jetcityimage

Elevator Pitch

I rate Tesla, Inc.’s (NASDAQ:TSLA) stock as a Hold.

I wrote about Tesla’s lower-than-expected Q2 2022 deliveries in an earlier article published on July 6, 2022. With this latest update, I focus on TSLA’s recently completed stock split and the changes in Tesla’s consensus price target.

I continue to have a Hold rating assigned to Tesla, as I don’t think TSLA’s shares are heading significantly higher after target price changes and the stock split. An initial analysis suggests that the stock split has yet to boost Tesla’s trading liquidity; while the implied upside for TSLA’s shares as per the consensus price target isn’t very attractive.

TSLA Stock Key Metrics

Tesla completed the company’s 3:1 stock split on August 25, 2022. Earlier on August 5, 2022, TSLA disclosed that the split was approved by the Board with the purpose of making “stock ownership more accessible to employees and investors.”

There are certain key metrics that offer an early, albeit imprecise, indication of whether Tesla’s stock split has been an initial success.

One key metric is the change in trading liquidity for TSLA’s shares following the stock split.

Based on trading data taken from S&P Capital IQ and my own calculations, Tesla’s average daily trading volume (adjusted for split) has decreased by -19% from 63.3 million for the seven trading days prior to the stock split to 51.4 million for the seven trading days after the completion of the split. In other words, TSLA’s trading liquidity didn’t improve after the stock split.

That said, the time frame for comparison is a bit too short to arrive at the conclusion that the stock split wasn’t able to boost Tesla’s trading volumes. The recent Labor Day holiday in the U.S. could have also impacted trading volume as pre-holiday trading tends to be lighter for the overall market.

Another key metric is the company’s post-split share price performance.

According to data obtained from Seeking Alpha, Tesla’s shares have underperformed the broader market in the one week post-split. Between August 24, 2022 and September 2, 2022, TSLA’s stock price dropped by -9.1%, while the S&P 500 pulled back by a milder -5.2% during this period.

Similar to the trading volume changes, it isn’t possible to conclude that the impact of the stock split on Tesla wasn’t positive. The time period of observation isn’t sufficiently long, and Tesla’s share price could be affected by multiple factors unrelated to the split in such a short period of time.

As a comparison, other heavyweight stocks, Amazon (AMZN) and Alphabet (GOOG) (GOOGL) did their stock splits in June 2022 and July 2022, respectively, and both have seen their respective share prices trade higher after the stock splits. As such, it will be meaningful to check back on Tesla’s trading volumes and share price performance in a few months’ time to better evaluate the stock split impact for the company.

In the subsequent two sections of the article, I highlight TSLA’s current consensus price target and the changes in its consensus target price in the past one year.

What Is Tesla Stock’s Target Price Now?

Wall Street’s consensus mean target price for Tesla is $306.17 now as per S&P Capital IQ data. This implies that the sell-side analysts think that TSLA’s shares can potentially rise by +13% as compared to its last traded stock price of $270.21 as of September 2, 2022.

An upside potential of +13% as implied by the current sell-side’s consensus price target doesn’t appear to justify a Buy rating for Tesla. Investors will typically demand a required rate of return of at least +15% to be interested in acquiring any company’s shares for capital appreciation.

The relatively low target price for TSLA is also reflected in the mixed view that Wall Street analysts have with regards to Tesla as evidenced by their respective investment ratings. Only 21 out of 37 (or 57%) of the sell-side analysts covering Tesla’s shares have either a Strong Buy or Buy ratings for the listed company.

I also look at the changes in Tesla’s target price over the past one year in the next section.

What Is 12 Month Price Target Changes For Tesla?

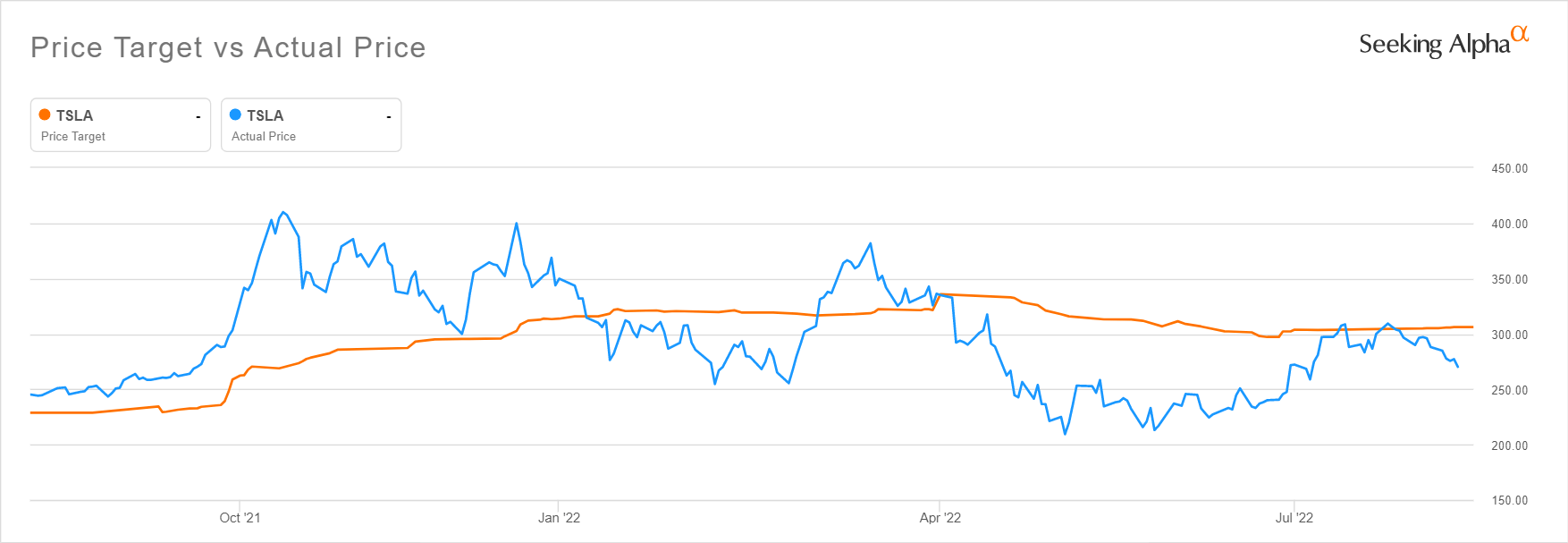

In the last 12 months, the sell-side’s consensus average target price for Tesla increased from below $250 to slightly above $300 as per the chart presented below.

The Changes In TSLA’s Consensus Sell-Side Price Target In The Past 12 Months

Seeking Alpha

The changes in the consensus price target for TSLA are a reflection of how the market’s expectations for the stock have evolved over time. As such, it is worthy to note that the downward revisions in Tesla’s target price started in late-April 2022, which coincided with two key headwinds that the company has been facing in recent months.

Firstly, the worst of China’s COVID-19 lockdowns happened in the second quarter of 2022. In my prior early-July update for Tesla, I highlighted that “I am concerned about the degree of TSLA’s reliance on China with respect to both production and sales.” As China continues to persist with its zero-COVID stance, this represents a key downside risk factor for Tesla.

Secondly, the Fed had announced a series of rate hikes in March, May, June and July 2022. The rising rate environment has been negative for growth stocks including Tesla, and this is validated by the stock’s valuation de-rating over time. According to S&P Capital IQ’s historical valuation data, TSLA’s consensus forward next twelve months’ Enterprise Value-to-Revenue multiple has compressed from a six-month peak of 14.26 times recorded on April 4, 2022 to 7.89 times as of September 2, 2022. As it stands now, it doesn’t appear that investors are willing to pay a huge valuation premium for growth names such as Tesla, unless there is a clear indication that the Fed’s rate hikes are coming to an end.

Is Tesla Worth Investing In For The Long-Term?

It isn’t very clear that Tesla is a worthy long-term investment choice.

On one hand, Tesla has a clear edge over its rivals in terms of sourcing. Batteries are the key constraining factor relating to future production and market share gains. Based on a July 13, 2022 research report (not publicly available) published by Piper Sandler titled “Tesla’s Competition: A Framework for Ranking 20th-Century Auto Brands”, TSLA is the only automotive company to have 100% of “(battery) cell demand (2030) met by in-house or JV cells.” No other competitor comes very close to Tesla based on Piper Sandler’s analysis, with Volvo (OTCPK:VOLAF) (OTCPK:VOLVF) being a distant second (in a ranking of 14 automotive OEMs including TSLA) boasting a 71% 2030 battery cell demand coverage.

On the other hand, it is uncertain if Tesla will remain the most popular or appealing EV brand going forward. As TSLA grows in size, it might also have lost some of its appeal as a niche brand as compared to its early days. Morgan Stanley (MS) does a survey with its summer interns every year to see which automotive brand they prefer. According to the most recent survey performed this year as per an August 11, 2022 MS report (not publicly available) titled “4th Annual Intern Survey: Tesla Still Tops, But Less Cool Now”, TSLA’s “desirability as a share of total intern preference declined to 19% (in 2022) vs. 30% or over in each of the past three years.” This might be an early warning sign for how the Tesla brand perception might have changed in recent times.

Is TSLA Stock A Buy, Sell, or Hold?

TSLA stock is a Hold. Tesla’s valuations might have already de-rated significantly based on the forward Enterprise Value-to-Revenue metric, but China could pose further downside risks to TSLA’s outlook in the near term. In the longer run, I am positive on Tesla’s competitive edge in terms of sourcing, but I am less certain that TSLA’s branding power will remain intact going forward.

Be the first to comment