Sundry Photography

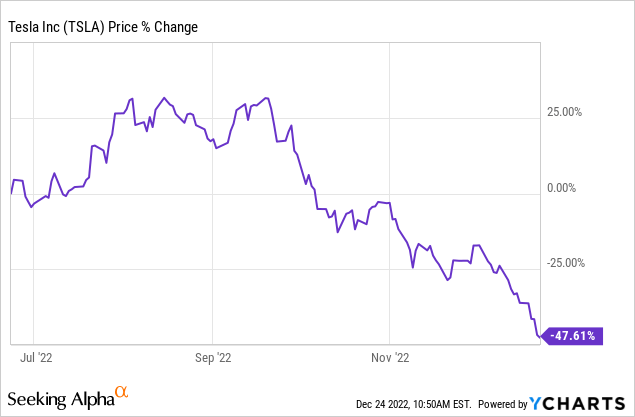

Tesla, Inc. (NASDAQ:TSLA) is a stock I’ve had zero interest in throughout the Covid bubble. Finally that’s changing. As the share price dives and earnings soar, it’s finally becoming a company you can fundamentally value. I detailed this in my December 15th piece titled: “With A Forward P/E Of 28, Is Tesla Now A Value Stock?”

With the price continuing to plummet, now we are at a forward multiple of around 22-23x, for the fiscal period ending December 2023. After that we’re in a – gasp! – teens multiple for what was previously the posterchild of Covid mania.

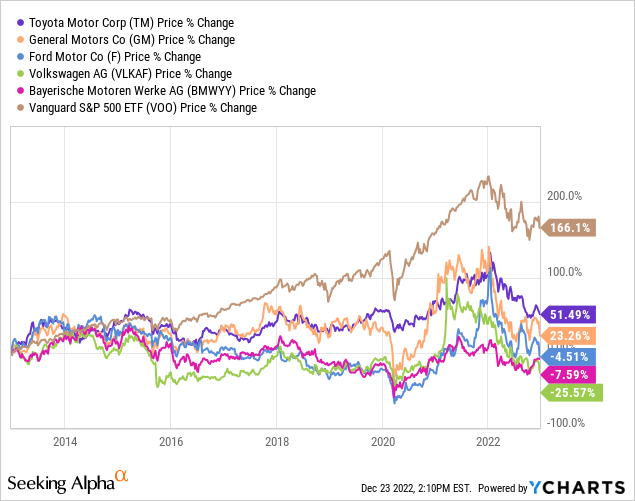

Of course, the rebuttals to what I just said will be things like BMW (OTCPK:BMWYY) trades at a P/E of 4x, or that even best of breed Toyota (TM) is 10x. I started learning over 20 years ago that investing based solely on low P/E’s also led to low returns.

Since selling my business, I live entirely off my investments, so yes I do hold lots of higher yield, low- to no-growth stocks. That’s how I classify the incumbent automakers, and frankly, I feel there are better risk/reward industries for that type of investment. Instead of these debt-laden and pension-bloated ICE (internal combustion engine) makers, who now have to cannibalize those sales with their money-losing EVs (electric vehicles).

If you disagree, just look at their multi-decade history. YCharts doesn’t allow me to generate this for 20 or 30 years, but trust me, that underperformance is just as ugly. If they couldn’t deliver alpha during the days of 100% ICE, how are they going to do so during the secular transition to EV?

You should not expect Tesla to trade at an earnings multiple comparable to the legacy automakers. In summary, here’s why:

- Tesla is an EV company from the ground up. They are not going through the messy manufacturing transition from ICE.

- Tesla, being an entirely EV company, receives regulatory credits for free. They have a surplus. Meanwhile almost all other automakers have a deficit, so they need to buy credits from Tesla and others, in order to offset their ICE sales.

- Tesla has cut out the middleman; the dealership. Granted, margins on new vehicle sales are minimal for dealers. Still, that’s more money for Tesla.

- Tesla is not drowning in debt and pension obligations. In fact, they have net cash. Yes, a large portion of the automakers’ debt comes from the financing of vehicle purchases. However, contrary to consensus, this is higher-risk debt. How many people do you know that are in way over their head on a fancy new car or truck, relative to their job security and income in a boom-and-bust economy?

- Tesla has technology superiority. I understand some facets of this lead are debatable but overall, even the bears agree it’s true.

- Tesla has other bets, such as those related to FSD. If that and other bets are successful, even if they fall far short of Cathie Wood-like projections, it will still mean a massive revenue boost. The same cannot be said about the largest incumbent automakers.

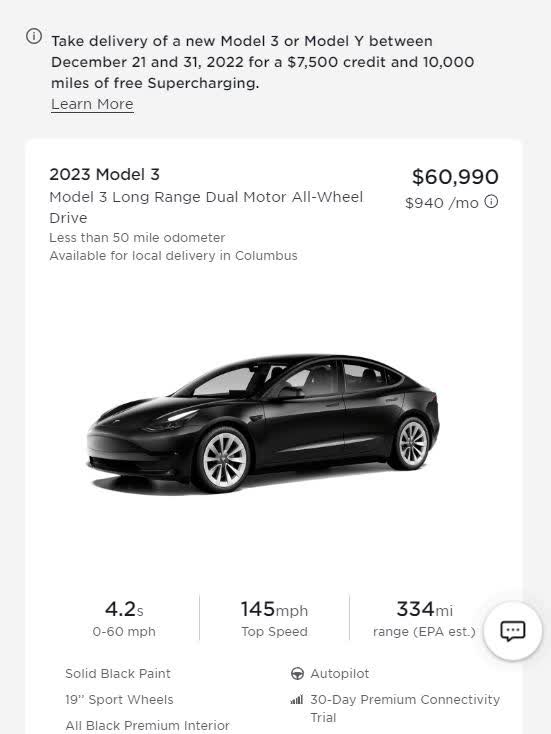

If sales are so good, why the 12% discount?

Tesla

The $7,500 discount equates to over 12% on the above Model 3. That’s a lot for a company that normally doesn’t discount!

To be clear, they are not offering a fixed percentage discount, as the realized percentage will vary based on the purchase price.

So why $7,500?

Because of the Inflation Reduction Act, a misnamed law if ever there was one. It includes a $7,500 EV tax credit. Not just for any EV, though. It stipulates where not just the cars are assembled, but also their batteries and where their materials are sourced. Must be North America or no credit.

Previously, it didn’t matter where the cars were made or how much they cost. Even the Bentley SUV hybrid qualified. Due to the 200,000 vehicle cap per manufacturer, Tesla sales haven’t qualified for quite some time.

That all changes on January 1st, as the manufacturer cap is being eliminated. Once again, folks who can afford an $80k car are also getting a $7,500 tax credit to um, reduce inflation?! Well regardless of this logic, it’s great news for Tesla.

Not so much, though, if you were buying a Tesla this month, or really anytime since the legislation passed in August. If your adjusted gross income is <$150k ($300k for joint filers), you basically save $7,500 by waiting until January 1st to take possession of your new car.

With that, of course the domestic inventory was building up in Q4. Is it any wonder why Tesla decided to match the upcoming tax credit, to move this inventory now?

If the share price didn’t fall off a cliff, they probably would have waited. They started with a $3,750 discount on December 1st. With a near 30% decline since then, it’s understandable why they stepped it up to $7,500. They know they need blowout delivery numbers for the quarter, to hopefully reverse the trend.

Discounting some vs. all sales

How much will the $3,750-$7,500 bring down the average selling price for Models 3 and Y?

Maybe not much at all.

They essentially waited ’til last minute in the year to discount, despite the 2023 credit being known since August. The question is how many people since then were postponing their purchase, that we don’t know.

Given the income threshold, for some the upcoming credit didn’t matter anyway since they didn’t qualify. For them, it actually made sense to buy one now from inventory, even if it wasn’t the exact color and features desired, because it would be discounted $7,500 through December 31st.

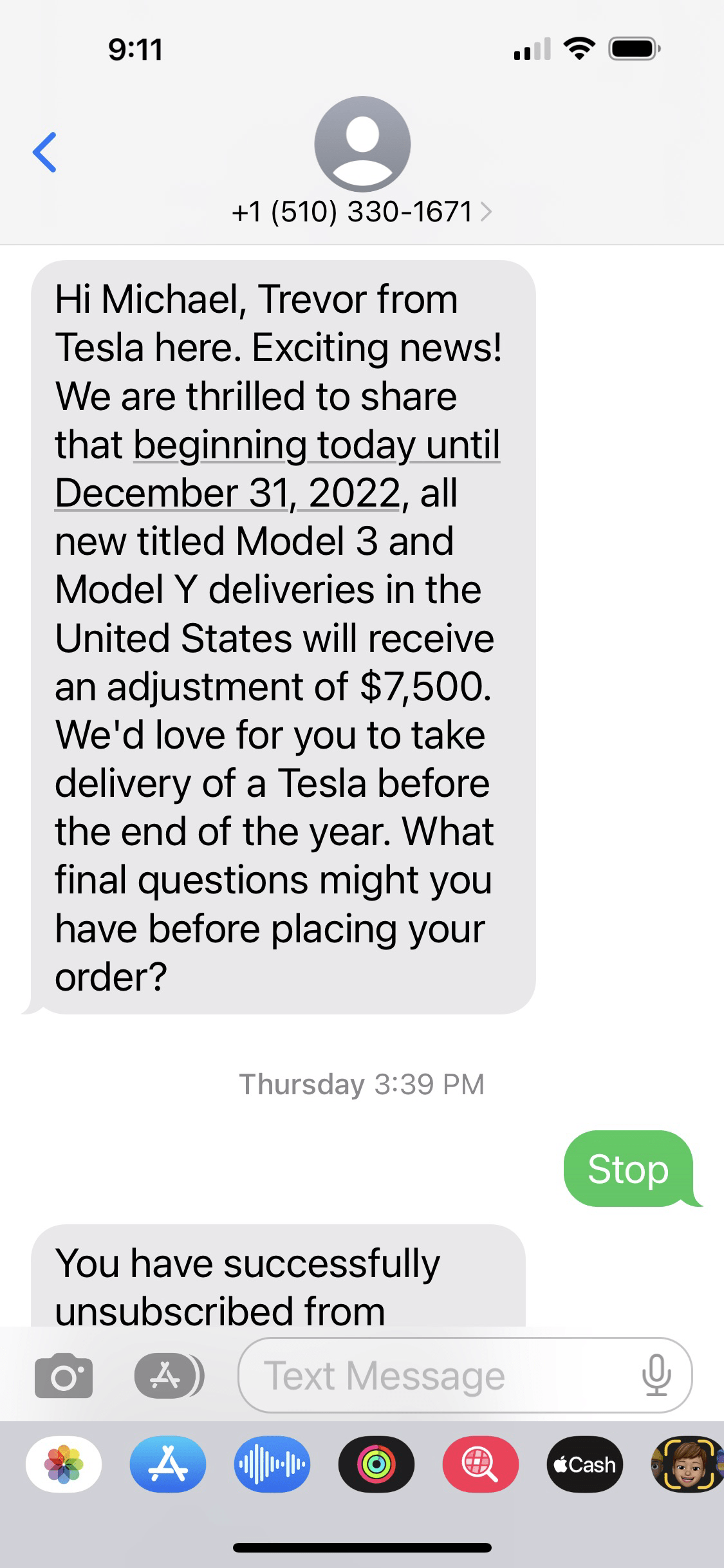

I’m in Los Angeles and received the text:

from own phone

Yeah I had to tell the so-called Trevor to stop. This is Tesla’s general text number for deliveries and more, not a personal line. It’s an automated marketing text made to sound personal.

I went on Tesla’s website that morning and only saw a few dozen cars within 50 miles. When I checked a day later for the purpose of this article, on Friday the 23rd, there were ZERO cars available within 200 miles of Los Angeles.

I did find some throughout the country, within 200 miles of random zip codes, but by the morning of Christmas Eve I couldn’t find any.

When they were available, they were all the higher cost packages. Nothing close to base models were being discounted for $7,500.

That being said, on Christmas Day I did happen to drive past their Long Beach store. This is one of their few actual stores (not just showrooms) in Los Angeles. The parking lot was packed, but given no inventory for purchase, not sure the explanation there.

The takeaway?

Tesla has probably cleared the inventory. Yes, with discounting, but it should bode well for Q4 deliveries domestically.

China, on the other hand, remains a wild card. They did halt production at Shanghai slightly early, on the 24th, as part of the planned year end break. That hasn’t happened before. With no reason being given, we don’t know if its demand or Covid related. It’s possibly the latter, given that sources have reported illnesses at that Gigafactory and supplier plants.

Q4 deliveries should be reported within the first few days of January. The otherwise bullish Dan Ives at Wedbush is not sounding sanguine. Criticizing Musk and lowering estimates to 410-415k (vs. prior 450k). The street’s whisper number is around 435k.

If Tesla disappoints even after the discounting, then it will certainly be time to re-evaluate 2023 projections. That said, there is a chance the opposite may come, with Tesla reporting blowout numbers for deliveries. Don’t be too bearish.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment