Marcus Lindstrom

Tech companies are making a lot of headlines, but for all the wrong reasons. For example, who would have thought only several months ago that even Google (GOOG) would be at risk of being disrupted by Microsoft’s (MSFT) new AI-powered Bing search platform?

For those who can’t keep up with the dizzying array of tech innovations, investing in tangible assets such as real estate may be a better idea. This brings me to Terreno Realty (NYSE:TRNO), which owns very high quality assets in premier markets.

It seems like quality still wins the race, as I found TRNO to be fairly priced the last time I visited the stock near the end of 2020, and it still managed to outperform the market with a 17% total return, outpacing the 12% return of the S&P 500 (SPY) over the same time period. In this article, I highlight the durable attributes that make TRNO a buy at present, so let’s get started.

Why TRNO?

Terreno Realty is a self-managed industrial REIT that owns and operates properties in six supply-constrained major coastal markets of Los Angeles, NY Metro, SF Bay Area, Seattle, Miami, and Washington D.C. It specializes in acquiring functional and flexible infill real estate at the “intersection” of growing demand and shrinking supply.

As of the end of 2022, TRNO owned 252 buildings aggregating to 15 million square feet and had 46 improved land parcels consisting 161 acres, giving it plenty of growth runway.

TRNO exhibits very strong operating fundamentals, with a 98.6% occupancy rate as of the end of the fourth quarter, comparing favorably to 95.5% in the prior year period. It’s worth mentioning that this includes newly acquired properties that have yet to be fully stabilized, and same store occupancy is virtually at capacity, with a 99.5% occupancy rate.

The true growth story lies in TRNO’s very strong 45% blended cash rent spread on new and renewed leases during Q4, and 49.5% for the full year, signaling very strong tenant demand that’s well ahead of the rate of inflation.

TRNO is also showing no shortage of acquisition opportunities, as it acquired 4 more properties during Q4, with 2 being in Los Angeles, 1 in New York, and 1 in Miami. With the exception of 1 property with a 2.5% cap rate (in LA), the other properties came with cap rates ranging from 5.2% to 6.2%. Plus, TRNO is also redeveloping a property in Southern California with an estimated stabilized cap rate of 6.1%.

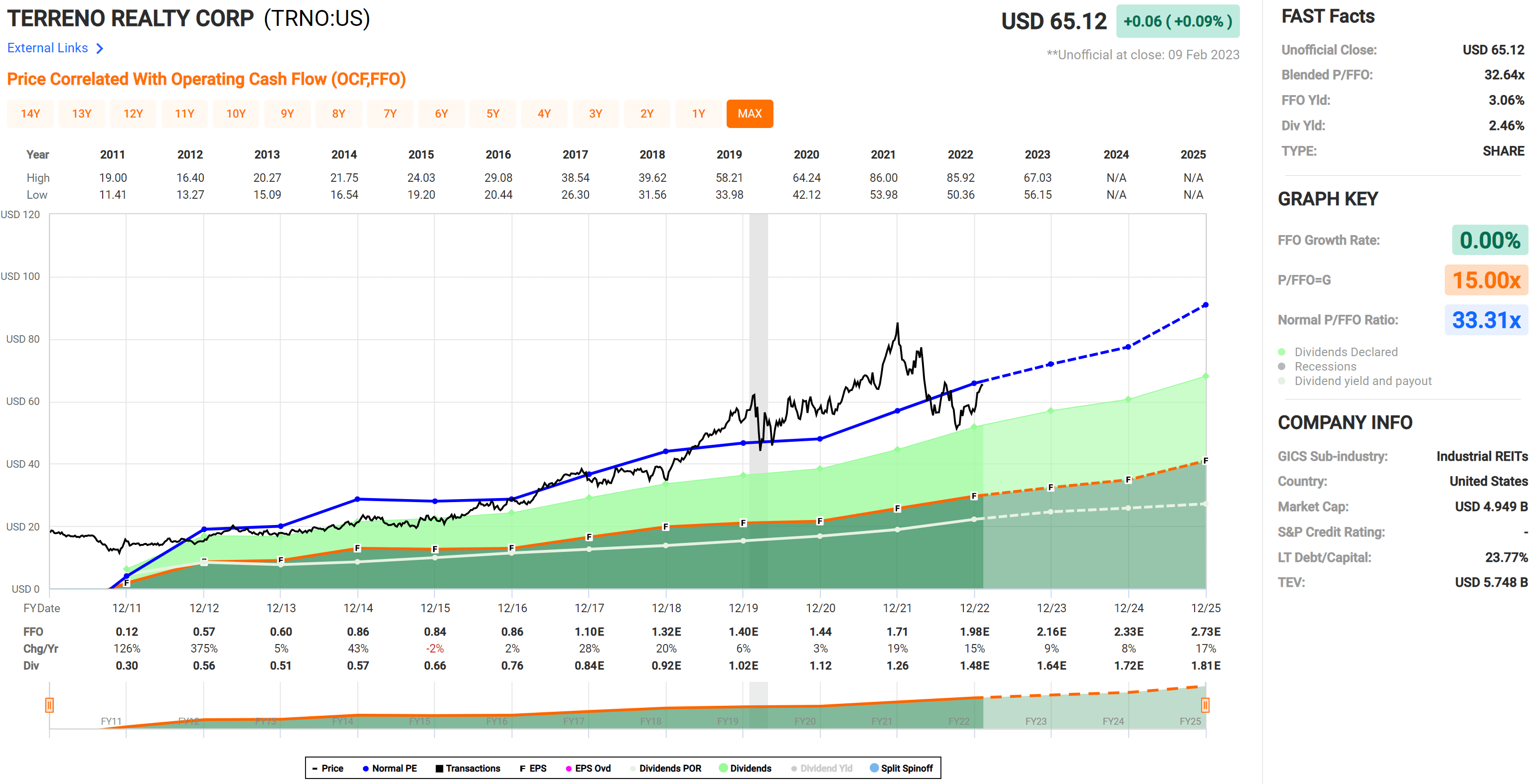

This compares favorably to TRNO’s cost of equity, which at the current price of $65 with a forward P/FFO of 33 translates to a 3% cost of equity. This is perhaps why management announced a 5 million share offering on February 9th, which would enable it to capture a healthy investment spread. Management expects to use the proceeds for future acquisitions, including the acquisition of a 121 acre project in Miami’s Countyline Corporate Park.

Meanwhile, TRNO maintains a solid balance sheet with a net debt to EBITDA ratio of 4.8x and no debt maturities this year, thereby mitigating the impact of higher interest rates. It also has no borrowings under its $400 million revolving credit facility, giving it plenty of flexibility.

While TRNO’s 2.5% dividend yield isn’t particularly high, it is well above that of the S&P 500, and comes with a 12.5% 5-year dividend CAGR and 9 years of consecutive growth.

Lastly, TRNO currently trades well below its 52-week high of $81 at its current price of $65 with a forward P/FFO of 33. While this may seem pricey on a standalone basis, I believe TRNO’s aforementioned operating strengths including its high cash rent spreads justify the valuation. Analysts also have a consensus Buy rating on the stock with an average price target of $67.

FAST Graphs

Investor Takeaway

Given the above-mentioned attributes and growth prospects, I believe TRNO is a buy at present despite its high valuation. It maintains strong operating fundamentals and carries a solid balance sheet, positioning it well for further acquisition opportunities.

As such, investors who are accustomed to paying a premium valuation for tech growth stocks may want to consider this “hard asset” growth stock that actually pays you to own it.

Be the first to comment