nimis69

Business Diversification Props Technip Energies

Technip Energies N.V. (OTCPK:THNPY) is an engineering and technology company that deals in LNG, downstream, offshore, and sustainable energy transformation. In Q3, the company’s Project Delivery segment had a setback after it exited the Arctic LNG 2 project. Nonetheless, its legacy LNG and ethylene business remain firm with steady deliverables. Recently, the company has proactively diversified in clean hydrogen, decarbonization, and other energy transition revenue streams. Its energy transition commercial pipeline has expanded by 50% since 2021, keeping with the latest ESG trend.

However, uncertainty over the Ukraine-Russia conflict has affected natural gas and LNG prices. So, in the short term, its LNG business can see limited growth or a decline. However, I expect engineering services activity in the Middle East and the ethylene and biodegradable polymer business to make up for the loss. The company’s balance sheet is robust, with bulky liquidity. The stock is undervalued versus its peers. I expect investors to benefit from holding the stock over the medium-to-long term.

Strategies And Key Drivers

Technip Energies’ 9M 2022 Presentation

Technip Energies’ management has continued to diversify in clean energy projects. Its focus has grown beyond ethylene and now includes clean hydrogen, decarbonization, and other energy transition initiatives. Its energy transition commercial pipeline has expanded by 50% since 2021. The ethylene market is recovering after a contraction in the last three to four years due to a reduction in significant new capital projects and the recent economic uncertainties.

Some key drivers that would allow a strong turnaround in this business include the EU Packaging Directive and related economic agendas and strategic expansion of the refiners into petrochemical production. I will discuss more on other green energy projects later in the article.

Forecast And Outlook

Seeking Alpha

Technip Energies N.V.’s FY2022 guidance suggests 1.3% lower revenues than FY2021 (at the guidance mid-point). Its adjusted recurring EBIT margin can rise to 6.8% from 6.5% in the previous year. In backlog, it has EUR 4.5 billion in sales for 2023. While the topline can see revenue loss from the Arctic LNG 2 exit, cost-based management, project execution, and growth from TPS activities will add to the operating margin in FY2022.

LNG And Downstream Project Updates

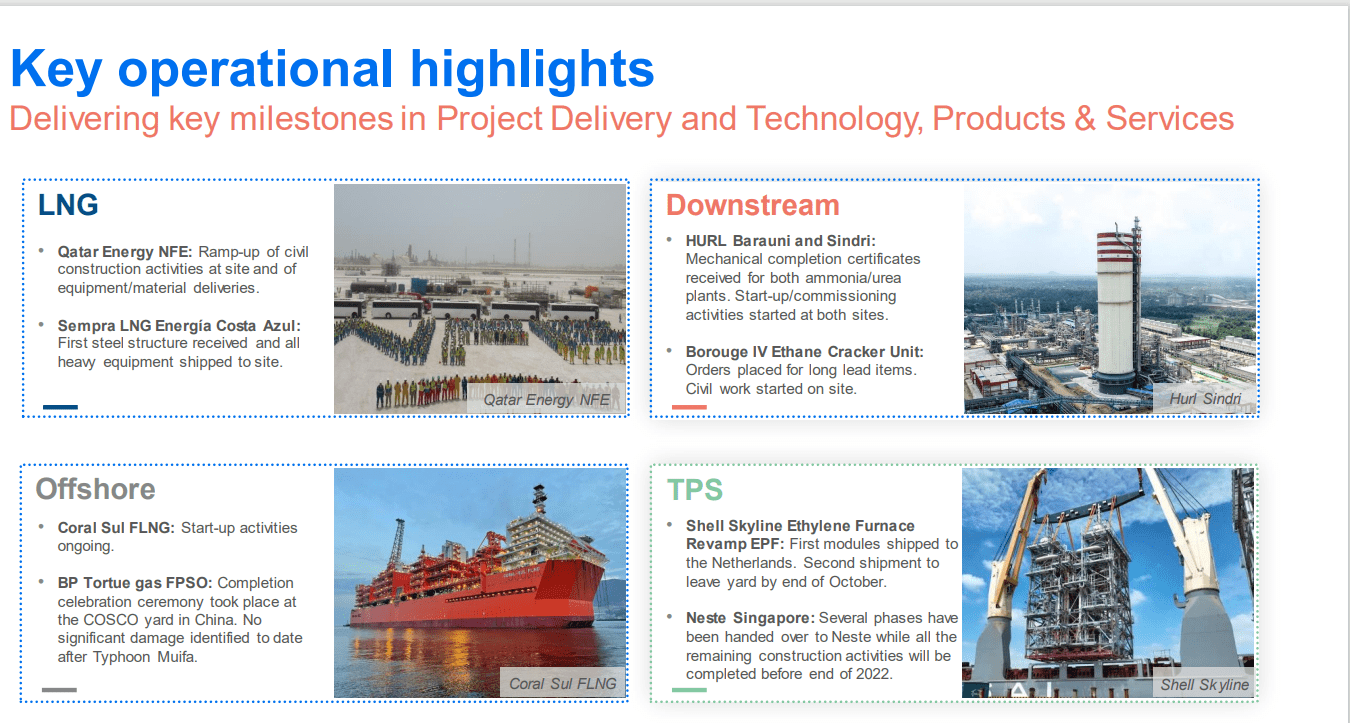

LNG, THNPY’s legacy business, saw a significant decline in contribution from Arctic LNG 2, which led to a revenue fall in its Project Delivery segment. In Q3, it signed an Exit Framework Agreement with a client. However, a couple of its projects have been robust. It has ramped up civil construction activities in the Qatar Energy NFE. Offshore, the Coral Sul FLNG start-up activities are ongoing. Downstream, it has received Mechanical completion certificates in HURL Barauni and Sindri (in India). It has also shipped its first steel structure in Shell Skyline Ethylene in the Netherlands.

LNG Price Is On A Seesaw

EIA

In 2022, U.S. LNG export price increased by ~45% until October 2022, although it was 20% lower than the previous month. According to EIA, the U.S. monthly storage inventories have remained below the five-year average. According to its estimates, due to weather-related declines, U.S. natural gas production of dry can go down by 0.5 Bcf/d from December through March. In 2022, natural gas production increased by 2% due to increased drilling activity in the Haynesville and Permian regions.

Key Clean Energy Project Update

Company Filings

Among the key projects in Q3 was Project 1 for INEOS in Belgium. By September-end, the company’s order backlog in the Project Delivery segment decreased by 20% compared to the start of the year. In the Technology, Products, and Services segment, however, it increased by 44%. Book-to-bill has trended up since mid-2022, estimates the company.

The company plans to deploy a cracker design to lower the CO2 footprint by ~50%. The design also allows for future transition into 100% hydrogen firing. In clean hydrogen markets, it obtained the first license sale for its proprietary Blue H2 to decarbonize a petrochemical plant in South Korea. It also procured a green hydrogen project in Australia.

Project Delivery Segment: Performance

Company Filings

Technip Energies’ Project Delivery segment revenue declined by 7% in Q3 2022 compared to Q3 2021 due to the Arctic LNG 2 exit. However, the adjusted recurring EBIT in this segment increased by 28% year-over-year. It ramped up major LNG and downstream projects significantly in Q3, which offset much of the topline decline and led to the operating profit rise.

Technology, Products, And Services Segment: Analyzing Recent Performance

Year-over-year, THNPY’s Technology, Products, and Services segment revenues increased by 10% in Q3 2022, due primarily to increased PMC and engineering services activity in the Middle East. Also, its revenues from ethylene and biodegradable polymer increased rapidly during the quarter. Adjusted EBIT increased by 20% during this period as the share of higher-margin process technology, and advisory services increased in the portfolio.

Cash Flows And Balance Sheet

Technip Energies’ cash flow from operations (or CFO) deteriorated by 80% in 9M 2022 compared to a year ago. Apart from a marginal revenue fall, a much higher working capital requirement led to a steep fall in CFO. So, free cash flow decreased by 84% in 9M 2022 versus a year ago. In the future, the management expects to deliver 70% free cash conversion, net of working capital. However, cash flows can face working capital and cash outflows following purchase orders and subcontracts closeouts.

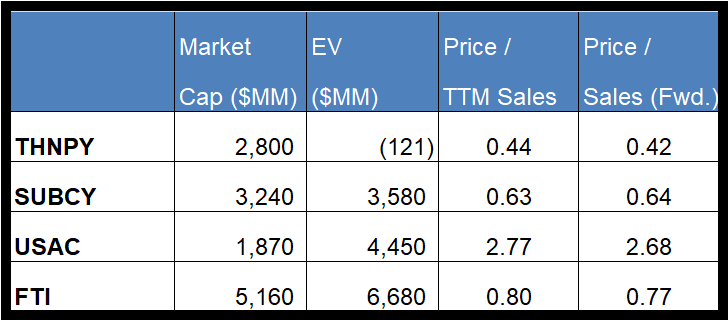

THNPY’s debt-to-equity ratio (0.46x) is lower than its peers’ (SUBCY, USAC, FTI) average of 1.8x. The majority of its debt is slated to mature in 2028. As of September 30, 2022, its liquidity (cash plus investments plus availability of borrowings under the revolving credit facility) was €4.7 billion. So, robust liquidity ensures little financial risks. Also, in 9M 2022, it repurchased €29.8 million of its shares per the share buyback program announced in March.

What Does The Relative Valuation Tell Us?

Seeking Alpha

THNPYs forward Price-to-Sales multiple contraction versus the Price/Sales is steeper than its peers because its revenue is expected to rise more sharply than its peers in the next year. This should typically result in a higher Price/Sales multiple than peers. However, the company’s P/S multiple (0.44x) is lower than its peers’ (SUBCY, USAC, and FTI) average of 1.4x. So, the stock is relatively undervalued at this level compared to its peers.

Analyst Target Price And Rating

Seeking Alpha

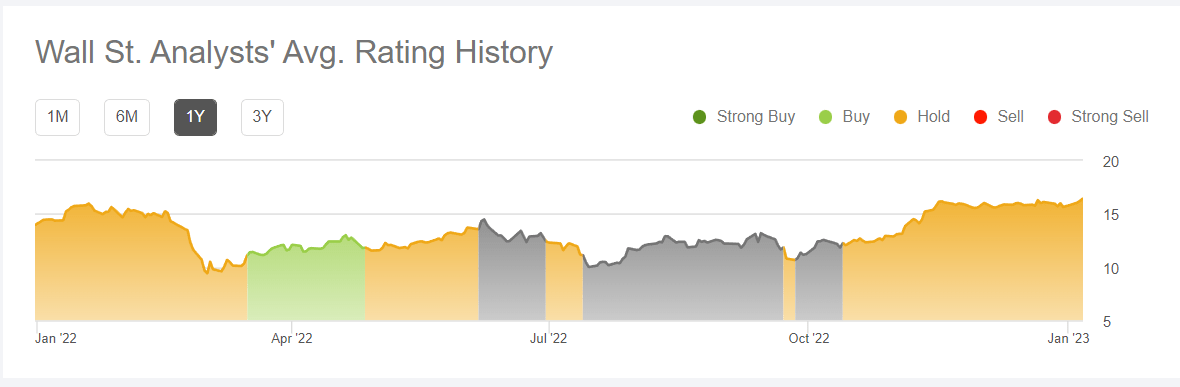

According to data provided by Seeking Alpha, only one analyst rated THNPY a “buy” in the past 90 days, while one recommended a “sell.” None of the sell-side analysts rated it a “hold.” The consensus target price is $14.1, which suggests a ~14% downside at the current price.

What’s The Take On THNPY?

In Q3, Technip Energies’ Project Delivery segment had a setback after it exited the Arctic LNG 2 project. Nonetheless, its legacy LNG and ethylene business remain firm, with steady deliverables from the Qatar Energy NFE, Coral Sul FLNG start-up, HURL Barauni and Sindri, and the Shell Skyline Ethylene in the Netherlands.

Although the natural gas price has increased over the past year, it declined sharply in October. So, in the short term, Technip Energies N.V.’s LNG business can see limited growth or a decline. However, I expect engineering services activity in the Middle East and the ethylene and biodegradable polymer business to make up for the loss. Its cash flows also dwindled in 9M 2022 as the increased activity required higher working capital deployment.

Technip Energies N.V. has no short-term debt repayment, making it nearly free from financial risks. The stock underperformed the VanEck Vectors Oil Services ETF (OIH) in the past year. Given the low valuation multiples, Technip Energies N.V. stock is apt for a “hold” in the near term.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment