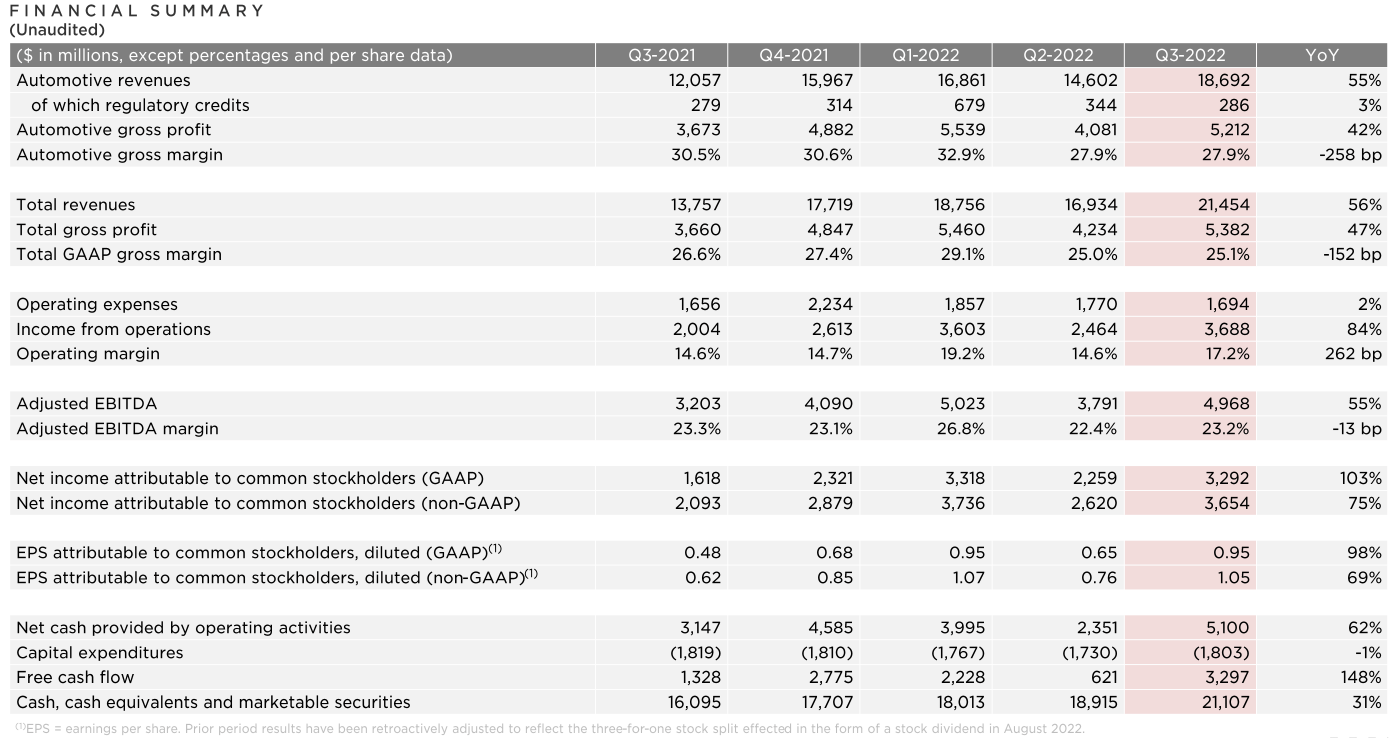

After the release of a somewhat mixed Q3 earnings report, Tesla’s (NASDAQ:TSLA) shares closed at $208.16 (down ~6.25%) in the after-hours session. In Q3, Tesla’s non-GAAP EPS of $1.05 came in slightly ahead of street estimates; however, Tesla missed on the top-line with revenue coming in at $21.45B (est. $21.98B, ~2% (or $500M) miss) and auto gross margin of 27.8% (est. 28.5%) also fell short of expectations. Further, Tesla reported an operating margin of 17.2% for Q3 on the back of strong operating leverage, which was somewhat offset by FX and Gigafactory Texas and Gigafactory Berlin ramp-ups.

Tesla Q3 2022 ER Deck

Tesla Q3 2022 ER Deck

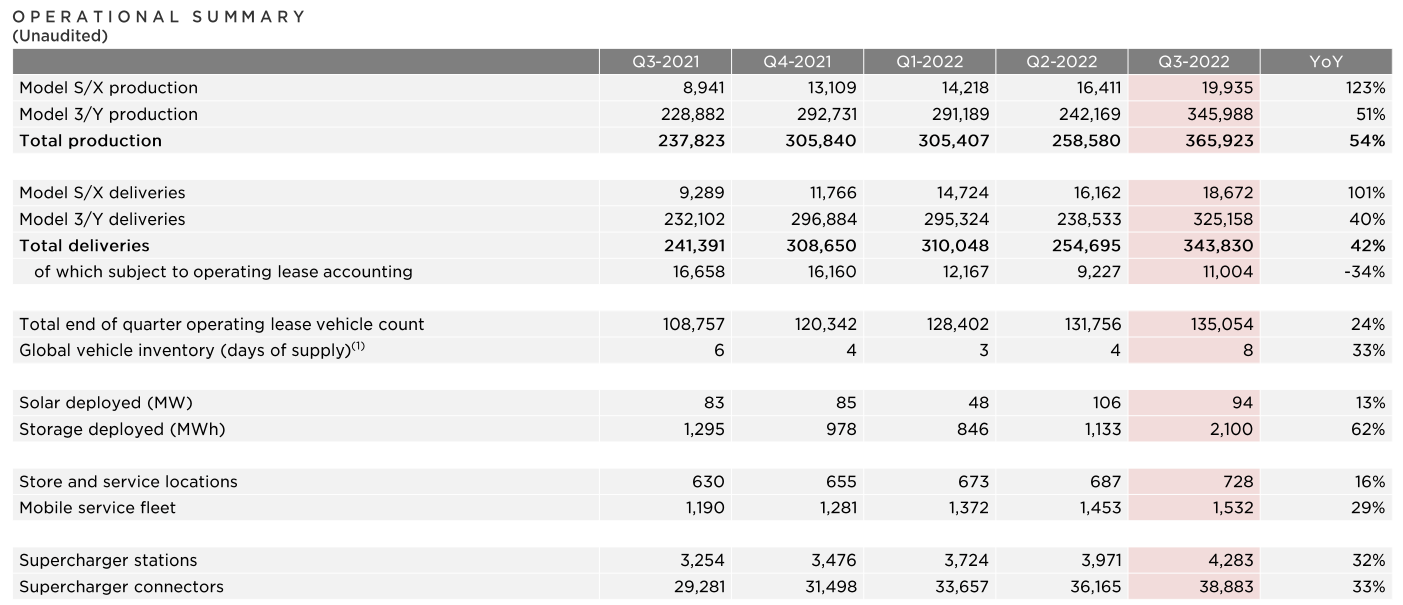

While the broader media is probably going to make a lot of Tesla’s minor sales miss, there’s nothing to be surprised about here. The deliveries data released on 2nd October had already telegraphed a revenue miss for this quarter, and we discussed this a few days back: Tesla Tumbles As Musk Fumbles, But There’s A Silver Lining. According to Tesla’s management, the company is hitting limits on outbound logistics for shipping from Shanghai to Europe/US and local trucking in these markets due to batch production concentrated towards the end of quarters. Tesla is trying to solve this issue by smoothing out the production across the quarter, but this will take time, and so, production will continue to come in higher than deliveries in Q4. Now, this explanation from Tesla makes sense, but investor doubts about demand in China are equally reasonable. And this differential is something I’ll be monitoring closely in upcoming quarters.

Now, Tesla’s Q3 ER was a mixed bag. However, if we factor in macroeconomic and supply chain issues, Tesla’s 56% y/y revenue growth is an astounding achievement. Tesla just reported a record-breaking quarter. More importantly, Tesla’s management reiterated its multi-year volume growth target of 50% CAGR. We know that Tesla Semi deliveries are starting in December, and Musk told us during the Q3 earnings call that Tesla Cybertruck is in the final lap (close to industrialization, deliveries in 2023). In my view, Tesla’s EV product roadmap is the strongest its ever been, and additional business lines like autonomous vehicles (robotaxis), Optimus (humanoid bot), Dojo AI chips, and energy storage have immense potential.

Tesla Q3 2022 ER Deck

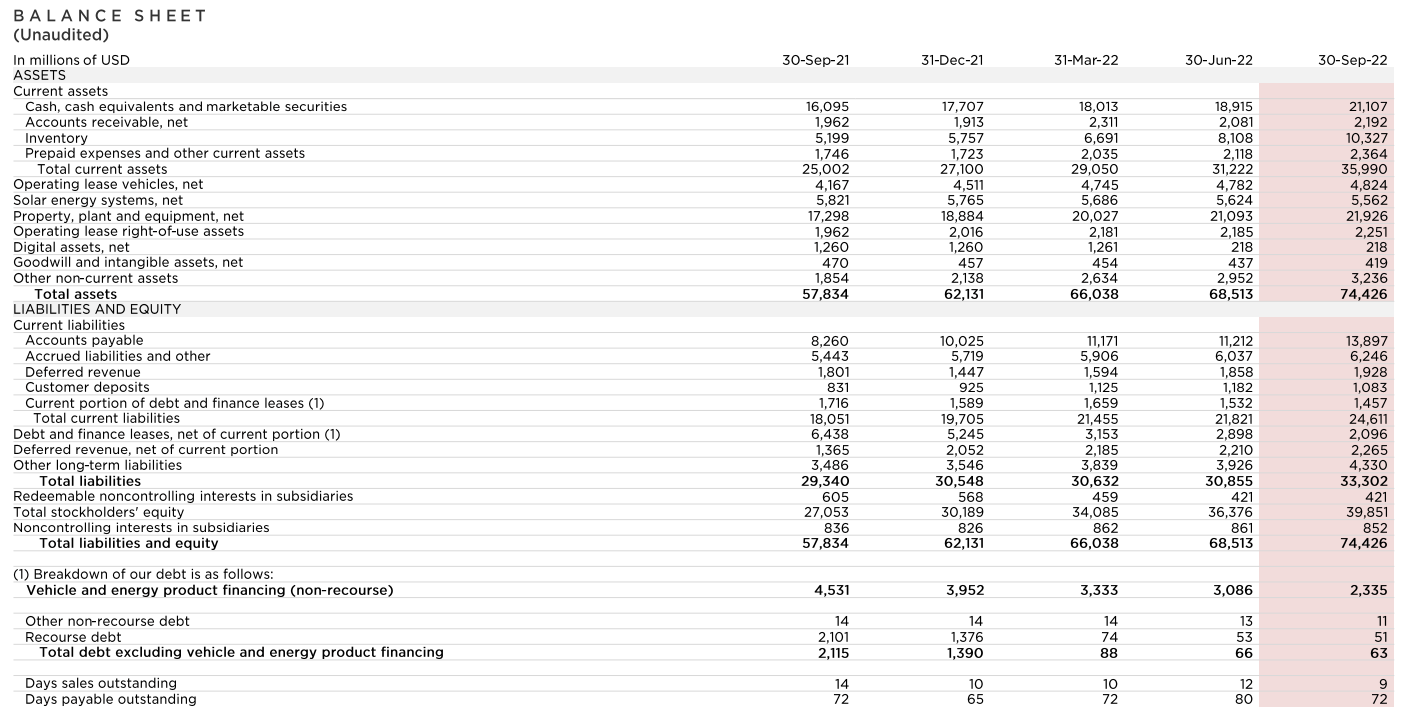

With a cash position of $21B and no debt, Tesla’s financial position is rock solid. Tesla is now producing tons of free cash flow ($9B over the last twelve months, $3.3B in Q3), and once the Gigafactory Austin and Gigafactory Berlin ramps are done, the cash generation could be even greater. Some of Tesla’s investors have been clamoring for a buyback, and Musk said during the ER call that a $5-$10B buyback could be on the way in 2023, and even if we go through a recession, Tesla could generate meaningful cash next year.

Tesla Q3 2022 ER Deck

While a $99M drop in customer deposits could be an early sign of demand destruction for Tesla, Musk and Co. just guided for an “epic” Q4 and brushed off any demand concerns. As an individual investor and financial analyst, I have attended several Tesla earning calls and investor events in the last few years; and I can say with confidence that Elon Musk has never been more bullish on the company’s future.

Now, Elon may be about to sell billions of dollars worth of shares (to raise funds for the Twitter (TWTR) deal) in the next few days, and a higher Tesla stock is favorable for him. Hence, Mr. Market’s skepticism about Musk’s hopium is more than justified, and investors must be cautious with such claims. After all, Musk just proclaimed that –

I see a potential path for Tesla to be worth more than Apple and Saudi Aramco combined.

Well, Musk basically said that Tesla could be worth more than $4.5T, which seems delusional. Now, I interpret this statement as one of Musk’s many long-term epiphanies, and since there was no timeline mentioned, this prediction could be 5, 10, or 20 years away from materializing (if it materializes at all). Looking at Musk’s history with such bold claims, I wouldn’t bet on him, and I wouldn’t bet against him. As an investor, I am just happy that Tesla’s CEO has a strong conviction in its future. While Musk’s hopium is no reason to buy Tesla, I think its valuation has moderated enough to warrant fresh capital.

Updated Valuation For Tesla

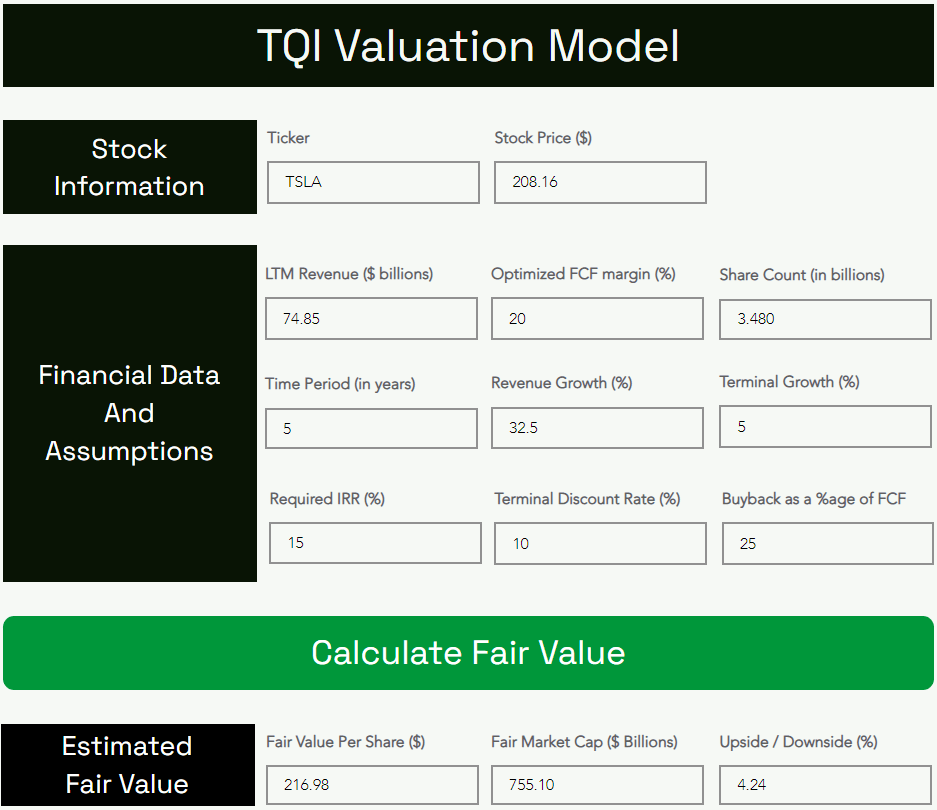

Recently, I shared my valuation model and rationale for the underlying assumptions. However, in light of quarterly earnings, I would like to share an updated valuation model with LTM revenue and Share Count changed to factor in the Q3 report, along with minor modifications to certain assumptions. Please let me know if you have questions or concerns via the comments section.

Here’s what Tesla’s fair value is looking like after its Q3 report:

TQI Valuation Model (TQIG.org)

According to my analysis, Tesla’s intrinsic value is ~$217 per share (upgraded from $214 per share). This means Tesla is now undervalued by ~4%.

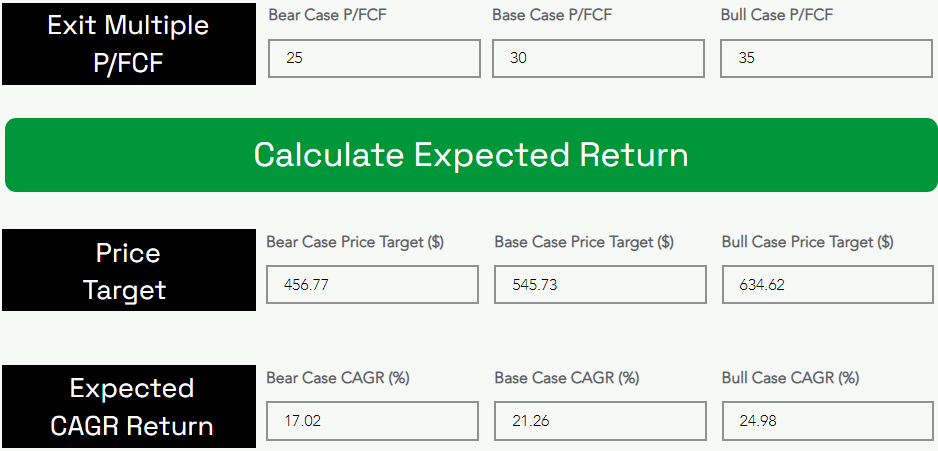

Now let’s look at expected CAGR returns for the next five years. Assuming a base case exit P/FCF multiple of 30x for Tesla, I see the stock hitting $545.73 per share by 2027.

TQI Valuation Model (TQIG.org)

As can be seen above, Tesla is projected to deliver CAGR returns of 21.26%, which beats my minimum IRR of 20% for high-growth stocks. Hence, I rate Tesla a ‘buy’ at $208 per share. However, there’s a catch!

A Precarious Technical Setup

Before we discuss Tesla’s technical chart, I wanted to share an excerpt from my work on Tesla (published to my marketplace service on 6th October 2022):

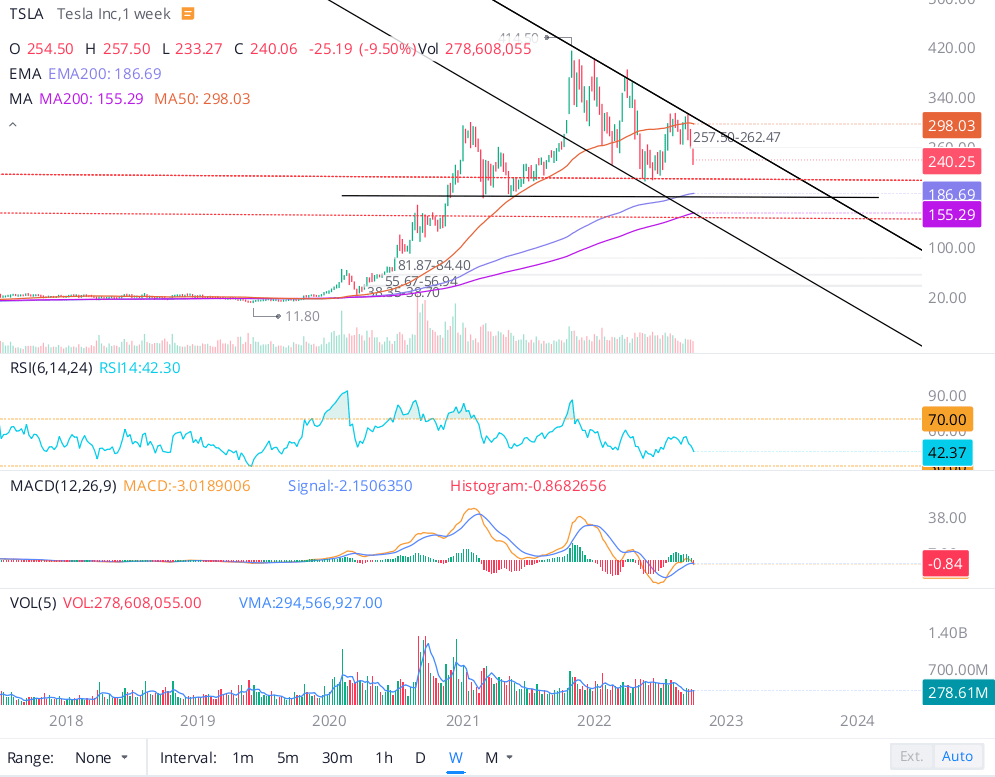

As of writing, Tesla is trading at ~$240 and trying to form a base at this level after a rapid decline; however, the stock remains stuck in a falling wedge pattern. From a technical perspective, Tesla is looking nailed on to retest its 2022 lows of ~$209 (a level last seen in May), which is very close to my fair value estimate for the company.

WeBull Desktop

If Tesla fails to hold onto the psychological support level of $200, we could see a swift ride down to the $175 to $150 range. In the past, I have discussed the idea of a reverse gamma squeeze in Tesla, and such a move could come to fruition in the event of a deep economic recession hurting consumer demand for Tesla’s products amid rising competition in the EV market (yes, competition is coming in the form of traditional automakers and other EV startups).

On the flip side, if Tesla can break out of the falling wedge pattern, we could see a run up to new all-time highs ($400+) in 2023. While it is hard to see such a move in the foreseeable future due to the rising probability of a recession, the market is unpredictable, and Tesla is one of the strongest earnings growth stories in the market.

If I were to make a directional bet, it would be to the downside”

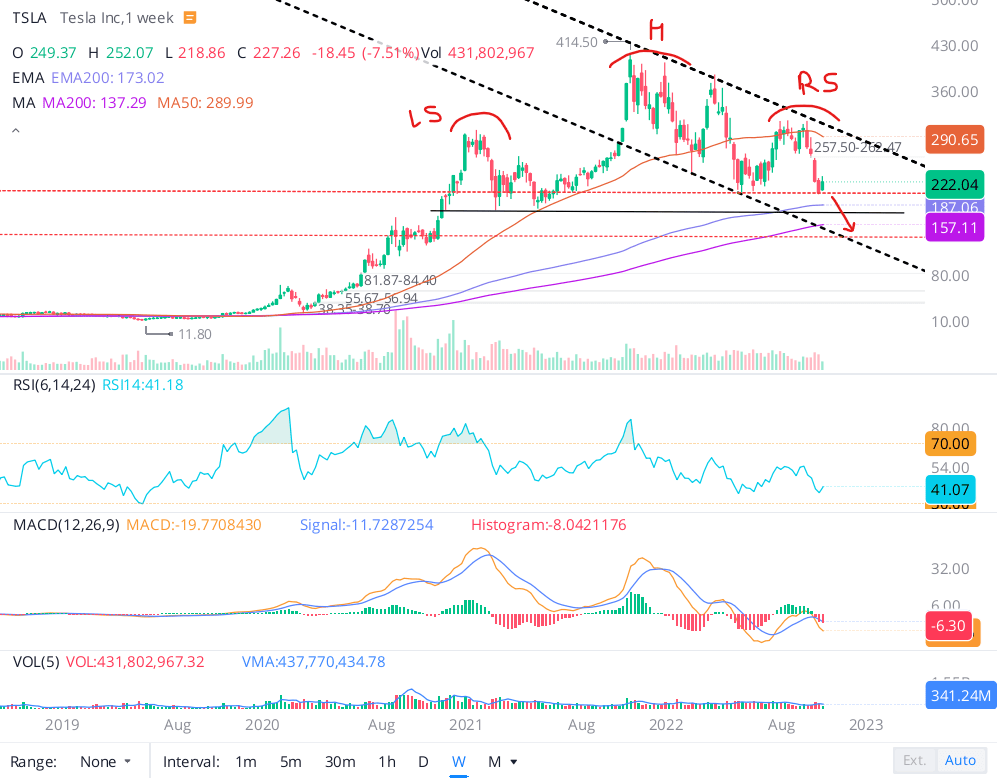

While it’s only been a couple of weeks since this research work was published, Tesla has already tested the $209 level twice and is currently trading below this level. With Elon Musk likely to sell more shares on Friday or early next week (to raise remaining funds for his $44B Twitter buyout), I could see a big test of the $200 psychological support in the coming days.

Tesla’s chart (WeBull Desktop)

On Tesla’s chart, we are now looking at the potential breakdown of a bearish “Head and Shoulders” pattern, which could mean a quick ride down to the mid-100s (even low-100s is possible). The prospect of a reverse gamma squeeze in Tesla is real, and despite my switch to a bullish stance for Tesla’s stock after considerable valuation moderation, I urge investors to proceed with caution. For anyone looking to buy Tesla for the long term, I see slow accumulation as the right strategy. However, if you are looking for a short-term buy, just skip Tesla for good.

Final Thoughts

After undergoing months of painful correction, Tesla’s stock is finally undervalued; however, given current market conditions, it may very well overshoot to the downside. A bearish post-ER price move indicates that Elon’s positive commentary around [50% CAGR] revenue (volume) growth, [$5-$10B] stock buyback, [best-ever] product roadmap, and Tesla’s future valuation [$4.5T = Apple + Saudi Aramco] has failed to paper over the evident cracks (albeit small misses) in Tesla’s Q3 report. That said, Tesla just reported yet another record-breaking quarter and is set to create new records in Q4. As a long-term investor, I view Tesla’s Q3 miss as nothing but short-term noise.

From a long-term perspective, Tesla is one of the strongest earnings growth stories in the market. And now that Tesla is undervalued, investors shouldn’t pass up on this fantastic company. Considering the rising probability of an economic recession and Tesla’s precarious technical chart (showing a ‘Head & Shoulders’ pattern), I think slow accumulation is the way to go here. As I have said in the past, the low-200s seem like a reasonable entry point in Tesla for long-term investors. If we do see Tesla break down to the mid-100s, I think that would be a great buying opportunity.

Key Takeaway: I rate Tesla a buy at $208 per share, with a preference for slow accumulation using 6-12 month DCA plans.

As always, thank you for reading, and happy investing. Please feel free to share any questions, concerns, or thoughts in the comments section below.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment