Spencer Platt/Getty Images News

Price Action Thesis

We follow up with a detailed price action analysis on Tesla, Inc. (NASDAQ:TSLA) stock as there have been significant developments over the past month.

We re-rated TSLA to Buy in May after cautioning investors to be wary about the unknowns in Q2 after its robust Q1 results in April. Our postulation about the headwinds that impacted TSLA in Q2 has played out, as investors were overly optimistic in April.

However, the market astutely drew in buyers to set up a double top bull trap in early April before forcing a rapid liquidation in May, resulting in a validated bear trap. As a result, we revised our rating earlier than usual, expecting a bear trap to ensue.

However, TSLA has remained in negative flow (decisive bearish momentum) as it struggled to regain its bullish bias. Therefore, we revisited our price action thesis and valuation models to parse the recent developments.

Despite the near-term bear trap, we believe that the momentum in TSLA stock has shifted dramatically to the downside. Therefore, TSLA could continue to underperform the market as it parses its rich valuation.

Accordingly, we believe it’s appropriate to revise our rating from Buy to Hold as we await a re-test of its revised near-term support ($540).

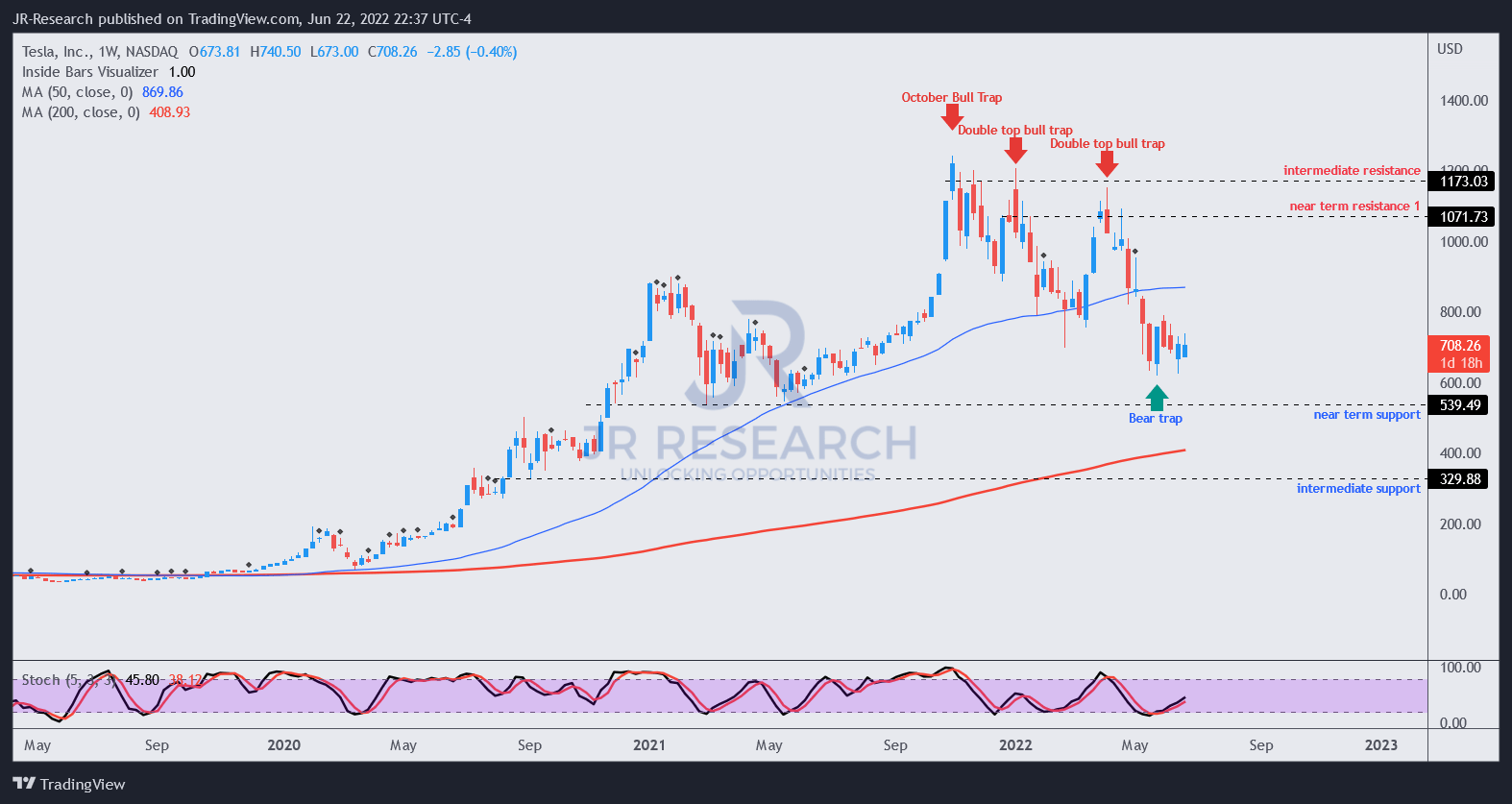

TSLA – The Double Tops Took Its Toll

TSLA price chart (monthly) (TradingView)

We believe the market has moved to digest TSLA stock’s massive rise from the COVID bottom since October 2021 (its first significant bull trap). Moreover, it formed its first double top bull trap in January 2022 (as seen above), which cautioned that the party could be over soon.

TSLA price chart (weekly) (TradingView)

Poring into its weekly chart, we can glean its first double top in January, which sent TSLA into a rapid liquidation that formed a validated bear trap in late February. But, a second double top in early April (drawing in buyers rapidly before the release of its Q1 earnings) with a lower high formed after its February bear trap (thus resolved).

Two double tops in quick succession would typically have caused significant concerns because such price action structures are often potent early warning signals of trend reversals.

But, we postulated in May that the rapid sell-off could form a bear trap (which it did, as seen above) as TSLA consolidated at the current levels. However, we noted that TSLA has failed to regain positive flow (decisive bullish bias), despite its near-term bear trap, moving into bearish momentum.

Consequently, the change in flow is significant, which is consistent with the impact from its twin double tops. The market seems keen to continue forcing further sell-offs after it draws in the current round of dip buyers.

Therefore, we have lowered its near-term support to $540 as we await its potential re-test.

TSLA’s Expensive Valuation Is Coming Home To Roost

TSLA valuation metrics (TIKR)

Given its normalized P/E of 55.37x, we think the argument that it’s cheap is getting harder to defend. We have consistently recognized that TSLA stock has traded at a premium. Notably, the market has supported that premium previously, as TSLA grew its topline and profitability significantly. Therefore, the 50x P/E mark has helped to form previous bottoms in its price action.

But, investors must recognize that the market has reversed its flow convincingly on TSLA stock (from bullish to bearish). Therefore, past arguments defending its 50x P/E “bottom” may be increasingly tenuous. Instead, we think the market has shifted its focus on TSLA stock’s rapid ascent over the past two years, which has made its valuation too rich to justify.

| Stock | TSLA |

| Current market cap | $733.76B |

| Hurdle rate (CAGR) | 20% |

| Projection through | CQ2’26 |

| Required FCF yield in CQ2’26 | 2.5% |

| Assumed TTM FCF margin in CQ2’26 | 13% |

| Implied TTM revenue by CQ2’26 | $292.6B |

TSLA reverse cash flow valuation model. Data source: S&P Cap IQ, author

TSLA stock delivered a 5Y CAGR of 56.72%, easily outperforming the Invesco QQQ ETF’s (QQQ) 15.17% 5Y CAGR. Therefore, to expect it to meet its previous outperformance moving forward would have required a gargantuan effort that, in our opinion, is “impossible.”

As a result, we revised our hurdle rate to a more reasonable 20% (which is still above the market’s 5Y average). However, with a lower hurdle rate, it only makes sense that the market would require a higher free cash flow (FCF) yield to hold TSLA. Hence, we assumed an FCF yield of 2.5%, consistent with our assumptions of “high-growth plays.” We have been “lenient” because we usually use at least a 25% hurdle to justify a 2.5% yield. Therefore, we have cut CEO Elon Musk & team some slack.

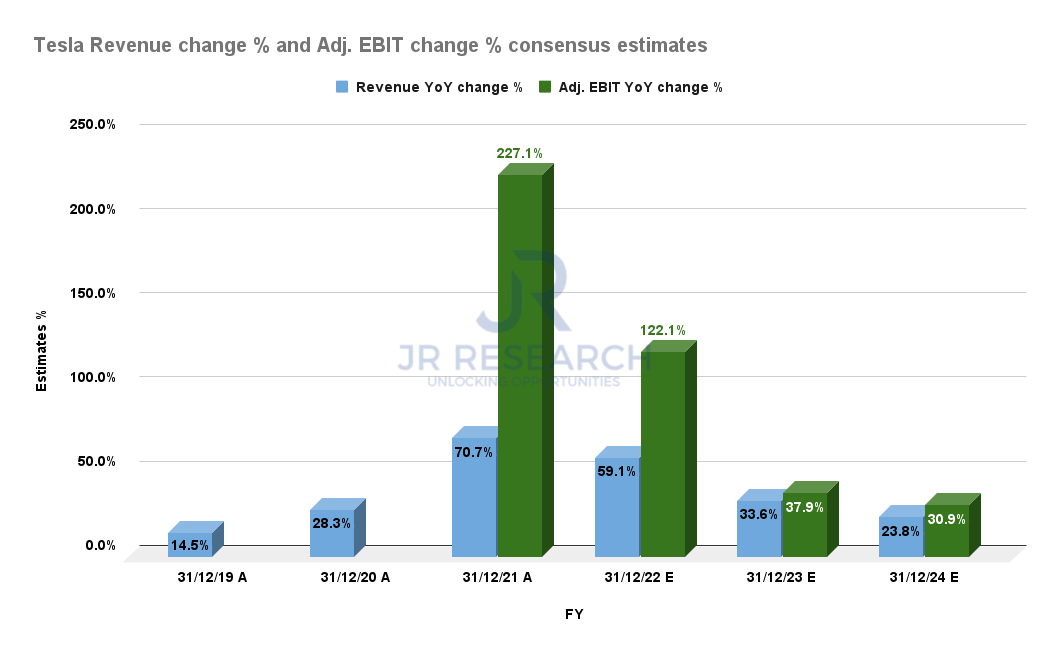

Tesla revenue change % and adjusted EBIT change % consensus estimates (S&P Cap IQ)

Using a blended TTM FCF margin of 13%, we arrived at a TTM revenue target of $292.6B by CQ2’26. However, the consensus estimates suggest that TSLA could deliver revenue of $141.6B in FY24. Notably, as seen above, Tesla’s revenue and adjusted EBIT growth is estimated to slow dramatically through FY24. Therefore, investors need to be prepared that the potential for outperformance could be diminishing fast.

Given the Street’s consensus (generally bullish), Tesla would need to post a TTM revenue CAGR of 43.97% through CQ2’26. Therefore, investors need Tesla to deliver a cadence markedly above the consensus estimates. In our opinion, that’s highly unlikely.

Is TSLA Stock A Buy, Sell, Or Hold?

Tesla CEO Elon Musk probably recognized the need to prove that Tesla can continue scaling rapidly to justify its valuation and his enormous wealth tied to its stock. As a result, he has been emphasizing “massive scale” and also working to retool Giga Shanghai to ramp production, compensating for its Q2 weakness.

But, we believe that the market has moved decisively against TSLA stock, and therefore, Tesla investors should recognize the market’s forward intentions.

As such, we revise our rating on TSLA stock from Buy to Hold. We urge investors to be patient and wait for a much steeper fall in its valuation before adding exposure.

Be the first to comment