Sean Gallup/Getty Images News

It’s been more than five years since my last article on Tesla (NASDAQ:TSLA) in which I urged investors to avoid missing out on the big picture by “micro-analyzing” certain data points like the delayed Model 3 ramp-up and resulting, financial implications at that time.

Suffice to say, the Model 3 quickly advanced to the top-selling electric vehicle globally with its larger sibling Model Y enjoying even greater success as the crossover is expected to have made the Top 5 of global car sales last year.

Since the time the article was published Tesla has generated billions of dollars in free cash flow and raised additional funds from underwritten offerings and opportunistically selling new shares into the open market.

At the end of Q3, cash, cash equivalents and short-term marketable securities amounted to $21.1 billion while debt and finance leases were just $3.6 billion.

Even after last year’s fall from grace, the stock is still up by more than 400% over the past five years.

That said, things have clearly changed for Tesla in recent months as the company is dealing with a plethora of issues:

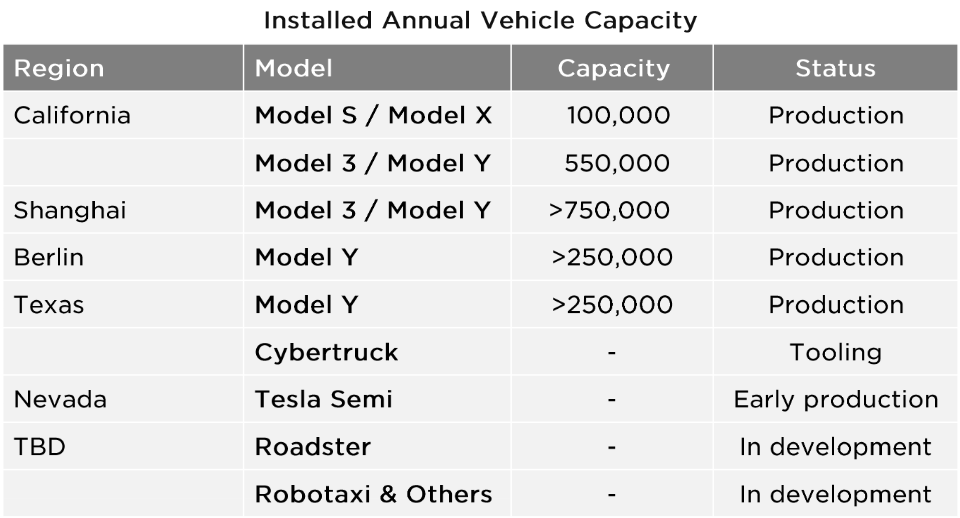

1. Increased Supply

Following a COVID-related shutdown in China last year, the company boosted output of its Shanghai Gigafactory to new records while at the same time ramping up its plants in Texas and Germany. Total installed annual vehicle capacity is approaching two million units:

InsideEVs.com

2. Lower Demand

After working through its backlog in Q3 and Q4, the company appears to be dealing with demand headwinds caused by looming subsidy regime changes and recessionary trends in key western markets and general weakness in China.

To provide some anecdotal evidence: When I ordered my Model Y Long Range in April, delivery was expected in May but ended up being delayed several times until the car finally arrived late in Q3.

To be fair, this was still much faster than most of the credible alternatives offered in Germany. Particularly Volkswagen-owned brands Audi, Porsche, Skoda and VW noted lead times of up to 15 months but BMW and Mercedes weren’t much better either.

In recent months, lead times have shortened substantially around the world with a Model Y in China currently available within four weeks.

Ongoing demand issues have reportedly caused Tesla to run the Shanghai Gigafactory at a reduced production schedule since last month. In addition, the plant will take an extended 12-day break for the Chinese New Year.

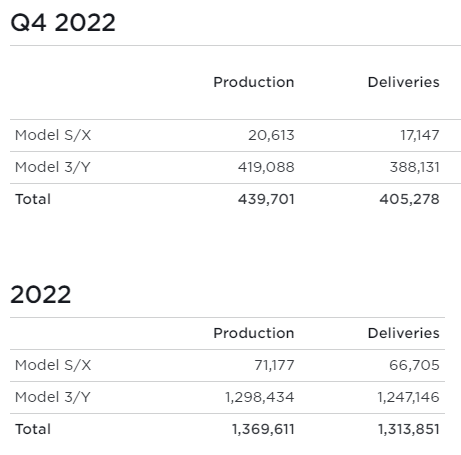

To stimulate demand, Tesla recently offered steep discounts in all major markets but this hasn’t stopped Q4 deliveries from falling well short of expectations:

Company Press Release

While the company’s growth rate for the full year exceeded 40%, year-over-year growth slowed down to 31.3% in Q4.

Particularly the increasing delta between produced and delivered vehicles is concerning.

3. Elon Musk

Would I have ordered my Model Y with the knowledge of Elon Musk’s most recent antics? To be perfectly honest, I am not sure and even Tesla perma-bull Gene Munster is concerned with Musk’s erratic behaviour, distraction from Tesla and apparent changes in political messaging causing long-term damage to the Tesla brand.

Quite frankly, following the last couple of months I would actually support Elon Musk moving to Twitter full-time and leave Tesla to capable and focused management with more adequately-sized ego.

4. Competitive Fears

Yes, competitors continue to ramp up EV production but the majority of analysts doesn’t seem to be concerned about Tesla losing its global lead anytime soon.

For example, Piper Sandler analyst Alexander Potter encourages investors to “stay grounded in the data” and while growth could easily slow this year due to recession, rising interest rates and “tapped-out” demand, the company’s market share is not “suddenly succumbing to a wave of new competition“.

While Morgan Stanley analyst Adam Jonas believes 2023 to be a reset year for the EV market, he also thinks Tesla might be in the position to actually extend its lead versus competition.

Baird analyst Ben Kallo also acknowledges potential demand issues but believes Tesla to be best positioned as EVs continue to take share of the total market due to the company having “many demand levers to pull including an increase in vehicle leasing and additional supercharging incentives“.

Bottom Line

While concerns regarding the recent actions and distractions of CEO Elon Musk are certainly valid, Tesla’s key near-term challenge will be to balance supply and demand in important markets like China, the U.S. and Europe.

Undoubtedly, reduced output and increased discounts will hurt both the company’s growth and margin profile while at the same time impacting cash flows.

The current analyst consensus calls for both earnings per share and revenue to increase by more than 30% in 2023 which I consider an optimistic assumption given the weak Q4 deliveries number, ongoing output reductions in China and likely requirement for increased discounting going forward.

After many years of being supply-constrained, Tesla will have to adapt to weaker-than-expected demand going forward.

While I expect the company, to remain solidly profitable with decent cash flow generation, analysts will likely be required to reduce estimates further as the year progresses thus providing an ongoing headwind for the shares.

Given the issues discussed above, investors should remain on the sidelines until the impact of the current market environment on the company’s growth and cash flow becomes more clear.

On a more personal note, I am nothing short of impressed by the Model Y LR which was delivered in flawless condition and is of much higher quality than expected by me. At least in my opinion, the vehicle offers plenty of value at an affordable price for buyers and remains way ahead of European challengers like the VW ID.4, Skoda Enyaq, Audi Q4 and BMW iX3.

For my part, I expect the Model Y to remain the undisputed global leader in its class for at least the next couple of years.

Be the first to comment