georgeclerk

The UK is expected to see a recession in 2023 if it’s not in one already. Economists at Goldman Sachs predict that the UK economy will shrink by 1.2% this year, as the high cost of living continues to reduce consumer spending.

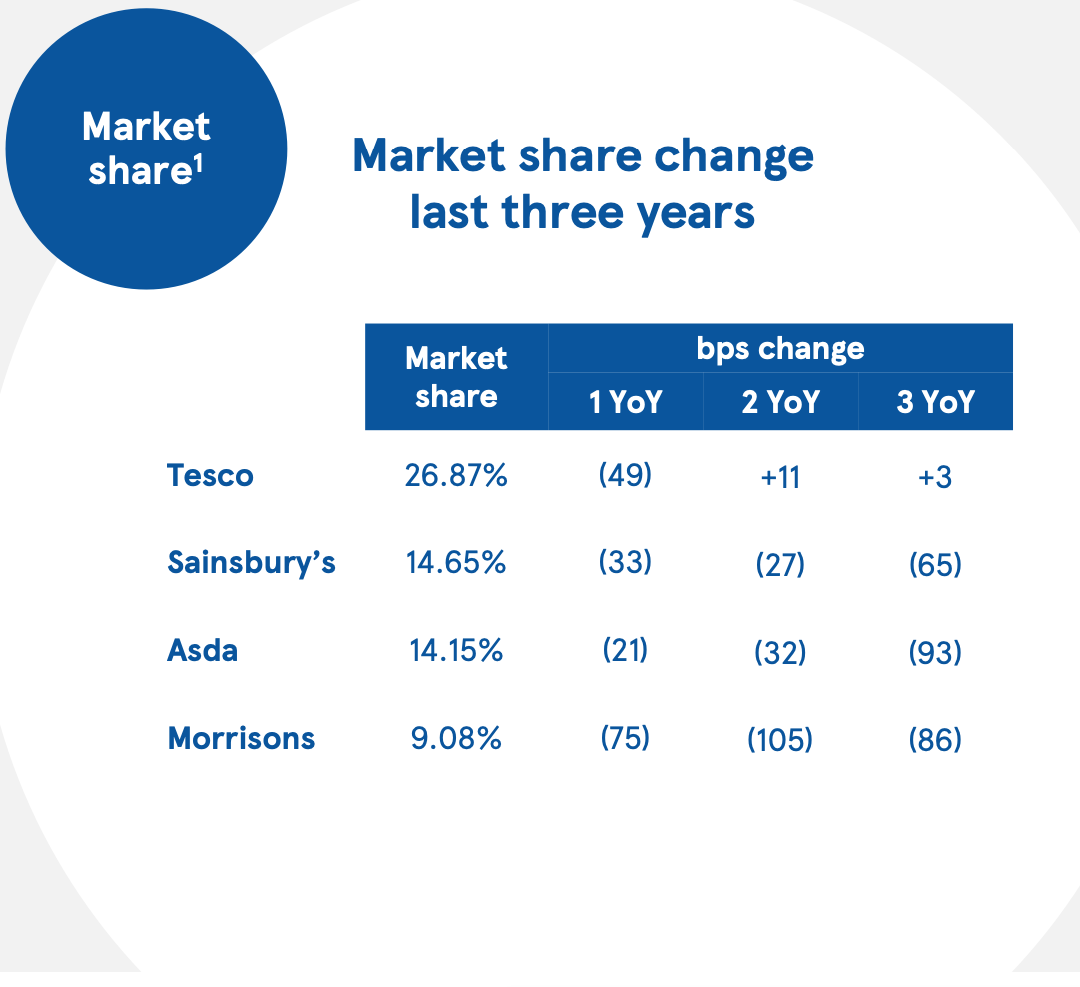

But this doesn’t have to be bad news for Tesco (OTCPK:TSCDY). At such times, defensives can be safe investing bets because while households might cut back on discretionary spending, spending on basics is still required. The grocer also has the advantage of being the UK’s biggest. Moreover, it has also gained market share over the past few years (see chart below). TSCDY has also fallen by 27% over the past year. Even though its price has recovered from the lows it saw last year, it’s still below levels pre-pandemic levels.

Source: Tesco

Keeping this in mind, here I make an assessment of what’s next for Tesco’s price based on its:

- Financial Performance and projections

- Market valuations based on both trailing twelve months [TTM] and forward basis

- Dividend yield, projections and safety

Revenues strong, profits weaken

First, its performance. For the first half of the current financial year (H1 2022/23, Feb 27, 2022-Feb 26, 2023), its revenue continued to grow by 6.7% year-on-year (YoY). This is notable considering that the base period was one of the lockdowns, which had seen a strong performance. Its sales at constant current have grown less, but they have risen too (see chart below).

Source: Tesco

However, its profits haven’t kept up in the same way. In H1 2022/23, statutory operating profit has slumped by a huge 43.6%, while diluted earnings per share [EPS] are down by almost 68%. The situation doesn’t look quite as dramatic when we consider the adjusted numbers. Operating profit is down by 9.8% and EPS by 4.9%. The gap between the two numbers at the operating level is on account of asset impairment charges. Even though adjusted numbers have seen a smaller fall, it doesn’t take away from the fact, however, that the environment isn’t quite as friendly to Tesco’s earnings now as it was in the last financial year.

High inflation impacts the outlook

Rising cost inflation, reflected in the cost of revenues is the big reason for this since they account for 94% of revenues. The number grew by 7.6% YoY in H1 2022/23, which is higher than the 4.5% increase seen last year. If it has grown at last year’s rate, Tesco’s operating profits would likely have been significantly higher this year too.

Underwhelming profits have a toll on its outlook. The company now expects retail adjusted operating profit, which makes up for most of its operating profit, to be in the range of £2.4-2.5 billion for the full year. This is a downgrade from the £2.4-2.6 billion figure the company had initially pencilled in. It also reflects that on average a 7.5% YoY profit decline is expected.

Interestingly though, the average decline is less than the 10% decrease seen in the figure in H1 2022/23, indicating that the second half of the year might be better for profits. We will have more information on this once some of the numbers for Christmas spending and the third quarter are made available later this week.

Fairly valued or not?

This brings me to the Tesco price, which is down by 28% YoY. Because of the decline in earnings, however, this isn’t entirely a reason to buy it right now, however. Its price-to-earnings (P/E) based on TTM statutory earnings, is at 20x, which is just a shade lesser than 20.6x for the Consumer Staples sector. Similarly, its forward P/E isn’t very different from the sector either.

However, its forward adjusted P/E makes some case to buy Tesco ADRs. At 11.8x, it’s much lower than the 19.1x figure for the consumer staples sector. Further, its TTM price-to-sales (P/S) at 0.3x is significantly lower than 1.15x for the sector, and its forward P/S also shows the same trend.

On balance, the market multiples do suggest that the ADRs could rise from here. But the potential price based on these varies widely depending on the ratio considered. Besides this, it’s worth keeping in mind, that it’s already trading at above its historical average P/E of 17.6x.

Macros stay unsupportive

In a good year, it would be easy to make a case for why its P/E could rise higher. But 2023 is not one of them. Inflation continues to stay high, and this will tell on its profits. The company has also flagged reduced volumes in the UK, its biggest market, because of the post-pandemic normalisation of demand. With its margins already having declined because of higher costs, it remains to be seen whether it can pass on any more cost increases to customers. In essence, this means that it’s possible for its revenues to be hit this year.

Dividend cuts possible

This can also tell on its dividends. Its dividend yield isn’t bad at 4.8%. And its 4-year average dividend yield is actually at an impressive 9.2%, so it does remain attractive for the income investor. At the same time, I think a dividend cut is in the offing. Its TTM dividend payout ratio is at a huge 89%. Combined with the fact that it expects earnings to be less for 2022 compared to the year before, it’s not a far-fetched projection. With the verdict for 2023 not looking great either, we might just see two consecutive years of dividend declines.

What next?

On balance, it’s clear that while Tesco ADRs can rise from their current level and the dividends are neat too, there are risks ahead. The macro environment is unsupportive and will continue to remain so for at least the first half of the year until inflation starts cooling off meaningfully. Despite being a solid defensive play, as long as this cyclical weakness shows up in its numbers, its price trend can stay weak. It doesn’t help that it appears as if dividends might be cut soon too.

I’d wait until it releases its next financial result to see where it’s headed. If the decline in profits subsides in the second half of 2022/23, that would be a positive. I’d watch out for the dividend announcement too. But it’s not until the second half of next year, that we can hope for a real turnaround. And the release of those numbers is more than a year away.

Tesco isn’t a bad company by any stretch. As a regular customer, I’ve been very happy with it for a long time. But it’s not in the best place in the economic cycle. I’d hold it.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment