SinArtCreative

Introduction

It looks like recent sentiment on Teladoc Health (NYSE:TDOC) among Seeking Alpha authors has turned bullish:

Seeking Alpha Author Sentiment (Seeking Alpha)

I did some research and this is my view:

Thesis Summary

I don’t see a fundamental bullish case for Teladoc due to these reasons:

- Growth is slowing down

- TDOC has low incremental margins

- Unrealistic valuation assumptions are required to justify a buy

Growth is slowing down

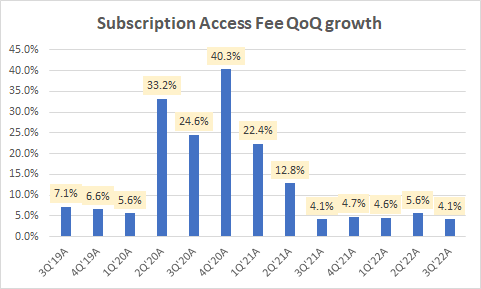

Subscription access fee growth slowdown

TDOC makes 86.1% of overall revenues from its subscription access fees. This growth has seen considerable slowdown over the past 5 quarters:

Subscription Access Fee QoQ growth (Company Filings, Author’s Analysis)

On an annual run-rate basis, growth rates are ticking at 20% YoY.

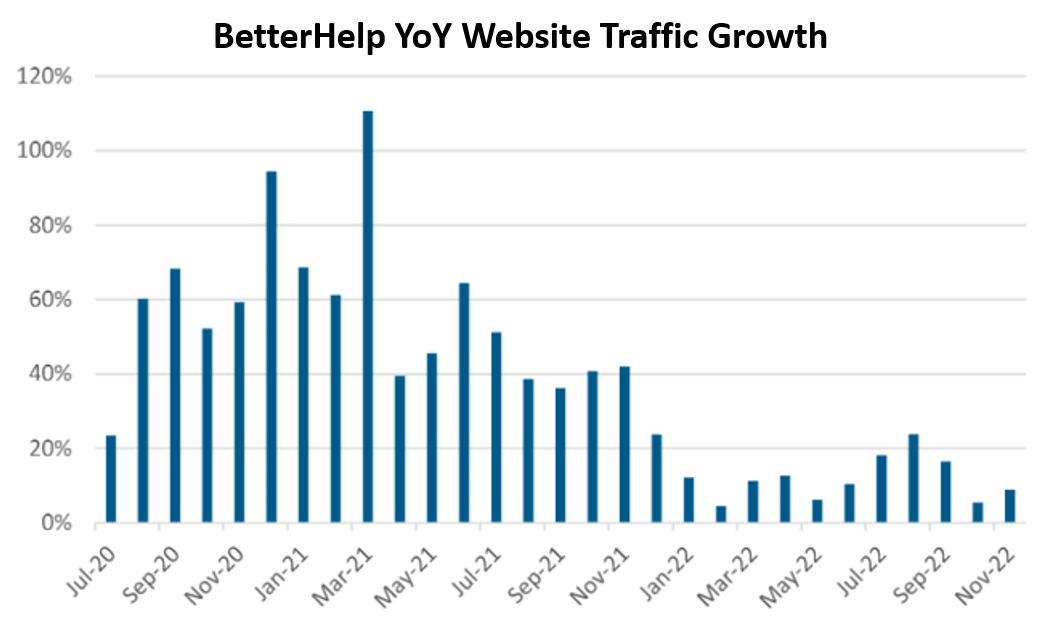

BetterHelp traffic growth slowdown

A key driver of Teladoc’s revenues is their subscription-based mental health and wellness app directed to consumers. Management also highlighted BetterHelp as being a key growth contributor in 3Q FY22’s 10-Q:

…revenue was driven substantially by the generation of additional access fees by our membership base, most significantly from our DTC mental health service, BetterHelp.

However, according to SimilarWeb, website traffic growth for BetterHelp is tepid at less than 10% YoY growth levels:

BetterHelp YoY Website Traffic Growth (SimilarWeb, Author’s Analysis)

Ultimately this casts doubt on the company’s growth execution.

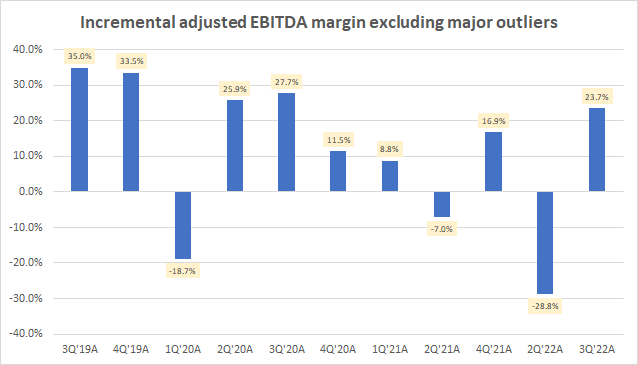

TDOC has low incremental margins

Incremental margins are important metrics to track for companies that have not yet achieved stable profitability margins. Incremental margins are indicative of long term margin profiles for a business. For TDOC, excluding some outlier years, the incremental margins can optimistically be assumed to be in the mid-20 percentage ranges:

Incremental adjusted EBITDA margins (Company Filings, Author’s Analysis)

My intuition says this is too low. But let’s prove it with the numbers:

Unrealistic valuation assumptions are required to justify a buy

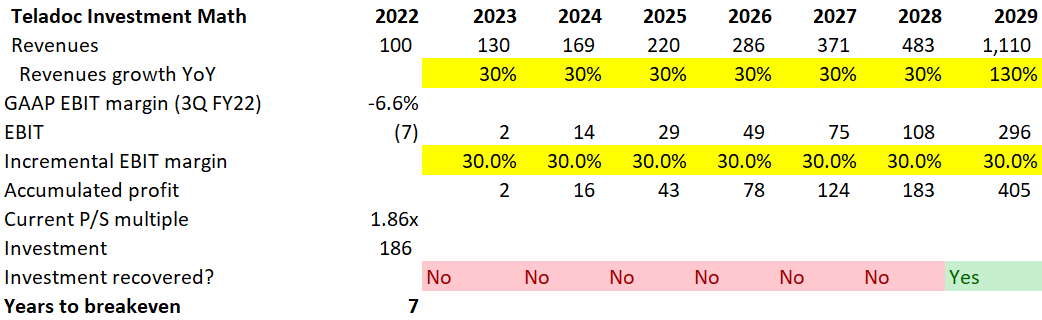

The table below shows my simple investment math for TDOC:

Teladoc; Simple Investment Math (Company Filings, Author’s Analysis)

Let’s start with a base of $100 in revenues today and very generously assume 30% YoY growth thereafter. Take the Q3 FY22 GAAP EBIT margins of -6.62% and again, give the company a great benefit of the doubt and believe they can do 30% incremental EBIT margins. Assume zero tax. The current P/S multiple is at 1.86x, which means an investment today in 1 share would cost $186 at a $100 revenue base. The resulting insight is that:

Forget about making a return; despite these highly optimistic assumptions, it would take you more than 6 years just to breakeven on your investment in Teladoc!

Therefore, I believe Teladoc is a very risky investment; it requires unrealistic assumptions to justify a buy.

How I can be wrong and why I won’t short

I can be wrong if animal spirits and irrational exuberance lift up TDOC’s stock price. However, I doubt whether this would be sustainable. Given the intense, almost cult-like fervor among many long term growth investors in search of potential multibaggers, I am hesitant to short such a popular stock due to short squeeze risks.

I can also be wrong if the company executes on these very demanding growth and incremental margin assumptions. The ball is in their court…

Takeaway

I think Teladoc’s business model is broken. It is hitting way below the mark in terms of revenue growth and margins to justify its valuation. I believe Teladoc buyers have got this one wrong.

Be the first to comment