pixelfit

Thesis

I still believe TELUS International (NYSE:TIXT) is undervalued as of today. My original thesis still stands, which is largely based on the idea that customers place value on brands based on the quality of the experience they are provided. TELUS has superior, cutting-edge technology based on a sustainable model for building and preserving customer relationships.

The positive news from this 4Q22 results is that management has emphasized that demand from clients for outsourcing remains high, and the addition of the rapidly expanding WillowTree asset should provide synergy possibilities in 2H23. In spite of this, I believe it is becoming increasingly apparent that the near-term macro pressure will persist at least through this year. As expected, TIXT’s 4Q results and 2023 outlook show that the macro headwinds it forecasted in the previous quarter are materializing. Short-term, I anticipate that TIXT’s traditionally strong verticals will experience weakness, putting pressure on growth and ensuring that FY23 organic growth remains in the low double digits (excluding contribution from WillowTree). Moreover, the acquisition of WillowTree is likely to have an effect on the potential for margin expansion. That said, all in all, TIXT is performing admirably, and bullish commentary regarding synergies with WillowTree’s potential provides reason for optimism regarding the company’s ability to achieve upward revisions in 2H23 if the macro environment remains stable.

4Q22 results

In 4Q22, TIXT reported $630 million in revenue, which was slightly below the $634 million consensus estimate. On the other hand, TIXT adjusted EBITDA of $157 million was higher than the expected $156 million, and its adjusted EPS was also higher than expected. Growth in revenue was led by Banking, Financial Services & Insurance, with eCommerce and Fintech lagging behind. During the quarter, TIXT brought in an additional 3,890 net employees, bringing the total team count to 73,142. This increase was primarily due to the company’s efforts to support TELUS Health.

Macro weakness to continue

Quarterly revenue was slightly below expectations due to macroeconomic pressure and FX, and TIXT is still feeling the effects of difficulties with some fintech customers and general softness. Considering that management has signaled near-term weakness across the customer base, I expect the weak macro backdrop to continue weighing on growth into FY23. The forecast for organic revenue growth of 10% to 12% also reflects the anticipated weakness.

Tech & Games, in particular, saw a significant deceleration, with growth of 10% on a constant currency basis compared to 23% in 3Q; this was expected, given the very weak performance of the large social media company that accounts for a big proportion of Tech & Games sales. Sales in the eCommerce and Fintech vertical fell by 9% year over year in the fourth quarter when adjusted for FX. Although the management’s comments sound positive on these few verticals, I anticipate the macro weakness will continue to dampen the outlook.

More on WillowTree

The immediate positive about this acquisition is that it will improve FY23 revenue. On the flipside, I expect margin to be pressured due to weak pricing dynamics. Also on margin, WillowTree’s lower margin profile and associated interest expense is going to pressure FY23 EPS outlook as well. Overall, I do think the acquisition is going to be beneficial in the long run as it enhances the global GTM model that I discussed in my original thesis.

Valuation

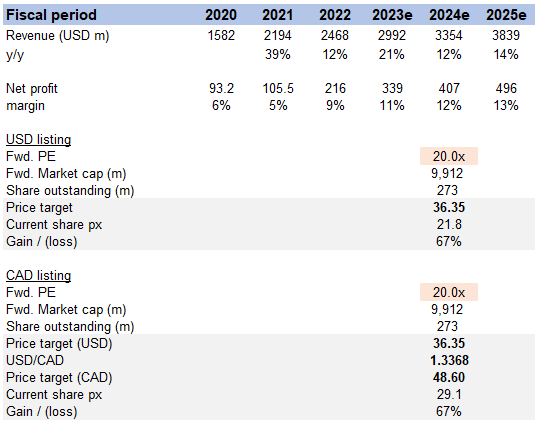

At these levels, TIXT still offers attractive upside, driven by mid-teens revenue CAGR over the medium term and improving margins, resulting in strong EPS growth. However, organic earnings growth in the near term may be pressured due to the dilutive impact of the WillowTree acquisition, which, when combined with higher interest expense, results in slightly slower FY23 EPS. Similar to my previous post, I believe TIXT will gradually trade up to 20x when it demonstrates strong earnings growth. This was demonstrated when it traded up from 15x to the current 17.4x forward earnings, which I believe is due to some investors looking beyond this year’s poor performance.

Own estimates

Conclusion

I expect the macroeconomic pressure to continue affecting growth in the near term, with organic revenue growth forecasted in the low double digits. The acquisition of WillowTree is expected to improve revenue in FY23, but also pressure margins and EPS due to its lower margin profile and associated interest expense. Despite the near-term challenges, TIXT remains undervalued, with mid-teens revenue CAGR over the medium term and improving margins driving strong EPS growth. TIXT should also gradually trade up to 20x when it demonstrates strong earnings growth.

Be the first to comment