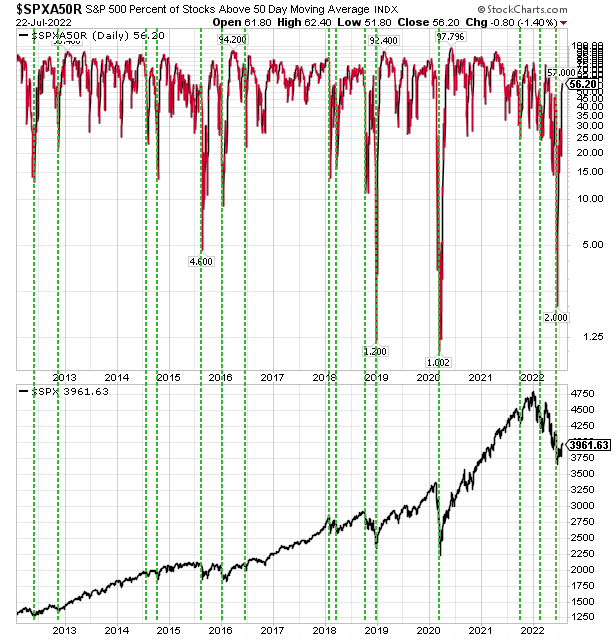

The other observable aspect of the above chart is the fact that the S&P 500 Index is now trading above its 50-day moving average. If one reads the earlier article noted above, at the time that article was written, only 2% of S&P 500 stocks were trading above their 50-day moving average. As of Friday’s close, the percentage has increased to 56% and the S&P 500 Index has increased from 3,674 to 3,961.

Percentage Of S&P 500 Stocks Above 50-Day Moving Average (StockCharts.com)

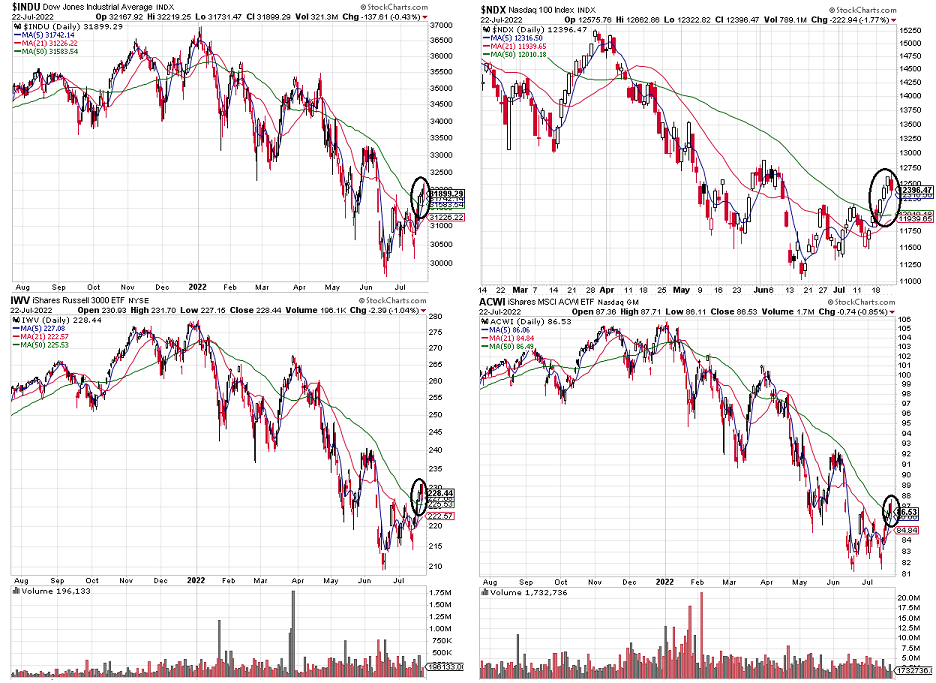

Many other indexes are showing technical improvement as well and are trading above their 50-day moving averages. A few are displayed below. This change in trend is certainly a positive one and is an indication of investors’ increased appetite for risk.

Dow Jones Industrial Average, Nasdaq 100, IWV, ACWI – All Showing Technical Improvement, Above 50-DMA (StockCharts.com)

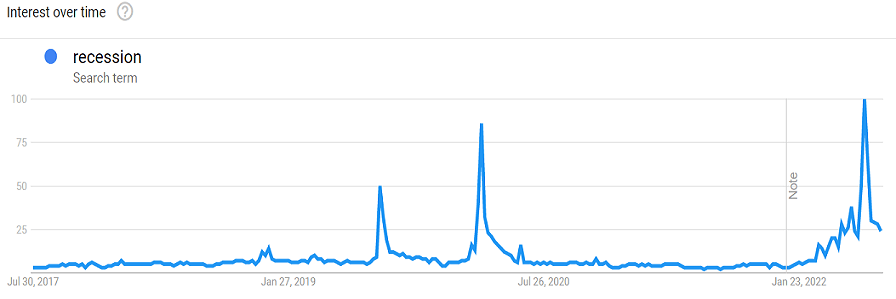

It is nearly impossible not to hear the heightened discussion about the economy headed for a recession. In fact, it is quite possible that the economy is already in a technical recession, i.e., two consecutive quarters of negative real GDP growth. With this type of focus and widespread dissemination about a recession, then, the impact of a recession on the market tends to get reflected in asset prices, since it is widely known news.

Google Trends Results For Search Term “Recession” (Google Trends)

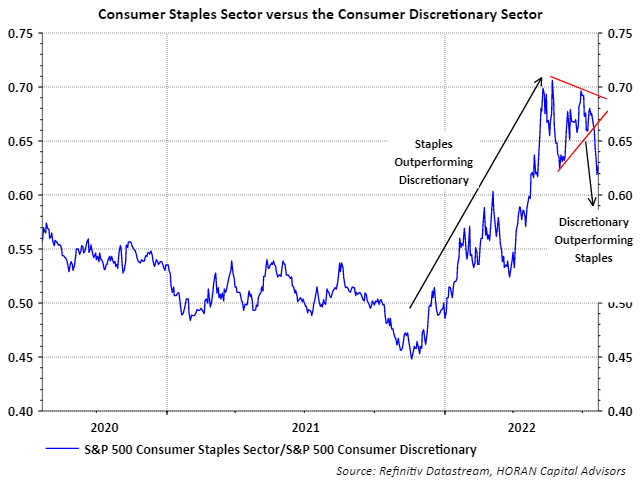

One market segment that tends to do poorly leading up to and into a recession is the consumer discretionary sector. Coming out of a recession though, broadly speaking, discretionary stocks tend to be a leader. Contrast this with the consumer staples sector, which tends to be more defensive, as companies that comprise the sector tend to sell products consumers need regardless of the economic environment. Since the beginning of this year, the consumer discretionary sector has been one of the worst-performing ones, second only to the communication services sector. From the start of the year through mid-June, the discretionary sector was down 34.7% versus the consumer staples sector being down 11.2%. Since mid-June though, the more economic sensitive consumer discretionary sector is up 15.4% and consumer staples are up only 6.5%. This outperformance appears to be the beginning of a potentially longer-lasting outperformance trend, as the blue line on the below chart has broken out of a wedge pattern, indicating an outperforming discretionary sector.

Performance Of Consumer Staples Vs. Consumer Discretionary (Author)

The equity market may not be out of the woods yet and does seem a little overbought after being up almost 8% since its June 16 low. Much discussion is taking place about earnings for companies and this being the next shoe to drop and create a headwind for the market as the economy slows. Earnings results are expected from some technology heavyweights this week – from the likes of Apple (AAPL), Amazon (AMZN), Alphabet (GOOGL), Meta (META), Microsoft (MSFT) and Intel (INTC), to name just a few. The advance reading on second-quarter GDP comes out on Thursday, and the Federal Reserve will report a decision about interest rates following the FOMC meeting on Wednesday. For investors, though, it hardly feels like a decent market advance over the past month or so given the steady trend lower on most asset classes for most of this year. Nonetheless, the market seems to be attempting to find a bottom at this level.

Disclosure: Firm and/or family long AAPL, GOOGL, INTC, MSFT.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Be the first to comment