Natali_Mis

Investment Thesis

Teck Resources (NYSE:TECK) made a significant change in the past twelve months. It spun off its energy business, which one could make the assertion was a foolish endeavor. Nevertheless, by doing so, it has now sought to increase its exposure to copper.

And whether the timing towards copper was luck or foresight, from our perspective it matters not. The fact that Teck’s end markets, in particular copper, are rapidly strengthening, leaves Teck Resources well-positioned for a strong 2023.

Near-Term Catalyst, Copper

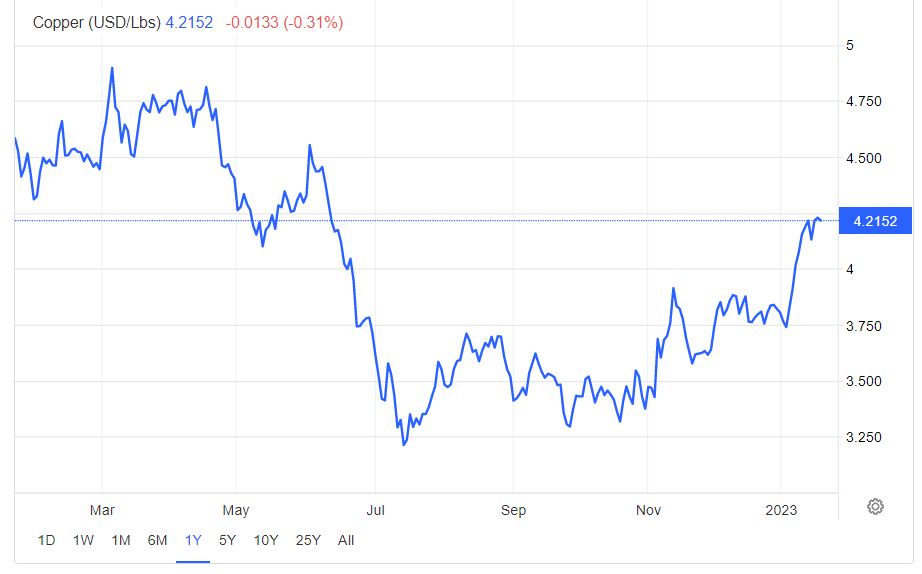

Consistent with what I stated last quarter, TECK’s business model has shifted towards doubling down on its coal opportunity. What I stated in the last article was that at some point in 2023, copper prices could reach $4.00 per pound.

Never would have imagined that copper prices were going to sizzle this strongly.

Tradingeconomics.com

In practice, this means that TECK’s copper business alone is going to print more than CAD$1.1 billion of free cash flow over the next twelve months.

Needless to say that this is provided that the tailwind that got copper prices to $4.20 per pound remains in place. Namely, China’s reopening continues to happen, as this is the biggest driver of copper demand.

But What About the Rest of Teck Resources?

To make something clear, even though my bullish insight is on the dramatic improvement in the copper market, TECK isn’t just copper.

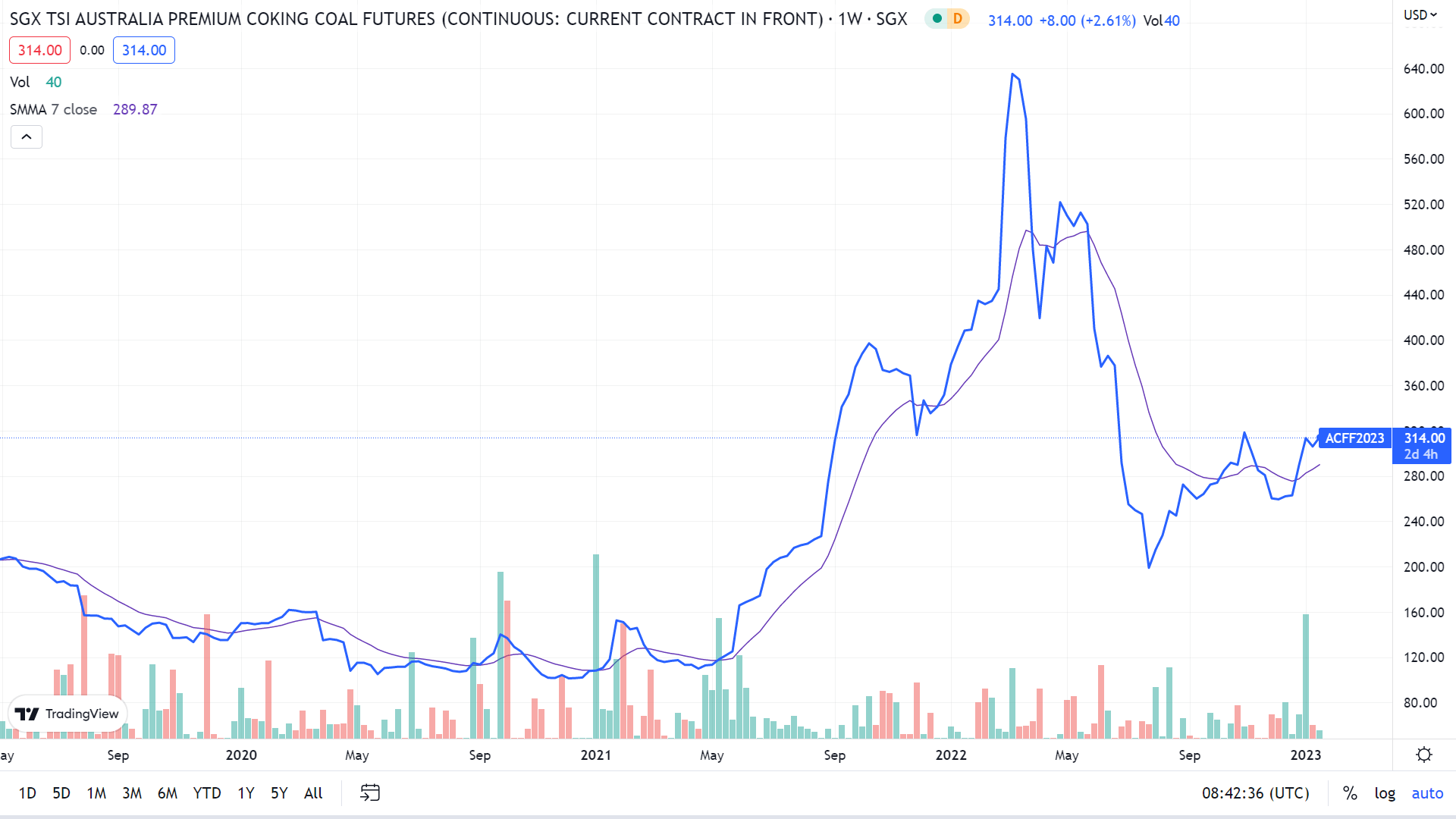

Indeed, coking coal is also a huge proportion of its business, making up approximately 40% of its business.

Furthermore, I believe that coking coal has recently stabilized and appears to also be moving higher.

TradeView, “ACF1!”, Coking Futures

Indeed, for better or worse, coking coal isn’t like thermal coal. Thermal coal saw its pricing get extended in 2022 as Europe scrambled for energy.

But now that natural gas prices have hugely sold off, this will be a significant headwind for thermal coal players.

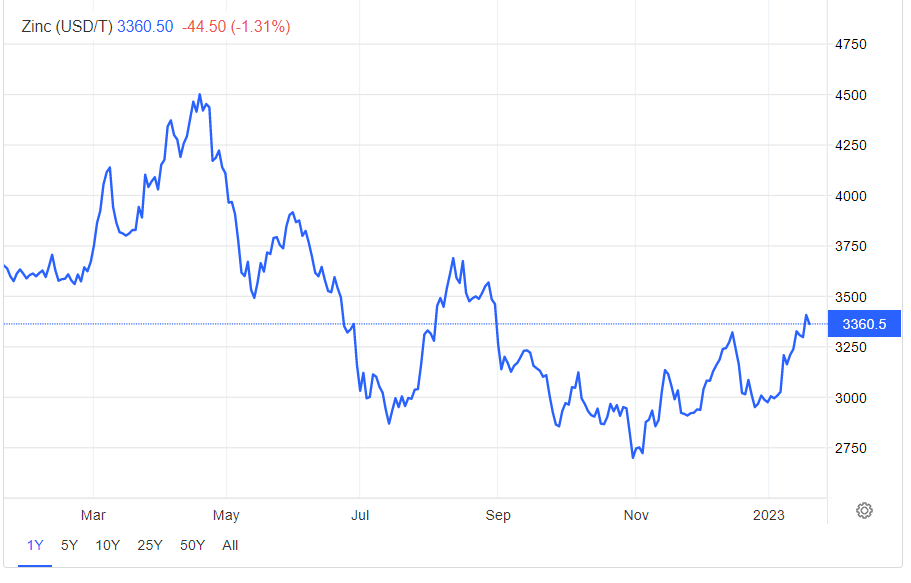

Also, making up around 20% of TECK’s business is its zinc business.

Again, similar to coking coal, zinc prices also appear to have stabilized.

Tradingeconomics.com

Hence, I believe we could summarize the situation as such. Coking coal and zinc have stabilized and will not provide a headwind for Teck.

Nonetheless, copper prices are where this story is truly at.

Before we go any further, note that there are other analysts that have a different point of view from my bullish thesis, declaring that copper prices are already factored into TECK’s valuation, something we’ll now discuss.

TECK Stock Valuation — 7x Free Cash Flow

According to my estimates, TECK’s capex in 2023 will be approximately CAD$3.3 billion. Furthermore, I estimate that in 2022 TECK could report around CAD$8 to CAD$8.5 billion of EBITDA.

Thus, it’s entirely possible that with strengthening conditions, TECK could in 2023 make at least CAD$4 billion of free cash flow.

This puts the stock priced at 7x next year’s free cash flow.

Now, keep in mind that TECK believes that if conditions permit TECK will be in a position to continue returning 30% of its free cash flow to shareholders. When asked on the call, TECK didn’t rule out a special dividend, but I personally believe that TECK will continue to favor share repurchases over dividends.

The Bottom Line

As I’ve proclaimed for several months now, the revenge of the old economy is a theme that investors would do well to note.

The winners of the last 5 years cannot be relied upon to be the winners in 2023. In a time of turbulence, raising interest rates, and overall uncertainty, investors don’t want to be invested in businesses where you have to accurately forecast the future.

Investors are likely going to be significantly better rewarded for siding with stocks that are cheaply priced and returning capital to shareholders.

With this in mind, I believe that TECK fulfills this imperative well.

Be the first to comment