FabrikaCr

Investment Thesis

Teck Resources (NYSE:TECK) is well positioned for the copper sector showing strength. More specifically, with China’s reopening, this will stimulate copper demand, as copper is intrinsically linked to the Chinese industrial sector.

I highlight how Teck is doubling down on its copper prospects and lay out my assumptions for 2023 free cash flow.

Furthermore, management remains consistent in its messaging that it’s going to return 30% of cash flows to shareholders on top of its 1% base dividend yield.

What’s Happening Right Now?

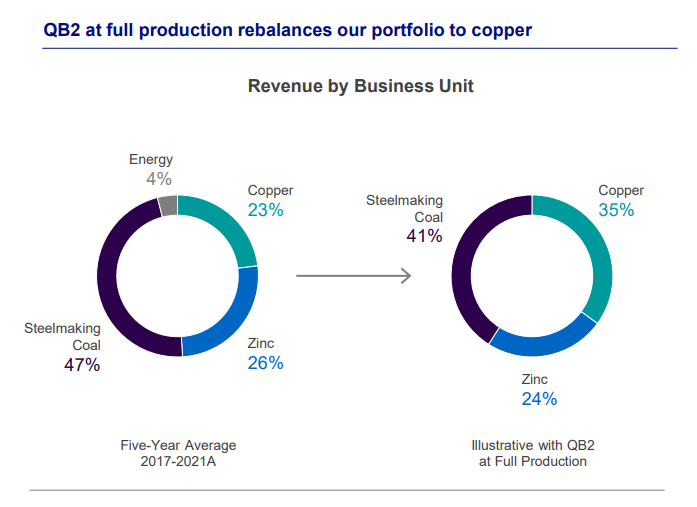

Teck’s prospects are about to change sooner, rather than later. Recall, once Teck’s QB2 project is in full production, 35% of Teck’s revenues will come from copper.

TECK Q3 2022

And with steelmaking coal being particularly healthy right now and copper starting to improve, this could translate into Teck’s 2023 prospects being substantially improved.

Put simply, Teck is going all out to increase its prospects from copper. And with that in mind, consider the graphic that follows:

Trading Economics

What you can see here is that coal prices have bounced hard from a floor in the summer. What is more, in the past several days, as China has seen countless riots in its streets, I believe that China is seriously reconsidering its lockdown policy.

Could China dramatically ramp up its Sinovac vaccination program? Yes, not as effective as Pfizer/BioNTech vaccine, but still provides around 70% protection.

And I’ll go so far as to argue that this is exactly what’s taking place right now.

The market is sniffing out a stop to lockdown, with some Chinese ETFs ripping higher in the past several days.

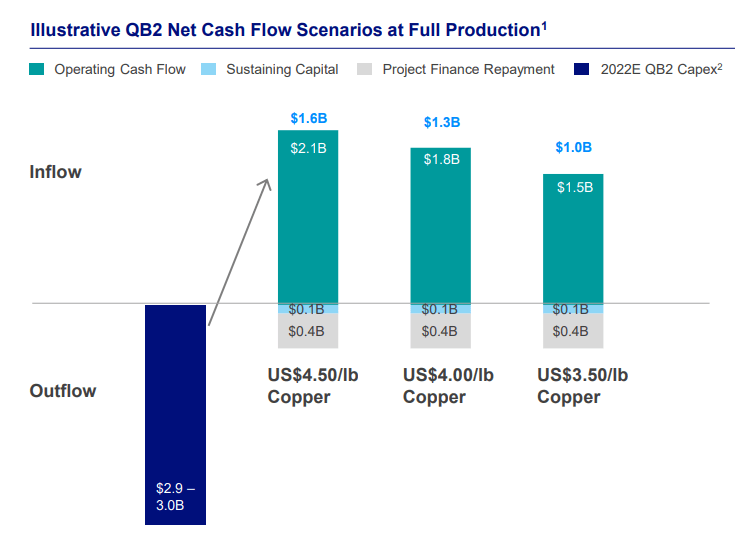

So with that in mind, given that copper prices on the spot market have already moved to $3.60 per pound, and are rapidly moving towards $4.00 per pound, I believe that in no time, Teck will be printing around CAD+$1 billion in free cash flow just from its copper business.

TECK Q3 2022

Capital Return Program

During its earnings call, when asked about Teck’s capital return program, given the sale of its energy unit to Suncor (SU), this is what was said,

[…] the first 30% of available cash flow is automatically returned to shareholders, and then we retain of course, based on consultation with our Board, the discretion to return additional amounts if we believe that’s warranted based on other uses of cash at that point in time.

Teck consistently states its ambition to return 30% of its free cash flow. By my rough estimates, that would equal around CAD$1.3 billion, or 5.2% combined return, via buybacks and dividends, on top of its 1.0% base dividend yield.

TECK Stock Valuation — 6x Free Cash Flow

Teck reported CAD$1.9 billion of EBITDA in Q3, which annualizes at CAD$7.6 billion. We don’t get a clear sense of what portion of the profits come from steelmaking coal. But I suspect that the vast majority of its bottom-line profitability will come from coal.

Hence, if steelmaking coal was to weaken, that could impact Teck’s 2023 prospects.

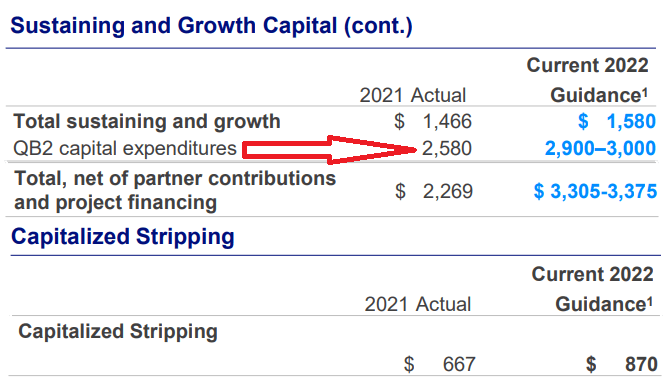

Meanwhile, we are told that capex in 2023 will be ”lower than 2022”, but not ”a reduction of $2 billion compared to 2022”. Now see below.

Teck Q3 2022

If we roughly assume that total capex in 2022 is around $4.3 billion, I believe that around $3.3 billion for 2023 seems fair.

Consequently, I believe that if we assume that copper prices do start to show strength, I believe that CAD$4 billion of free cash flow seems very reasonable.

That would put Teck at approximately 6x free cash flow.

The Bottom Line

I’ve attempted to be very conservative in my estimates. I believe that if China reopens, and sets out to support its ailing economy, this could drive strong prospects for Teck.

Simply put, I believe that whereas steelmaking coal was the biggest driver for Teck in 2022, that copper could be the game changer for Teck in 2023.

By my estimates, investors onboard Teck could get a total combined return of +6%, via buybacks and dividends.

Be the first to comment