Joe Raedle

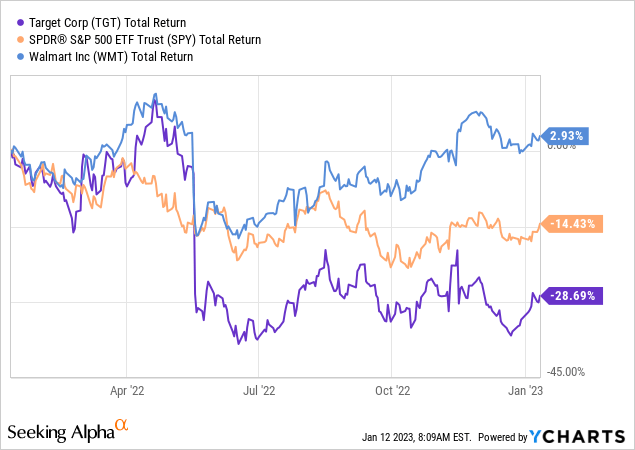

As its investors are well aware, Target (NYSE:TGT) had a miserable 2022, delivering its second-largest single-day drop ever of over 20% and falling twice as much as the S&P 500 by year’s end:

Whereas Walmart (WMT), which also suffered a double-digit drop in May 2022, has mostly recovered from it, Target shares have been rangebound between $140-160 since then and now sit at a possible breakout level around of $159.

In this article I’ll take a closer look at Target’s outlook, dividend strength, and valuation to see if it’s worth betting on as the market grapples with increasing signs of a recession offset by easing inflation and confounded by a Fed that remains hawkish on interest rates.

TGT: Rapid Margin Compression With Some Bright Spots

With its $73B market cap, 450,000 employees, almost 2,000 stores, and $107B in annual sales, Target is the seventh-largest retailer in the USA and a much-loved brand providing everything from school supplies to home furnishings to personal care products to groceries. It was a top retail winner during the COVID pandemic, but consumer discretionary retail can have boom-and-bust business cycles, and in Target’s case, the pandemic rapidly compressed these cycles into a three-year period, as its income statement shows clearly:

TGT Revenue History (Seeking Alpha)

As we can see above, Target’s annual sales remained relatively stagnant between $70-75B from 2013-2020, at which point pandemic lockdowns and government stimulus propelled sales to over $100B within two years. This period left retailers scrambling to keep inventory high while adjusting to new shopping trends. But once vaccines allowed life and consumer habits to return to normal, Target and its competitors were left with a glut of inventory that they needed to move quickly with aggressive discounting and offloading. This process has been more difficult than expected for Target, with rapid inflation and the ensuing Fed rate hikes leading to a rise in product, shipping, and financing costs, pressuring margins, and dampening consumer spending leading up to the holiday season in 2022 and continuing into 2023.

Target

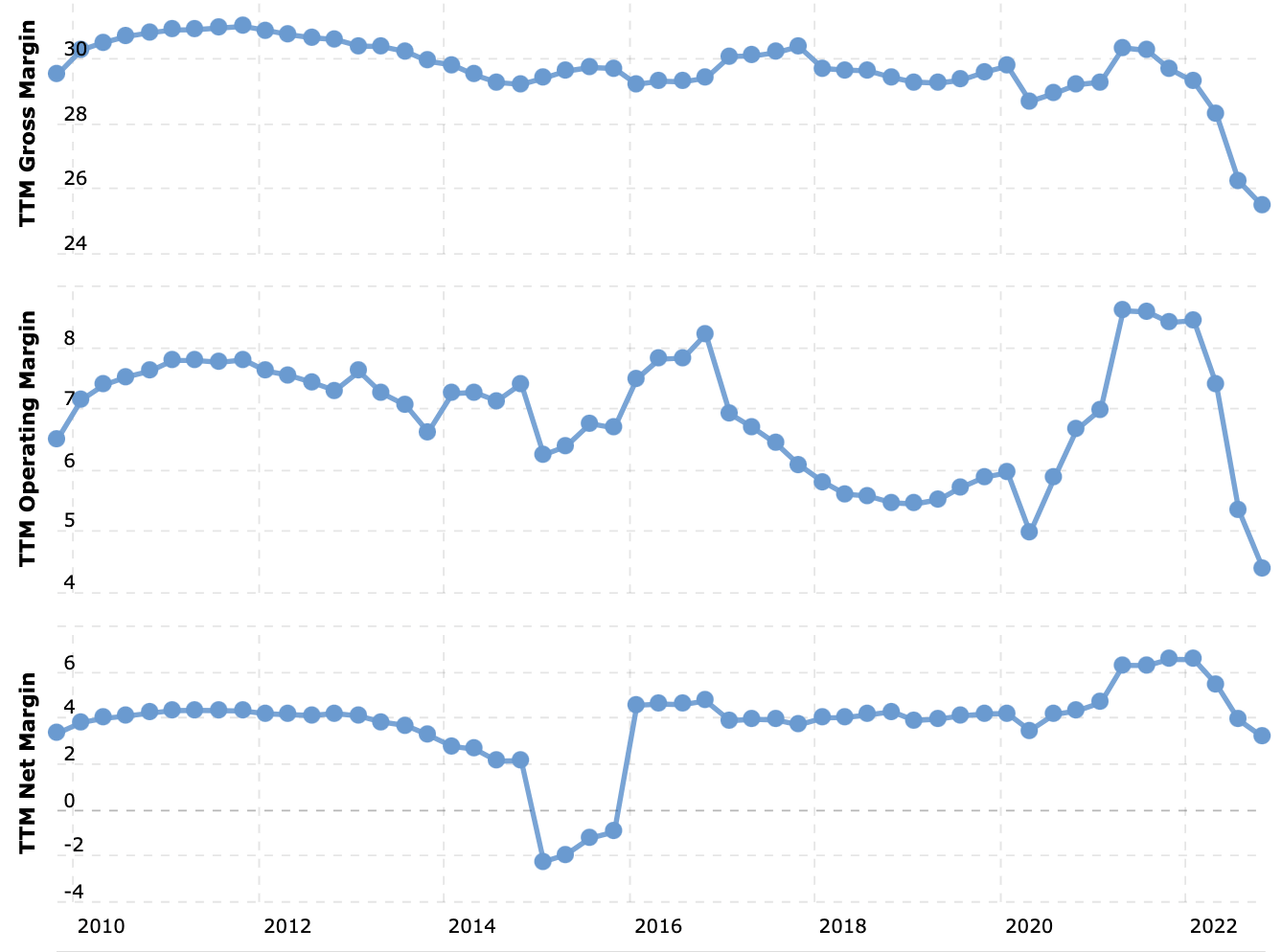

Its most recent Q3 2022 report shows that since its post-COVID revenue boom, in-store growth has slowed to ~3% and online sales have stagnated. As growth is measured year-over-year and the comps in 2020 and 2021 were quite high, I don’t think TGT’s low current growth rate is a problem in itself. The more concerning issue is margin compression, which shows how rapidly the company’s financial strength has deteriorated:

TGT Historical Margins (macrotrends.com)

While TGT’s operating margin has been quite volatile over the years, it is now at its lowest level in over a decade, and the rapid decline in TGT’s gross margin is likely unprecedented. This is a 100+ year-old company with solid management, so I don’t foresee this as an existential problem, but it certainly gives me pause as to whether I’d want to jump in as an investor until margins show signs of improving.

I don’t usually put too much stock in analyst coverage, but in this case I think Edward Kelly from Wells Fargo sums up TGT’s bear case up nicely:

TGT’s outlook has deteriorated meaningfully and we no longer see it as an attractive investment into an uncertain 2023. Our concerns include the potential for a sustained period of comp weakness in general merchandise, an inflection to negative traffic in Q4, a lack of visibility on the timing/magnitude of the margin recovery story, and the return of pre-COVID model scalability concerns.

While the outlook is indeed quite negative and there’s no sugarcoating it, one thing that Target’s management has excelled it is forming in-store partnerships with leading consumer brands. In addition to its ubiquitous Target-run Starbucks (SBUX) counters, TGT now boasts over 200 in-store Disney (DIS) shops and 300 in-store Ulta Beauty (ULTA) locations to help drive customer traffic.

In addition, the company is following the fat-cutting trend and recently announced an initiative to reduce costs across its operations, projecting a modest $2-3B in savings over the next 3 years. Its innovative partnerships and cost-cutting focus gives me some confidence that higher growth can and will eventually return.

Dividend Strength

For DGI investors, the main investment thesis for Target has traditionally been that the company offers an above-average yield plus the strongest dividend growth record in its sector along with a history of steady earnings growth to sustain it. Similar to Lowe’s (LOW) in the home improvement sector, Target is one of fewer than 50 Dividend Kings, an elite group of companies that have raised their dividends each year for at least 50 years.

Its current yield of 2.72% remains above average for the retail sector, and sits at the higher end of Target’s 20-year historical average as well.

TGT Historical Yield (macrotrends.com)

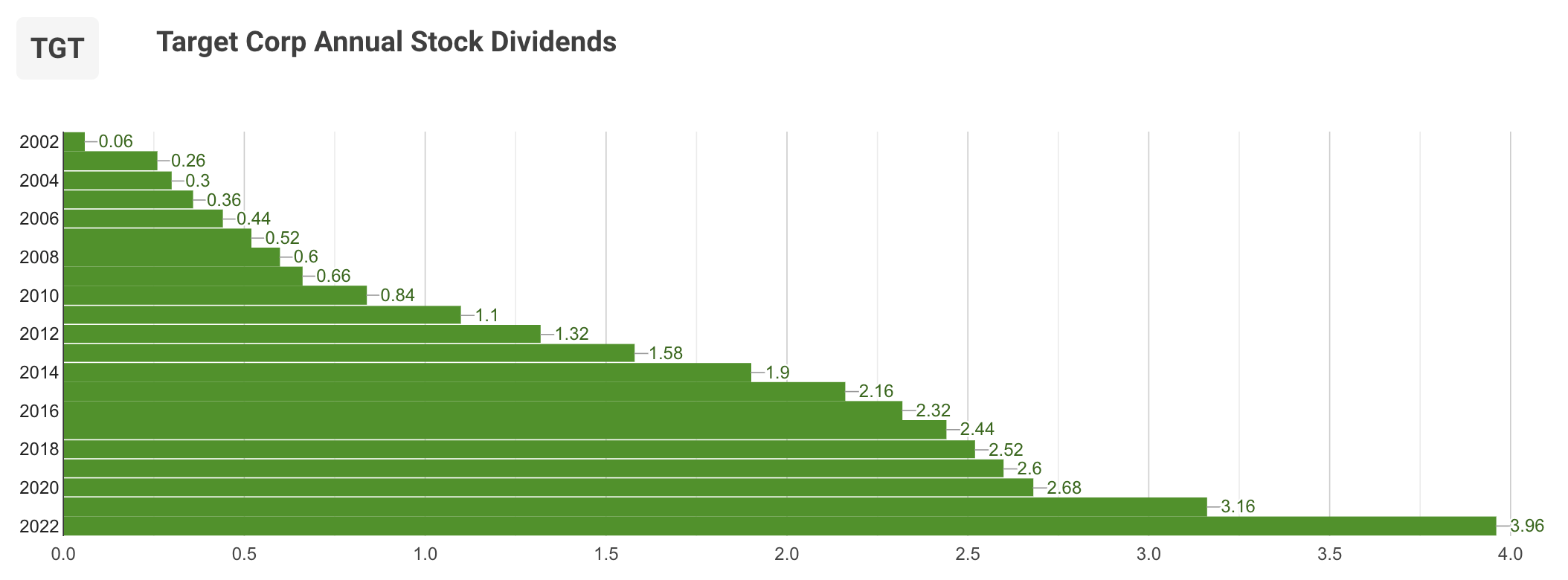

Looking at a visualization of its payout over the past 20 years, we can see that although its streak remains unbroken, Target has had periods of both high and low dividend growth, with the last two hikes of 20% in 2022 and 32% in 2021 clearly exceeding its historical average dividend CAGR:

dividendinvestor.com

In hindsight, I think it’s clear that the company was emboldened by its strong pandemic performance and may have gotten ahead of itself, raising the dividend too much too quickly without accounting for the possibility that its COVID-era performance was a blip with a short shelf life. These rapid dividend hikes combined with 2022’s margin compression have pushed its payout ratio to 54%, its highest level in the past 10 years.

TGT EPS History 2013-Present (Seeking Alpha)

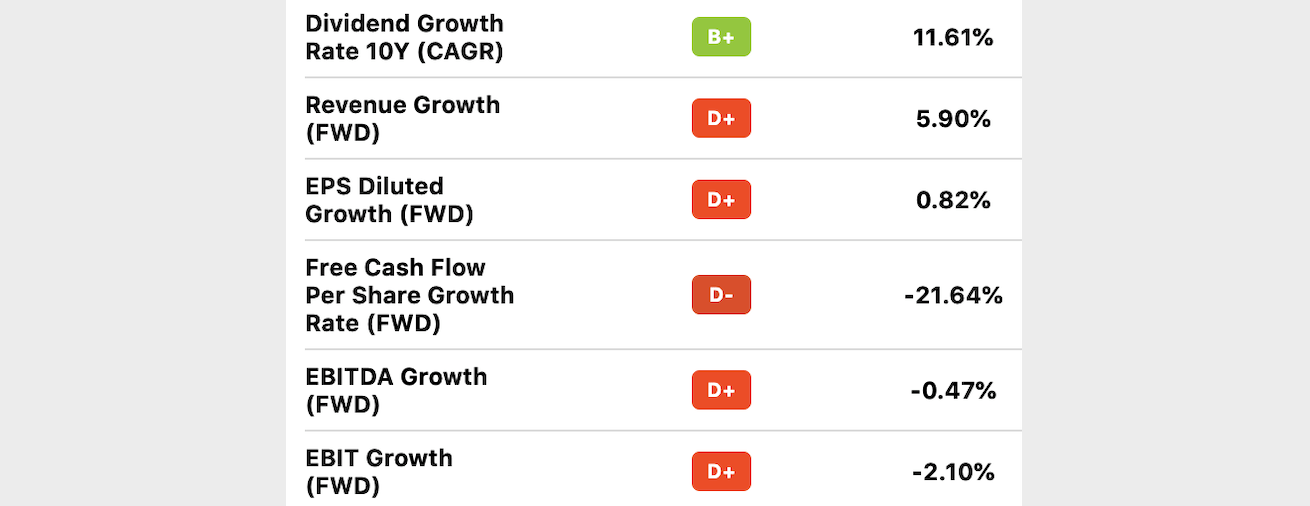

Currently running on negative free cash flow and lower-than-average revenue and EPS growth projected to grow around 2-3% YoY, it’s likely that TGT will be entering another phase of low dividend growth, which if the past is any guide will likely entail ~3% raises until growth normalizes and free cash flow turns positive. The company is no stranger to periods of negative FCF, and it is unlikely to cut its dividend and break its 51-year growth streak, but the original investment thesis I mentioned has certainly come into question.

TGT Dividend Strength (Seeking Alpha)

Valuation

While TGT appears undervalued on price to sales and forward earnings multiples, it looks quite overvalued on its trailing PE ratio of 21.7x versus its 5-year average of 17.6x as well as its cash flow and PB ratios. This isn’t surprising given its large decline in free cash flow in 2022. Furthermore, despite its relatively low forward PE ratio, its earnings growth ratio suggests that its current price is quite expensive relative to its slower-than-average growth rate.

TGT Valuation (Morningstar)

In situations with conflicting metrics like this, I tend to trust the PEG ratio as earnings growth is a company’s primary source of dividend growth and long-term safety. My conclusion is that although TGT shares are still nearly 40% below their all-time high, they still do not fully reflect the company’s compressed margins and slow growth outlook, and therefore are overvalued.

Conclusion

I do like Target as a shopper and don’t think that it deserves the no-moat rating that Morningstar assigns to it. It has stood the test of time, and some of its departments were all but essential in my household in different pivotal life stages, whether it be going to college, moving into a new apartment, buying your first house, starting a family, or the kids starting school.

Considering its entrenched place in the retail landscape for American consumers and its 51 years of dividend growth, I can’t bring myself to issue a sell rating for TGT at these levels. I do think the company’s cash flow will eventually recover and revenue growth will return to higher levels, but I don’t think this recovery will be swift, and I don’t think shares offer attractive value at their current levels.

As such, I rate TGT a hold based on its present overvaluation relative to its weak growth outlook, negative free cash flow, and historically low margins and dividend strength.

Be the first to comment