I last discussed the respective positions of Dynavax (NASDAQ:DVAX) and Novavax (NASDAQ:NVAX) in 03/2022’s “The Alphavaxers: Dynavax And Novavax – A Tale Of Two Cities” (the “Tale“). At the time, the Alphavaxers had each just reported Q4, 2021 earnings. Now each has two more quarters of earnings under their belts, having recently reported earnings for Q2, 2022.

In this article, I provide overviews on how these companies stack up now as the pandemic continues to wind down.

The Alphavaxers Results Have Diverged Sharply Compared To Prior Guidance During 2022.

Dynavax’s Q2, 2022 Earnings Report

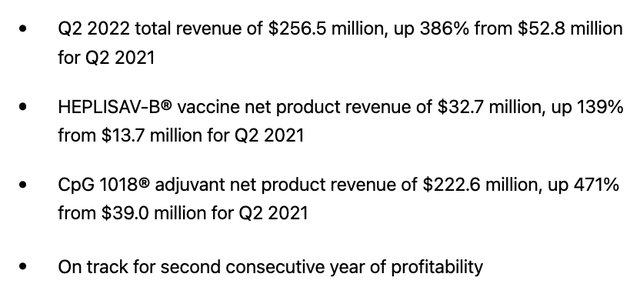

Dynavax reported its Q2, 2022 earnings after market close on 08/04/2022. Its leads pointed to a healthy situation as follows:

seekingalpha.com

HEPLISAV-B has been slow to develop, having been approved in 2017; however, as I will discuss, it has significant forward potential. Adding Q2’s $222.6 million in CpG 1018 net revenues to Q1’s $91.5 million puts it within 56% of meeting its ambitious Q4, 2021 guidance. I may strain to reach $550 million in net CpG 1018 revenues for 2022, however it is more than halfway there.

The big deal for Dynavax and its shareholders which contrasts so dramatically with Novavax is the profitability piece.

Novavax’s Q2, 2022 Earnings Report

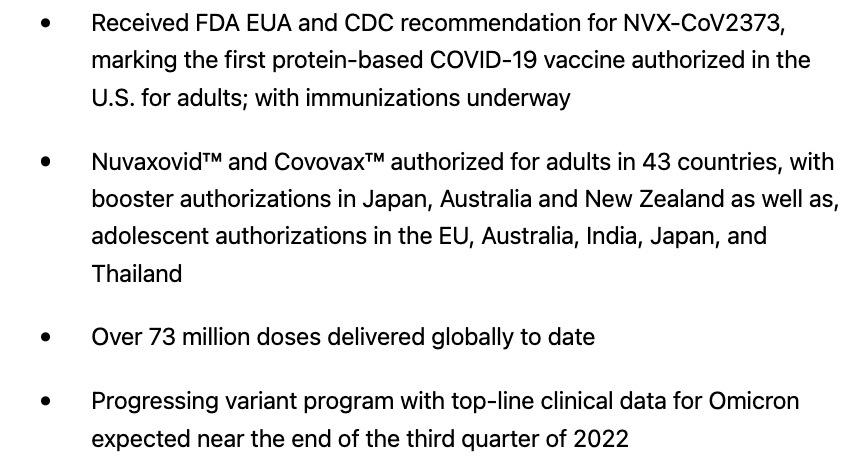

Novavax reported its Q2, 2022 earnings after market close on 08/08/2022. It was not nearly the nice, neat report that Dynavax had offered. None of its initial four leads mentioned its financial performance. Instead, they addressed an impressive run of regulatory decisions and performances as follows:

seekingalpha.com

This is always an issue with Novavax. It has never managed to achieve profitability in its >30 years of operation. Rather, it has run up an accumulated deficit of $3.6 billion. As one scrolls through the meat of Novavax’s Q2, 2022 earnings release, one finally learns:

Net loss for the second quarter of 2022 was $510 million compared to $352 million for the comparable period in 2021.

Both Issued Interesting Guidance.

Dynavax’s Revised Guidance For 2022

Dynavax issued a revised guidance for 2022 as follows:

Full-year CpG 1018 adjuvant net product revenues of between $550 million and $600 million, with an associated gross margin anticipated to be approximately 60%

Research and development expenses to be between approximately $50-$60 million

Selling, general and administrative expenses to be between approximately $130-$140 million

Interest expense of approximately $7 million.

It differs from its previous 2022 guidance given in its Q1, 2022 release in several respects. Its new range of $550-600 million for its CpG 1018 is an upgrade from its previous $550 million guidance, as is its expected margin increase from approximately 50% to approximately 60%.

In terms of guided expenses, its bottom range for selling, general and administrative showed an increase from $120 million. Its bottom range of research and development expenses dropped from $55 million to $50 million. So overall, the new guidance appears to enhance expectations around CpG 1018, while pointing to roughly equivalent aggregate expenses.

Novavax’s Revised Guidance For 2022

While Novavax’s business is busier and less compact than Dynavax’s, its revised guidance was far more succinct. It included the following concise but deadly revelation:

Revising full year 2022 total revenue guidance to $2 to $2.3 billion. Total revenue reflects all sources, including product sales of Nuvaxovid by Novavax, grants revenue, royalties and other revenue.

Dynavax would surely kill for a revenue guidance of $2 to $2.3 billion. For Novavax, it was a horrible embarrassment. The second lead bullet point in Novavax’s Q1, 2022 earnings release had trumpeted:

Reiterating full year 2022 total revenue guidance of between $4 and $5 billion

To be fair, Novavax had advised of a potential shortfall in its guidance during its Q1, 2022 earnings call. As disclosed below by CFO Kelly, it was trying to play both sides of the fence on its revenue guidance:

…Today, we are reiterating our full year 2022 total revenue guidance of between $4 billion and $5 billion. As a reminder, total revenue reflects all sources, including sales at Nuvaxovid by Novavax, grants revenue, royalties and other revenue.

…we’re prepared to deliver doses of our vaccine to Gavi under the terms of our supply agreement. However, we were recently notified by Gavi of their intent to seek to revise the number and timing of doses. To date, Novavax has not received an order from Gavi and the timing and quantities of future orders to deliver Novavax facility unclear.

Although we’re not adjusting our full year 2022 revenue guidance, we note that our current guidance assumes successful delivery and conversion up to $700 million prepayment to product revenue. In the event we deliver less, our resulting revenue expectations for the year could be affected. We look forward to sharing our progress towards realizing this total revenue guidance on future earnings calls.

To be even fairer, I will note that a guidance shortfall of ~$2 billion is hardly controlled by the fate of a $700 million item.

As The Pandemic Wanes, The Future For The Alphavaxers Will Likely Not Hinge Just On Their COVID Portfolio.

Dynavax Beyond COVID-19

Dynavax’s recent business results have greatly benefited overall from the pandemic. However, it has presented its challenges. Unfortunately, Dynavax offers no HEPLISAV-B guidance. Likely due to uncertainties as to impact on HEPLISAV of pandemic related COVID booster campaigns.

Its HEPLISAV franchise has significant potential revenue firepower. During its Q2, 2022 earnings call, Chief Commercial Officer Casale did emphasize the overall sanguine prospects for HEPLISAV as follows:

…The ACIP’s recommendation that all adults 19 to 59 years of age should receive Hepatitis B vaccination significantly expands the number of adults in the U.S. who should be vaccinated against Hepatitis B. Compared to the prior risk based recommendation, we continue to believe that the ACIP recommendation will be a significant catalyst for growth and estimate the Hepatitis B market opportunity could grow to approximately $800 million by 2027 with Heplisav-B well positioned to secure a majority market share over time.

In this regard, it is important to note that HEPLISAV’s recent gains are from increased market share. Dynavax has yet to see any increased sales from the revised ACIP recommendation, which will take time to work its way into clinical practices.

I am hopeful that with its superior two doses in a single month regimen, HEPLISAV should be able to lay claim to at least 50% of this $800 million market. Were it to do so, HEPLISAV would more than cover Dynavax’s entire expense profile with a nice excess.

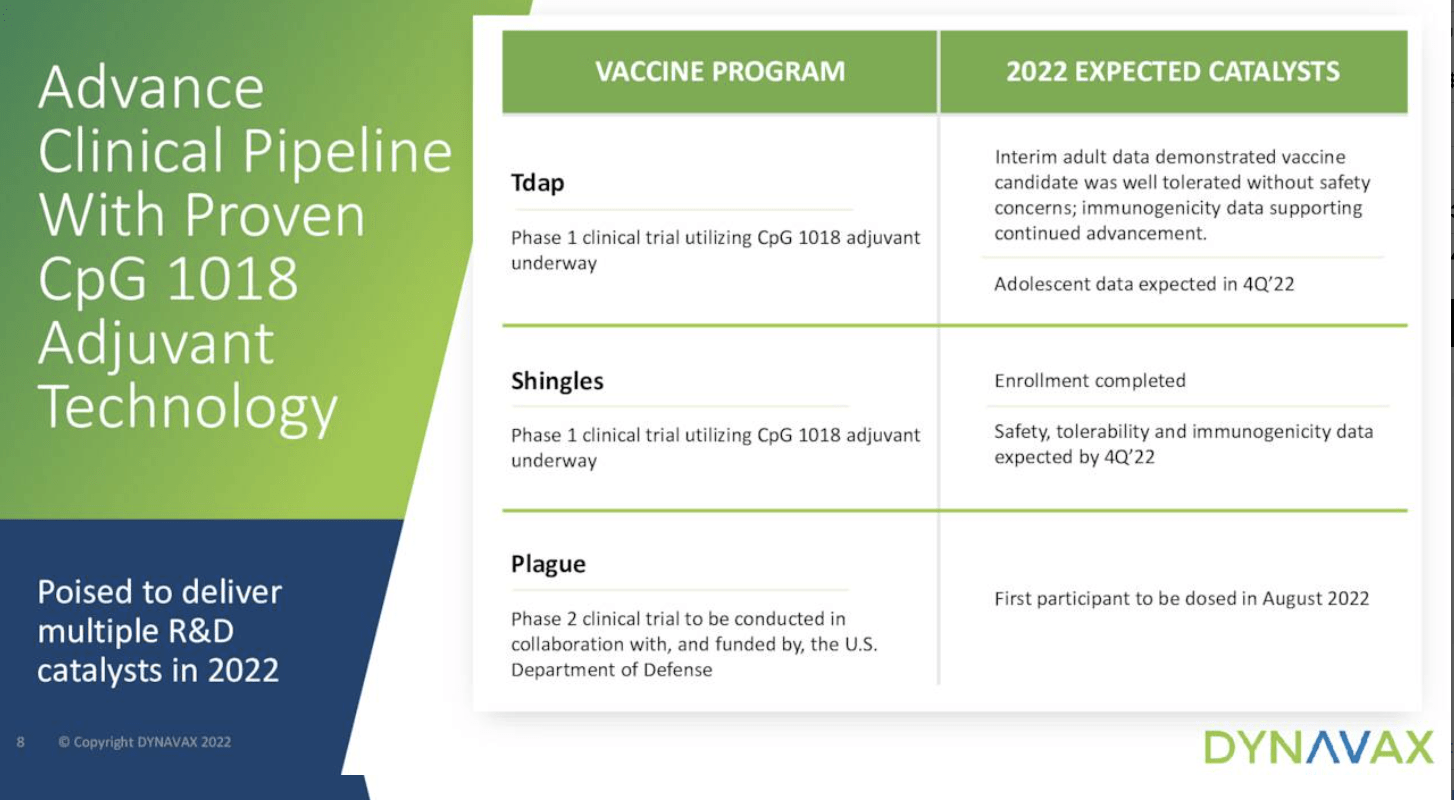

Even with all its potential, HEPLISAV is not the brightest jewel in Dynavax’s crown. Its adjuvant CpG 1018 is the real powerhouse. At the moment, it is shining because of the pandemic. However, it also contributes to HEPLISAV and has application throughout Dynavax’s pipeline as reflected by its Q2, 2022 earnings slide below:

seeking alpha.com

Novavax Beyond COVID-19

At the moment, Novavax’s product revenues are all tied to COVID per its Q1, 2022 10-Q p. 7. Back in the day, before COVID, Novavax’s fortunes rose and fell, on its two major programs, its RSV therapies and its NanoFlu inoculation for seasonal influenza.

Although from time to time these programs stood on the cusp of breaking through, to this point neither has panned out. Interestingly, Novavax makes no mention of RSV during either its Q1 or its Q2, 2022 earnings calls.

As for its NanoFlu program, this has gone from being poised for a 2021 BLA filing to seemingly being subsumed in its new combination vaccine. Novavax reports as follows on its current influenza plans in its Q2, 2022 earnings release:

COVID-19-Influenza Combination (CIC) Vaccine Candidate Clinical Development

Announced initial results of CIC Phase 1/2 trial demonstrating robust immune response with both stand-alone influenza and CIC vaccine candidates

Phase 3 trial to evaluate efficacy on-track to be initiated in 2023

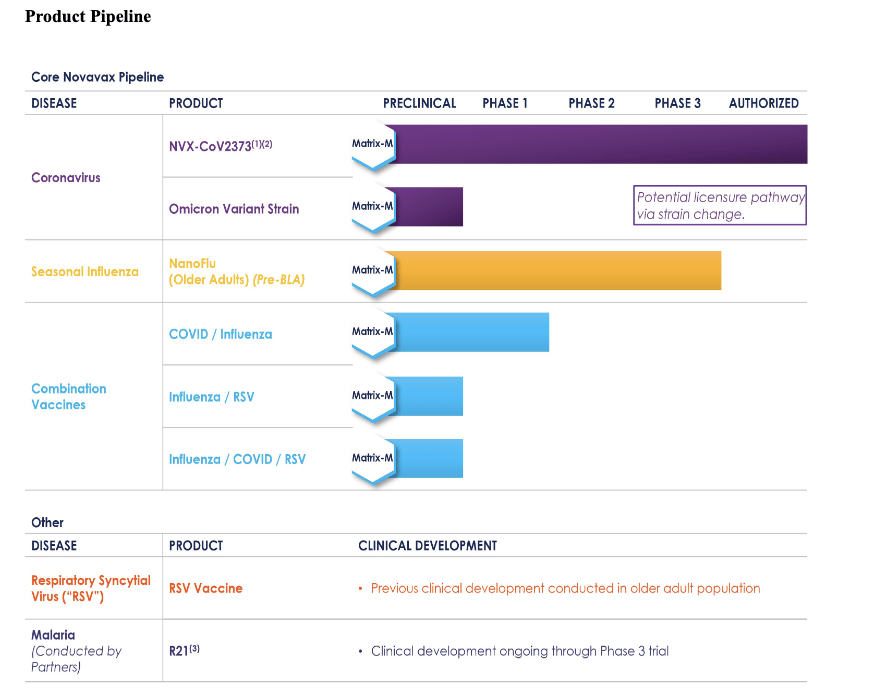

As for NanoFlu its position as a standalone product is unclear. Novavax includes the following pipeline graphic in its latest 10-K, pg. 8:

seekingalpha.com

This slide implies that a NanoFlu BLA is in process. Contrast this with its Q2, 2022 earnings slide below, which makes no mention of any such BLA:

seekingalpha.com

With clinical stage biotechs, uncertainty is always part of the game. Novavax takes such uncertainty to new heights.

Conclusion

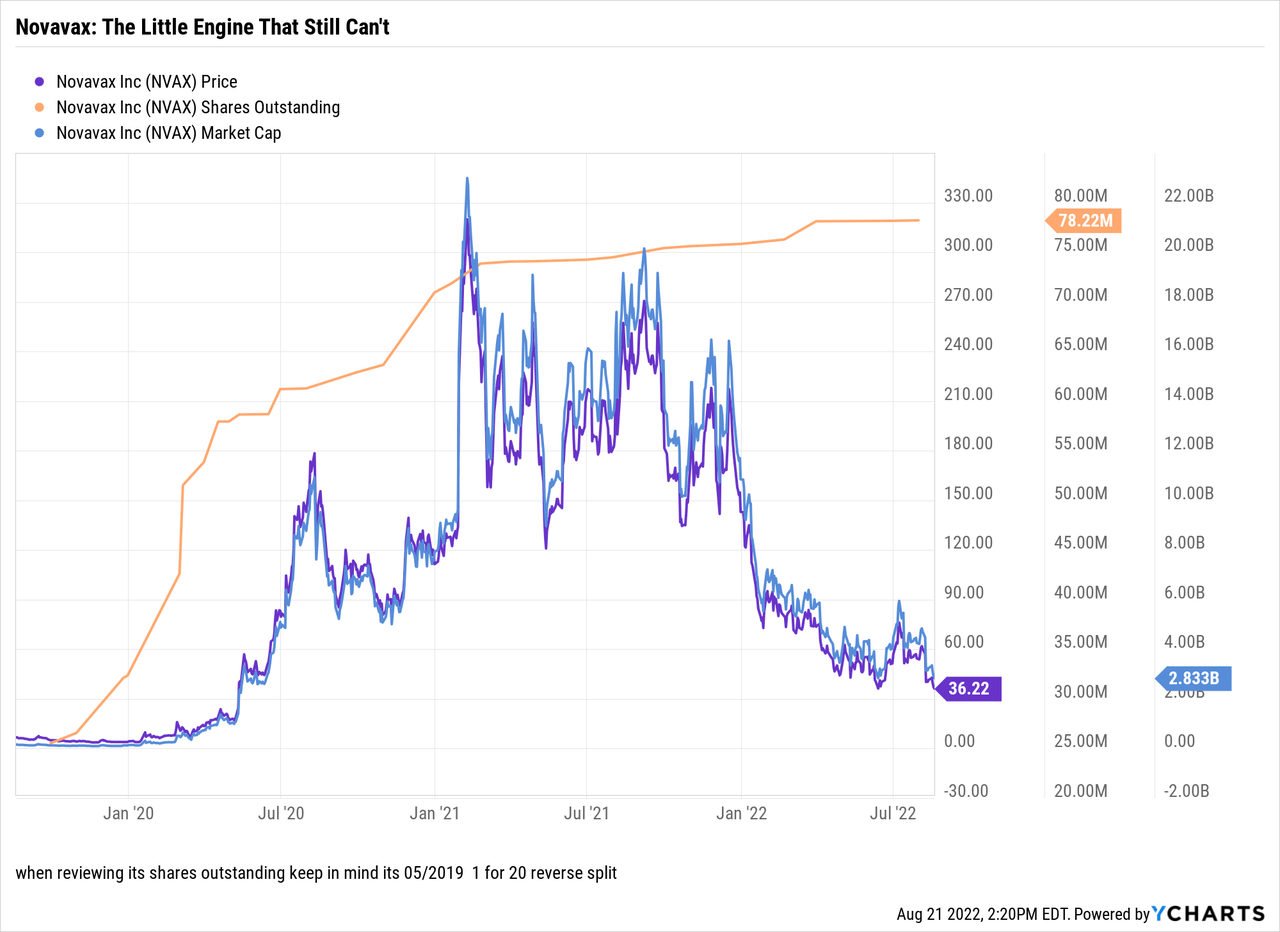

Novavax is bad news for investors. Its recent downbeat price as shown by its price chart below has prompted some to regain interest in the name:

Beware any such siren call. I submit that Novavax is another case where Seeking Alpha’s quant ratings have pegged things just about right. In 2016’s “Novavax: The Little Engine That Couldn’t”, I warned that Novavax’s facility in procuring diverse grants makes shareholders irrelevant.

Dynavax price action hardly shows any improvement compared to Novavax. Nonetheless, its fundaments trump Novavax’s by a mile. It has no obvious near-term catalysts, so there are no reasons to load up on it at the moment. Those, who, like myself, like its longer-term prospects, will do well to gradually accumulate it on weakness.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment