iLexx

Teradyne (NASDAQ:TER) is a leading global supplier of automation equipment for test and industrial applications. After pulling back over 40% over the past year, the stock may offer an interesting opportunity to own this highly differentiated company with strong long-term growth drivers. However, near-term macro concerns and the company’s high multiple are key concerns for owning the stock right now.

In this article, we will systematically examine the company’s business fundamentals, risks, financials, and valuation to help readers arrive at a more informed position to assess the risk and rewards of owning the stock.

Note: This article is for educational purposes only and does not constitute financial or investment advice. Please do your own due diligence and consider your unique financial needs and constraints before buying any stock.

Business Overview

Teradyne 3Q22 Earnings Presentation

Teradyne is a company that designs, develops, and manufactures automation equipment for testing electronic devices, including integrated circuits, smartphones, and other products. The company was founded in 1960 and is headquartered in North Reading, Massachusetts.

Throughout its history, Teradyne has developed and acquired a wide range of products and technologies that have been used to test a variety of electronic devices. Some of the key milestones in the company’s history include:

-

In the 1960s and 1970s, Teradyne developed a number of manual and semi-automated test equipment for use in the aerospace and defense industries.

-

In the 1980s and 1990s, Teradyne expanded its product line to include automated test equipment (‘ATE’) for testing integrated circuits (‘ICS’), which became the company’s primary focus.

-

In 2001, Teradyne acquired GenRad, a company that specialized in test equipment for electronic circuit boards and systems.

-

In 2015, Teradyne acquired Universal Robotics, a manufacturer of collaborative robots.

-

In 2018, Teradyne became a full-fledged autonomous mobile robot (‘AMR’) provider by acquiring Mobile Industrial Robots (‘MIR’).

Today, Teradyne is one of the leading providers of ATE and automation solutions for the semiconductor industry and other electronic device manufacturers.

ATE

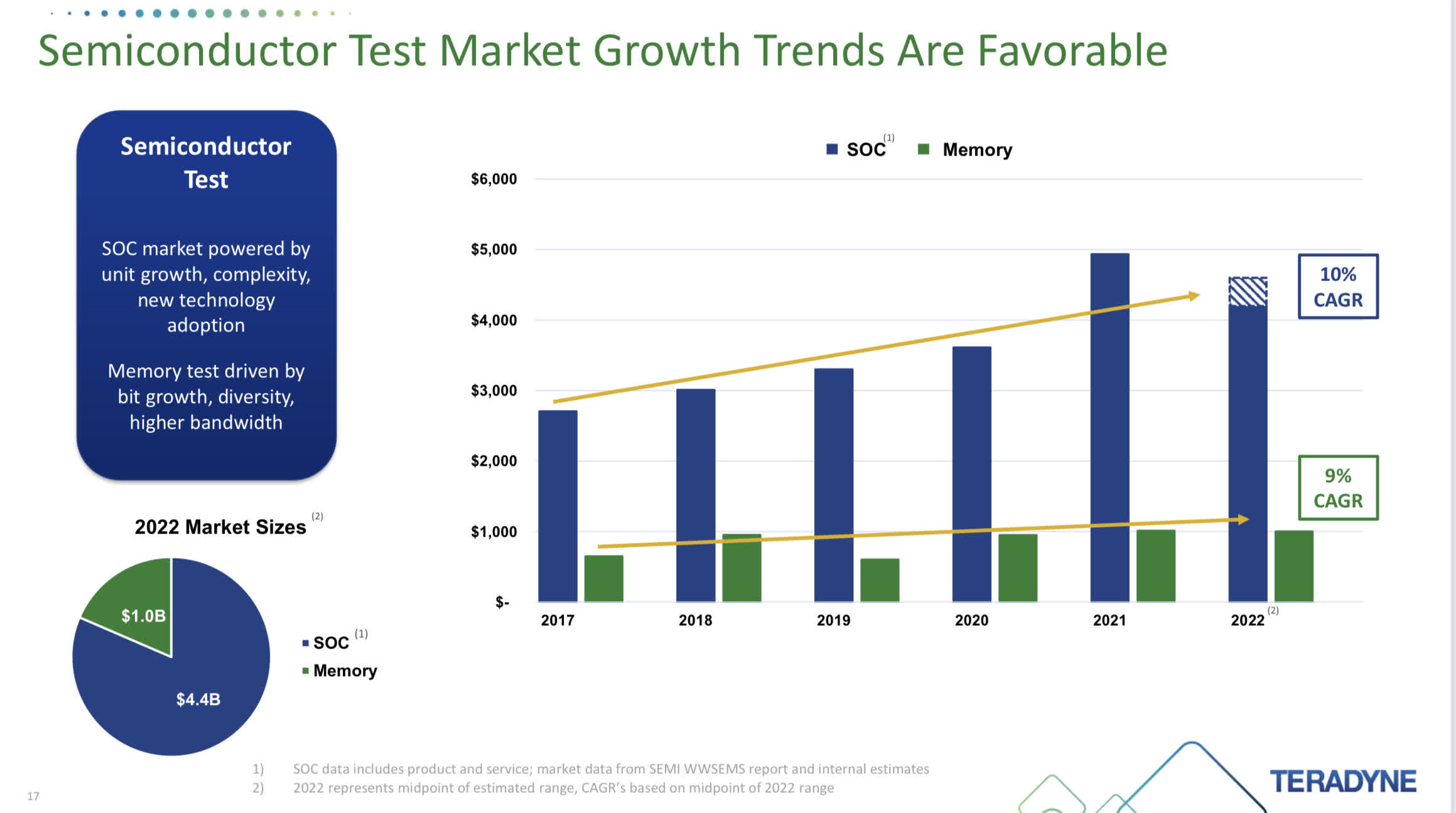

In semiconductors and memory testing, TER enjoys a duopoly with Advantest, together comprising 85-90% of the market. This business enjoys sticky relationships with major customers like Apple (AAPL), MediaTek (OTCPK:MDTKF), Broadcom (AVGO), and Qualcomm (QCOM). This business leverages to wafer fab equipment (‘WFE’) spending, which has a very promising long-term growth trajectory given the drive to manufacture semiconductors domestically around the world.

Teradyne 3Q22 Earnings Presentation

Automation

After three acquisitions, TER became the leading provider of collaborative robots, or “cobots”, with around 45% market share, as well as the second-largest player in autonomous mobile robots, or “AMRs”, with roughly 8% market share. TER’s automation business has been growing around 40% a year from 2015 through 2021, driven by low market penetration of robots, a secular shortage of labor, diminishing returns of offshoring, and fast payback of investments for cobots and AMRs. Industrial automation is expected to be a growth driver for the company. However, industrial automation is only around 10% of total revenue currently.

Competitive Advantage

Teradyne has a number of competitive advantages in the automated test equipment and automation solutions market. Some of the key advantages include:

-

Strong technology: Teradyne has a long history of developing and acquiring advanced technology for testing electronic devices. The company has a strong research and development team and is known for developing innovative solutions that address the testing needs of its customers.

-

Wide product portfolio: Teradyne has a wide range of products that address the testing needs of different electronic devices, such as integrated circuits, smartphones, and other products. This enables the company to serve a diverse customer base and to provide a one-stop-shop for all their customers’ testing needs.

-

Strong customer relationships: Teradyne has built strong relationships with its customers over the years, thanks to its reputation for providing high-quality products and services. The company has a deep understanding of its customers’ testing needs and is able to customize its solutions to meet those needs.

-

Strong market position: Teradyne is one of the leading providers of ATE and automation solutions in the market.

-

Strategic acquisitions: Teradyne has made strategic acquisitions over the years that have expanded its product offerings and allowed the company to enter new markets.

-

Diversification: Teradyne diversifies its product offering, not only in the Semiconductor industry but in other industries as well, such as military, aerospace, and health care, which helps to reduce its dependence on any one specific market.

Business Risks

Like any company, Teradyne faces a number of business risks that can affect its performance and financial results. The risks the company faces include the following:

-

Cyclical nature of the semiconductor industry: The semiconductor industry, in which Teradyne operates, is known to be cyclical. Many view WFE spending as being even more cyclical than the broader semiconductor industry, which comes with considerable near-term risks as the world potentially faces a global recession in 2023.

-

Dependence on key customers: Teradyne generates a significant portion of its revenue from a few key customers, most notably with Apple being a 20-25% customer (indirectly via TSMC). Apple sole-sources from TER and has considerable leverage to get concessions from the company, as it can threaten to switch to or dual-source from Advantest and others. WFE spending is also driven by Apple’s product roadmap, as product cycles drive considerable fluctuation in spending.

- Dependence on technology advancement: The pace of node advancement could slow more materially than expected, given Moore’s Law’s slow death over the past decades. The increase in semiconductor complexity may slow down given the rising cost of building advanced fabs or a weakening in demand environment. A slowdown in technology advancement will likely negatively impact demand for ATE.

Financials

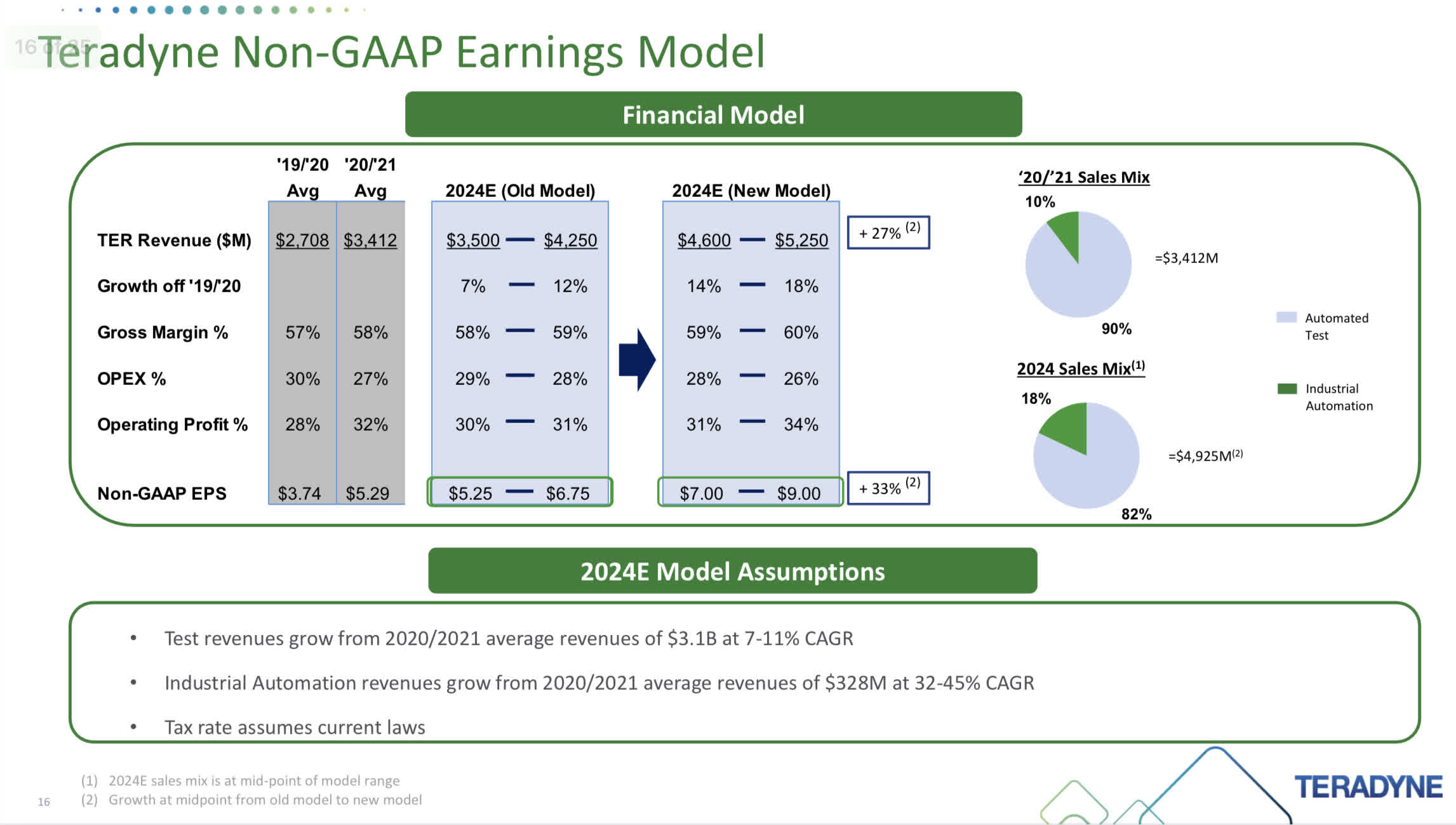

2019 through 2021 was a good growth period for TER as revenue went from $2.3B to $3.7B and EPS went from $2.86 to $5.98. However, consensus estimates expect revenue to contract 15% in 2022, and EPS to contract 32%. 2023 is expected to be another contraction year, with sales down 1.5% and EPS down 4.1%.

Looking past the weak macro environment, TER management believes revenue growth could accelerate given its mix shift to the faster growing Automation business, which is expected to go from 10% in 2021 to 18% in 2024.

Teradyne 3Q22 Earnings Presentation

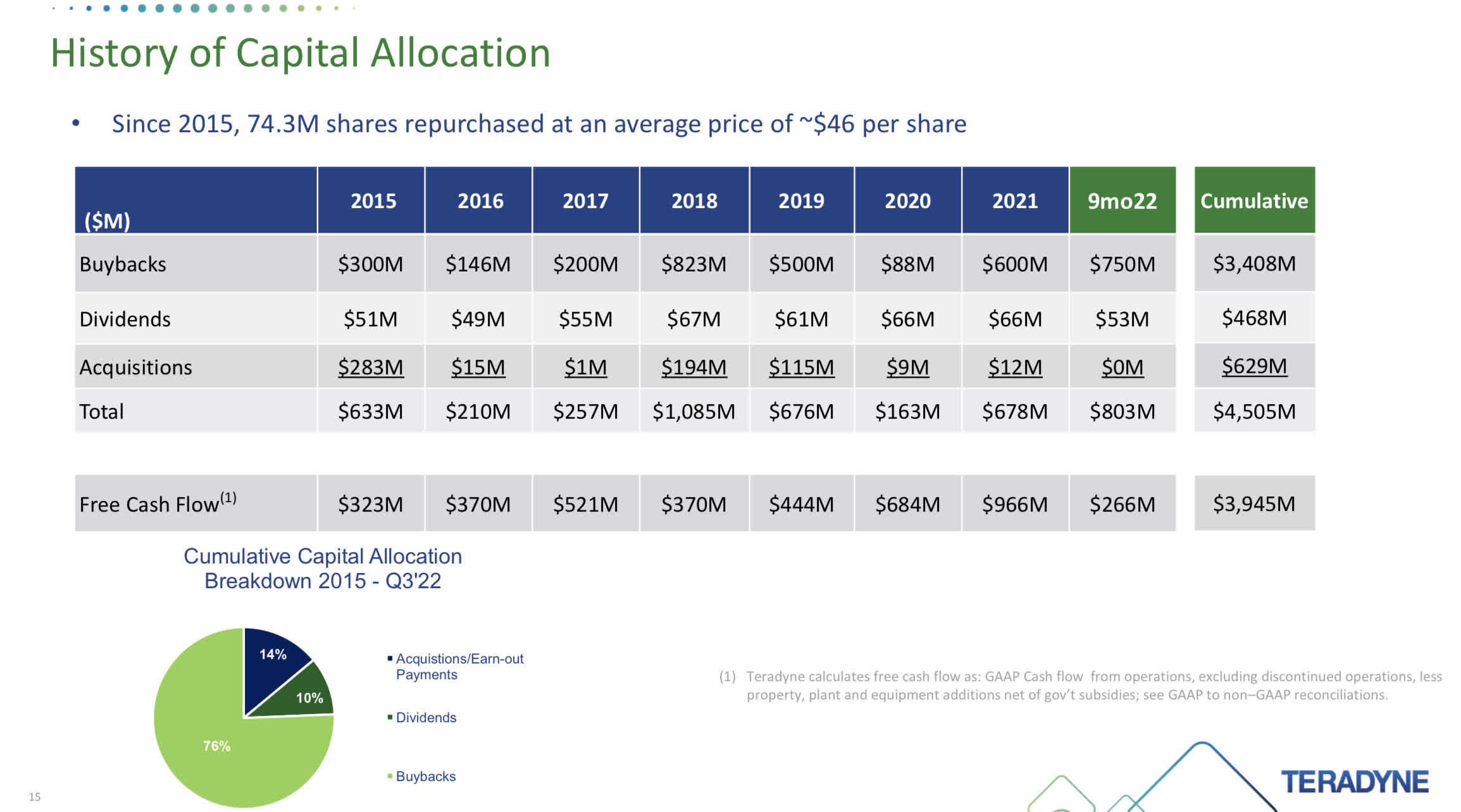

TER’s capital allocation track record has been decent. The company purchased $3.4B of its own stock at an average price of ~$46 per share since 2015. This compares favorably to the current market cap of $14.8B and stock price of ~$95 per share. TER pays a modest dividend, with the stock currently yielding 0.46%, which is well below the S&P 500’s ~1.7% yield.

Teradyne 3Q22 Earnings Presentation

Valuation & Trading

Despite a negative 41% 1-year stock return, TER continues to trade towards the high end of its earnings multiples. On next-twelve-months consensus estimates, TER trades at 24x P/E vs. a 5-year median of around 18-20x.

The stock’s FCF yield is only 4%, towards the bottom of its 5-year range.

Sentiment on the stock remains negative. Down 41% over the past year, TER significantly underperformed the iShares Semiconductor Index (SOXX) at -29% and the iShares Global Industrials Index (EXI) at -10%. Despite this underperformance, short interest in the stock went from 2.4% in November 2022 to 3.4% currently.

Conclusion

Teradyne is undoubtedly a great American company with very unique assets, underpinned by strong secular growth drivers. However, the story and valuation seem to be well ahead of the economic realities of the looming global economic recession. While the company has experienced tremendous growth in recent years, its main ATE business is highly cyclical and is a risk of a large correction, one significantly larger than consensus expectations for a modest contraction in 2023. While industrial automation and cobots are great investment themes, this business is only 10% of its total revenue and is a business untested by a weak macro environment. Given these considerations, I remain on the sidelines on Teradyne.

Be the first to comment