JIRAROJ PRADITCHAROENKUL/iStock via Getty Images

As one of only two companies in the world that can produce testers for the most cutting-edge semiconductors, Teradyne (NASDAQ:TER) has a very strong competitive moat. As a reminder, Teradyne is a leading company in the design and manufacturing of semiconductor test equipment, and has also diversified into the industrial robots space. Its advanced test solutions for semiconductors, electronic systems, and wireless devices ensure that products perform as they were designed. Its Industrial Automation offerings include collaborative and mobile robots that help manufacturers improve productivity and lower costs.

There is currently a very interesting trend in the semiconductor space, where increasing complexities are making it harder for smaller competitors to keep up, resulting in technology leaders gaining market share and improved pricing power. This has been happening in lithography with ASML (ASML) almost becoming a monopoly, in semiconductor manufacturing with TSMC (TSM) becoming dominant in leading semiconductor nodes, and in the Automatic Test Equipment segment with Teradyne and Advantest (OTCPK:ATEYY) basically becoming a duopoly.

Competitive Moat

A factor that contributes to Teradyne’s competitive moat is that it is constantly developing new and improved test equipment, especially for the most cutting-edge semiconductors. Its products are known for their accuracy, reliability, and performance, which further enhances the company’s reputation and market position.

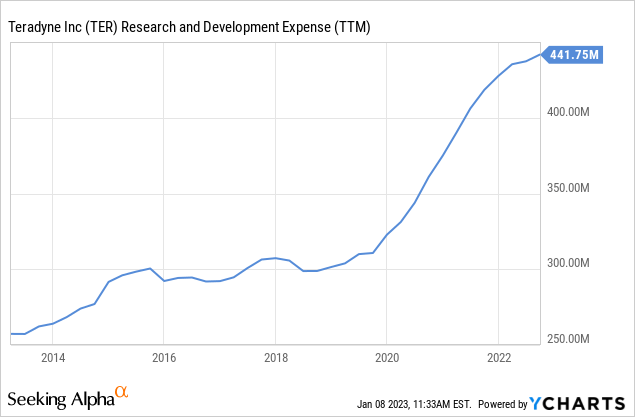

The company’s leadership position and strong profitability gives it the financial resources to further invest in R&D and increase its technological lead. As can be seen in the graph below, Teradyne has been ramping its research and development expense very meaningfully the last few years. Teradyne’s scale and global reach also give the company a cost advantage that adds to its intellectual property moat.

The Achilles Heel

While we are impressed by Teradyne’s competitive moat, we do believe it has an Achilles heel, and that is high customer concentration. In 2021 its five largest direct customers in aggregate accounted for 33% of the company’s consolidated revenues. Just Taiwan Semiconductor by itself accounted for approximately 19% of its 2021 consolidated revenues, and in 2020 it got as high as 25%.

Why is this a vulnerability? The reason is that if the company’s sales start coming from just a small number of customers, they will get increased bargaining power and could force the company to lower its prices or offer them big discounts.

Financials

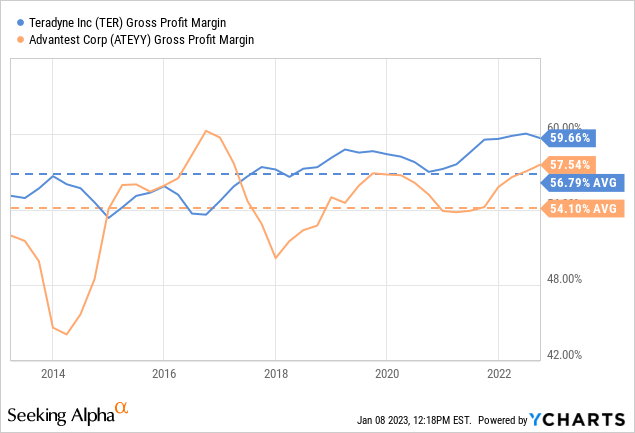

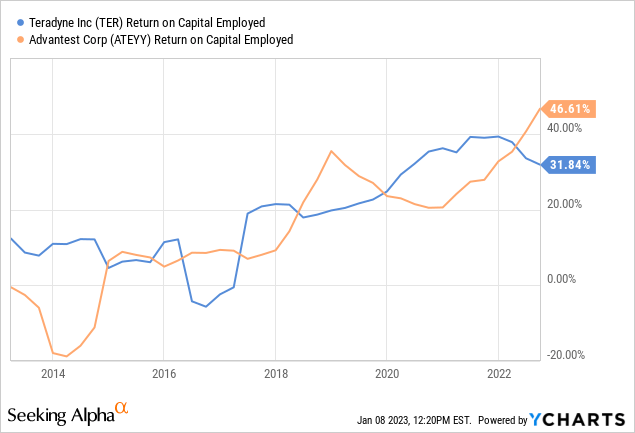

Customer concentration aside, there are signs showing that Teradyne’s competitive moat has been increasing. For instance, its gross profit margin and return on capital employed have been trending up in the last decade. Advantest has seen a similar development, which means that both companies are probably benefiting at the expense of smaller rivals.

Growth

Looking forward, global trends continue to fuel semiconductor growth, which is very positive for the company, as more semiconductor manufacturing means that more test equipment will be needed. The top three semiconductor manufacturers, TSMC, Intel (INTC), and Samsung (OTCPK:SSNLF) have announced plans to invest >$300 billion in global capacity. The semiconductor end market is expected to more than double between 2020 and 2030, which represents a CAGR of ~9%.

ASML Investor Presentation

Further fueling CapEx spend that should benefit the likes of Teradyne is the push for ‘technological sovereignty’, with programs such as the CHIPS Act promoting semiconductor investments.

ASML Investor Presentation

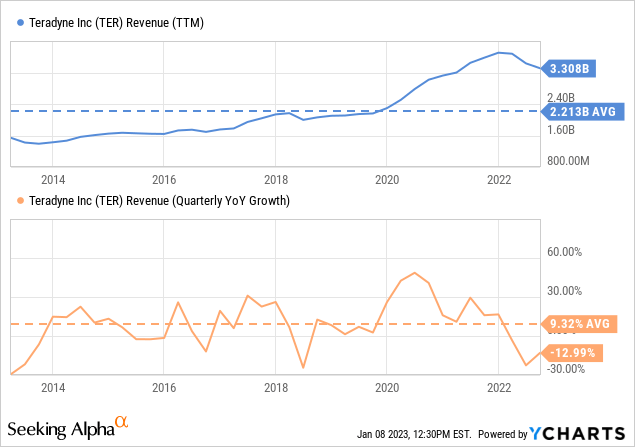

Coincidentally, the average quarterly year over year revenue growth rate for Teradyne over the last ten years has been ~9%. 2022 saw negative growth, but this is normal in a relatively cyclical industry, and we believe the company will soon return to positive growth.

Balance Sheet

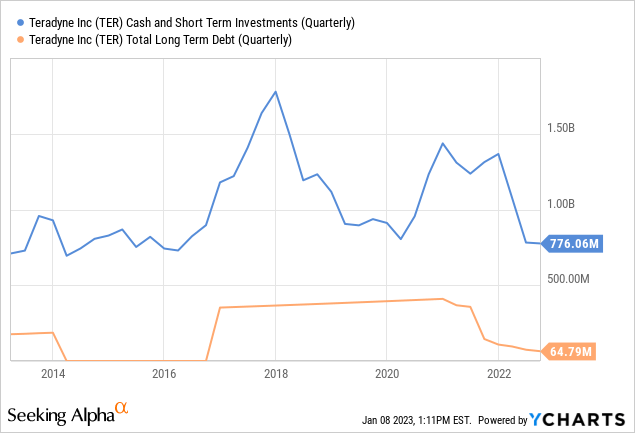

Teradyne continues to have a balance sheet in great shape, with significantly more cash and short-term investments than long-term debt. This positions the company very well to continue investing in its future.

Valuation

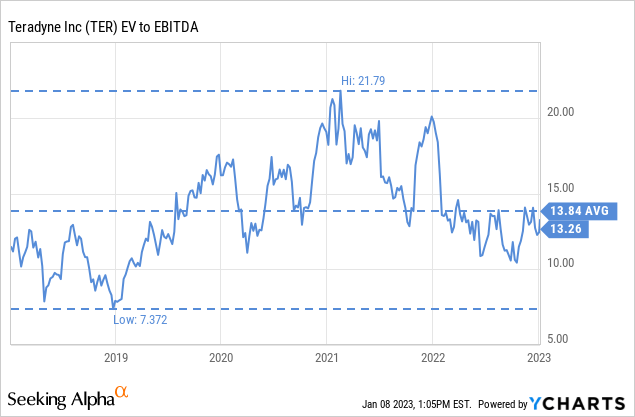

In our previous article, we focused more on valuation, and most of what we wrote remains valid as the share price has not changed that much since then. We view the current valuation as reasonable, with the EV/EBITDA multiple very close to the ten year average.

Based on the company’s 2024 Earnings Model, shares are currently trading with a P/E ratio between ~10x and ~13x the earnings the company estimates it can deliver in FY2024. We view this p/e ratio as attractive, especially considering the quality of the company and its competitive advantages.

Teradyne Investor Presentation

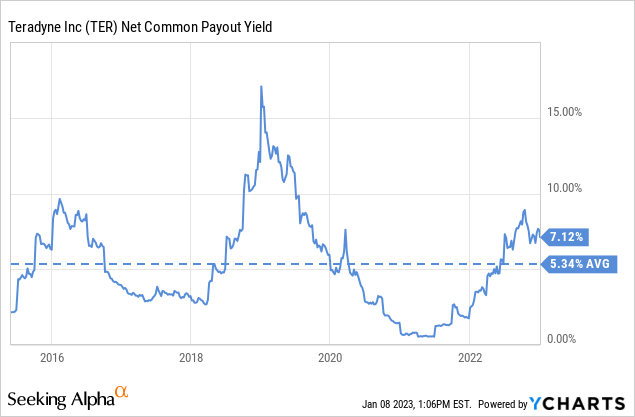

Teradyne pays a very modest dividend, but has been very active buying back shares, resulting in a high net common payout yield. As a reminder, the net common payout yield combines the dividend yield and the buyback yield.

Risks

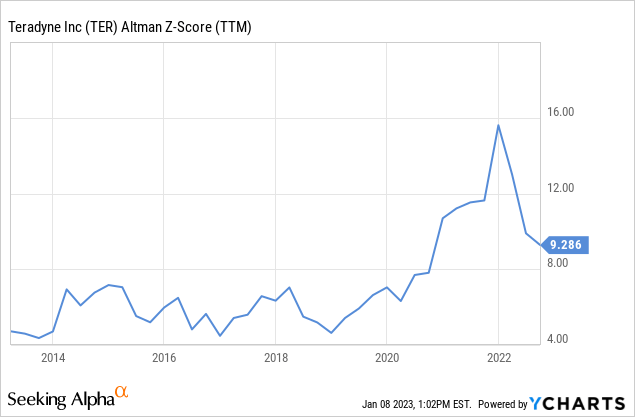

We believe an important risk is that Teradyne’s revenue is largely dependent on a small number of key customers, which can give them increased bargaining power. It is also worth noting that investors should expect significant volatility as the stock has a relatively high Beta. Another risk is that the company recently appointed a new CEO, and it remains to be seen how he manages the company. Risks are mitigated by the company’s strong balance sheet, and its impressive Altman Z-score of ~9.2x.

Conclusion

One of the key factors that makes Teradyne an attractive investment opportunity is its competitive moat, which refers to the company’s ability to maintain or improve its market position, and protect its profits from competition. Teradyne’s market leadership is demonstrated through its industry-leading margins, strong returns on capital employed, and top market share in the industry. As the company continues to grow and innovate and semiconductor technology gets increasingly complex, its competitive moat gets wider and stronger, making it an increasingly compelling investment at what we currently believe is a very reasonable valuation.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment