Lintao Zhang

I am downgrading Tencent (OTCPK:TCTZF) stock to “Hold”, as regulatory risk for the world’s largest gaming company resurfaces with a “Bang”. On December 22th, Beijing drafted a set of directives that are designed to curb consumption of gaming content, both relating to time and monetary spending. Specifically, the new regulatory framework is designed to significantly limit in-game rewards linked to regular log-ins and purchases, a notable part of Tencent games’ monetization strategy. This announcement prompted shares in Tencent (HK listing, ticker 0700) to fall by more than 12%. Shares for key competitor NetEase (NTES) (HK listing, ticker 9999) dropped by close to 25% respectively.

Needless to say, the latest regulatory commentary brings back fears of a significant and broader crackdown in the Chinese gaming landscape. For context, in 2022 Chinese state media characterized gaming as “spiritual opium,” followed by a suspension of approvals of new gaming titles for almost a year. Additionally, Chinese children were restricted from playing video games for more than three hours per week.

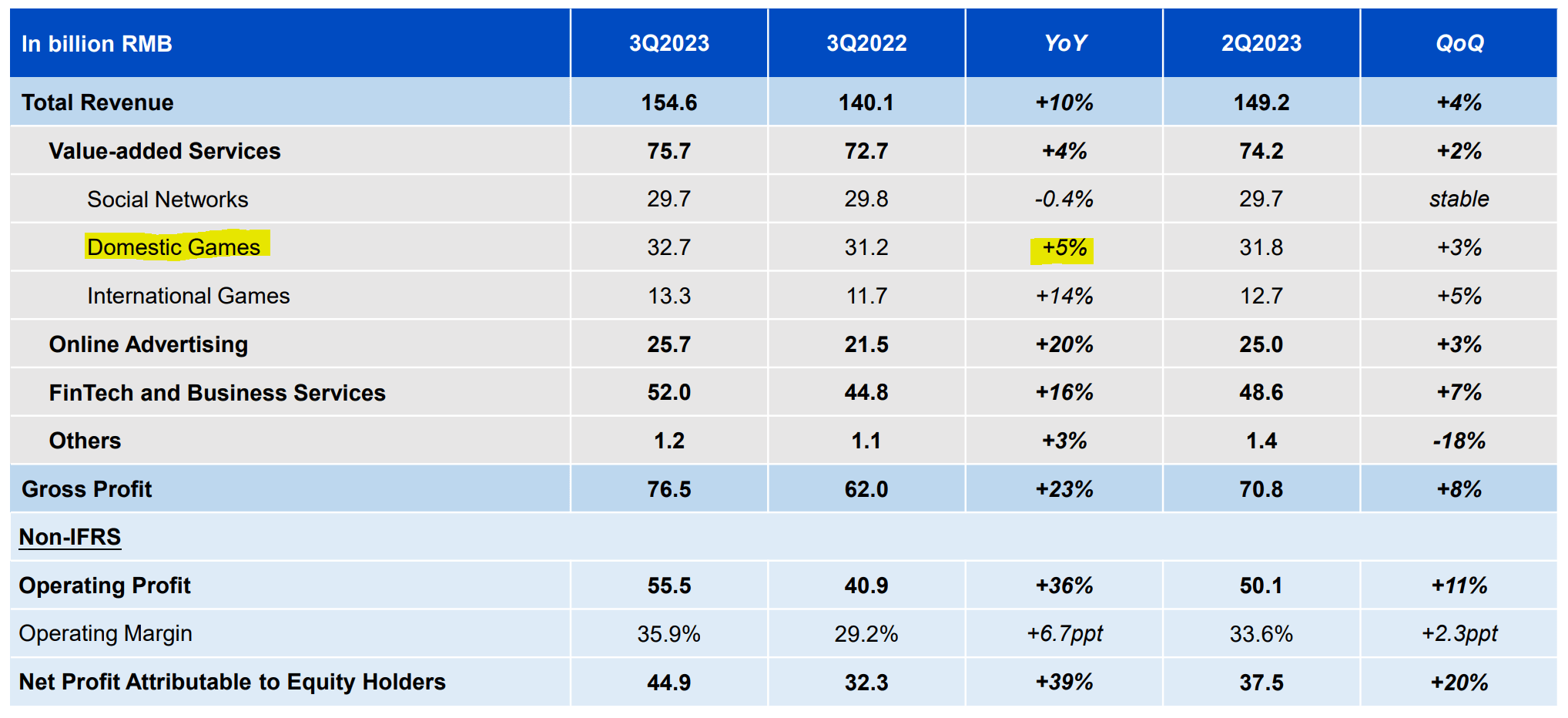

In my opinion, market participants are not necessarily overreacting to the news, pushing Tencent double-digit percentage lower in just one trading session. Albeit Tencent’s domestic gaming segment accounts for only about 20% of the group’s topline revenue, investors should consider that the regulatory crack-down in gaming may suggest a broader government-led rectification of the Chinese digital economy, especially social media, which would bring Tencent’s broader business model into exposure for headwinds. Moreover, investors should not forget that Tencent’s key verticals in Domestic Gaming and Social Networks have already been struggling with challenged momentum, with Q3 2023 vs. Q3 2022 revenues expanding by only 5% and -0.4% YoY.

Tencent Q3 2023

It is true that Tencent shares are trading cheap currently, with shares down more than 60% from all-time highs, and unlevered earnings (EBIT) valued at an enterprise multiple of about 12%. However, I am cautious to argue that Tencent stock presents itself as a bargain. One major issue that I am seeing with Tencent shares relates to the company’s unappealing shareholder distributions, which certainly are below levels that would justify investing in such a risky equity asset. For the trailing twelve months, Tencent has distributed about $6.2 billion in form of share buybacks and 1.2 billion in form of dividends, partially offset by -$3.4 billion dilution for share based compensation, bringing the net equity payout to about $4 billion only. Compared to a $375 billion market capitalization, the payout is quite unattractive, at ~1% yield. Why not invest into less risky, higher-yielding U.S. Treasury assets?

Valuation Update: Lower Target Price

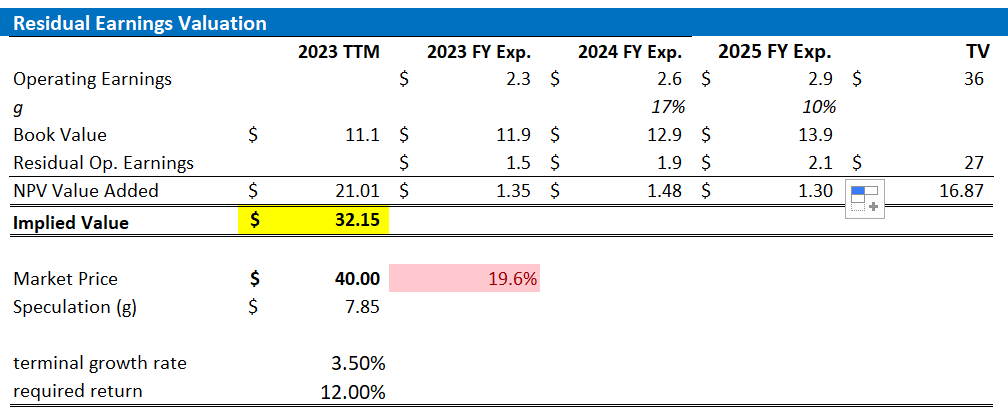

I update my EPS projections for the Tech giant in line with analyst consensus revision, according to data collected by Refinitiv: Accordingly, I now anchor on EPS equal to $2.3 for FY 2023, vs $2.55 estimated previously. Moreover, I adjust my EPS input for 2024 and 2025, to $2.6 and $2.9, respectively.

I continue to base my valuation model on a reasonable 3.5% terminal growth rate (one percentage point higher than estimated nominal global GDP growth). However, I pump my cost of equity estimate by as much as 200 basis points, to 12.0%, reflecting the heightened regulatory risk overhang.

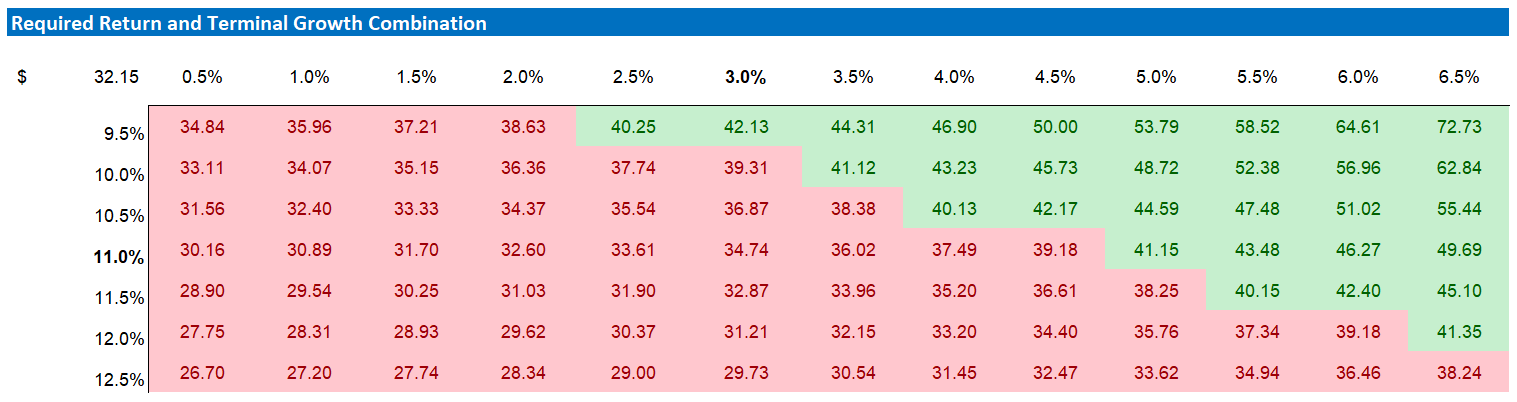

Given the adjustments as discussed above, I now calculate a fair implied share price for TCEHY equal to $32.15, seeing downside to the current valuation level of the stock (although I point out that much of the downside relates to the 12% cost of equity assumption; That said, investors who would like to test a higher cost of equity may reference the sensitivity table enclosed).

Analyst Consensus; Company Financials; Author’s Calculations

Below also the sensitivity table, which tests different assumptions for cost of equity (row) as well as terminal growth rate (column).

Analyst Consensus; Company Financials; Author’s Calculations

Investor Takeaway

I downgrade Tencent to “Hold” due to resurfacing regulatory risk in the gaming industry in China, with new regulations aiming to limit in-game rewards and spending. While only about 20% of Tencent’s topline is affected by the domestic gaming crackdown, investors should not ignore the possibility of additional, broader regulatory headwinds for the Chinese tech giant. That said, I view Tencent’s equity yield of approximately 1% as clearly not sufficient to offset the company’s broad investment risk. On updated valuation assumptions, I now calculate a fair implied share price for TCEHY equal to $32.15.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment