Spencer Platt

Investment Thesis

Take-Two Interactive (NASDAQ:TTWO) has been facing a very difficult year and has been penalized in consequence, as proven by the stock performance over the year 2022 (-41% vs -33% for the Nasdaq 100). The rise in interest rates, market concerns about the Zynga M&A deal, hacks – nothing spared the group. However, I expect the firm to benefit from its upcoming strong pipeline while capitalizing on its key license: GTA with GTA VI, which is in my view soon to come. In my view, the firm will be able to fuse perfectly with Zynga to deliver a unique and broad value proposition on the mobile game segment. Despite short-term concerns this deal will allow synergies and improve profitability. I initiate coverage on TTWO with a Buy rating and a target price of $138.

Company presentation

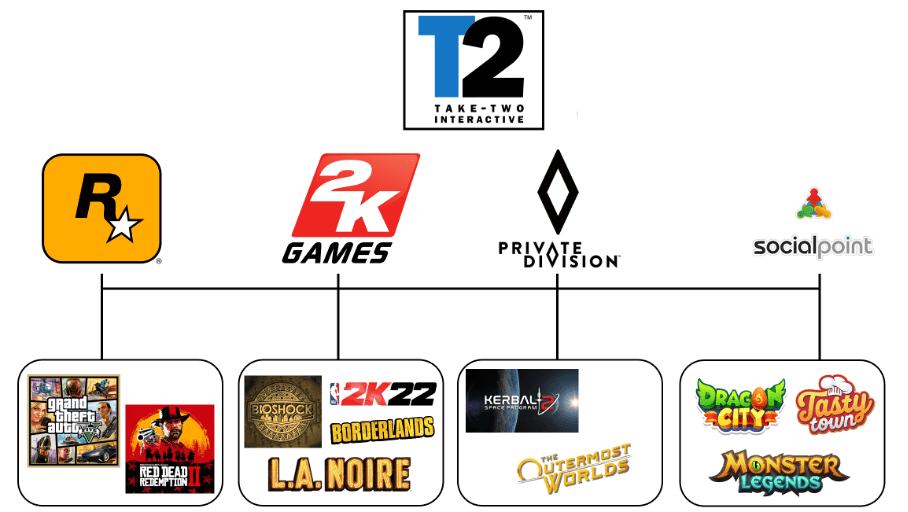

Created in 1993, Take-Two Interactive is a leading video game Company developing, and publishing video games for consumers around the world. The company offers its products under the Rockstar Games, 2K, Private Division, and Social Point labels. The firm is mainly known for its Grand Theft Auto (GTA) and Read Dead Redemption (RDR) license, both developed by Rockstar Games with GTA V being the 2nd most sold game in the world (170 million units sold) and RDR II being the 8th most sold game (40 million of unit sold). Note that the GTA Franchise represents approximately 375 million units sold worldwide. In terms of operation, the firm sells its products under dematerialized and materialized formats. Its main clients are Sony, Microsoft, and Apple which account for approximately 70% of the firm revenues. Geographically speaking, 60% of the firm’s revenues come from the US, 30% comes from Europe 5% comes from Canada and Latam, while the 5 remaining % comes from Asia.

TTWO most famous games and studios (Take-Two Interactive)

The current gaming pipeline remains resilient

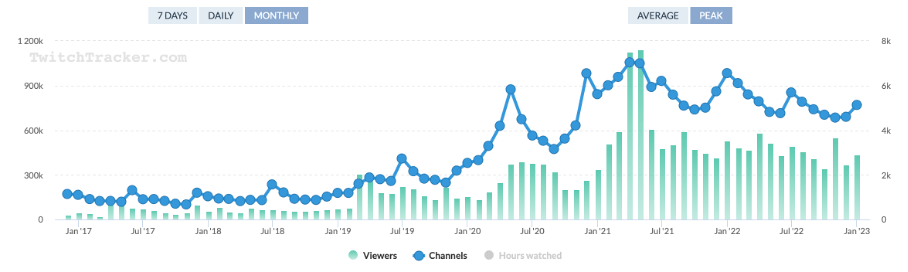

Take-Two Interactive is known for highly qualitative and immersive games and has one of the strongest reputations within the industry. The firm is capitalizing on its key licenses which surprisingly continue to deliver strong performances. Indeed, last quarter, Grand Theft Auto V sales exceeded once again expectations as new DLC and content continue to come out, the last ones being ‘Criminal enterprises’ and ‘Los Santos Drug Wars’. To have an insight into the popularity of a game, it is interesting to have a look at how many viewers on streaming platforms such as Twitch are interested in watching some gameplay of it. Here again, GTA V is still attracting a lot of viewers with an average of 160k viewers per day for the whole year 2022 making it the #3rd most watched game on Twitch.

Twitchtracker

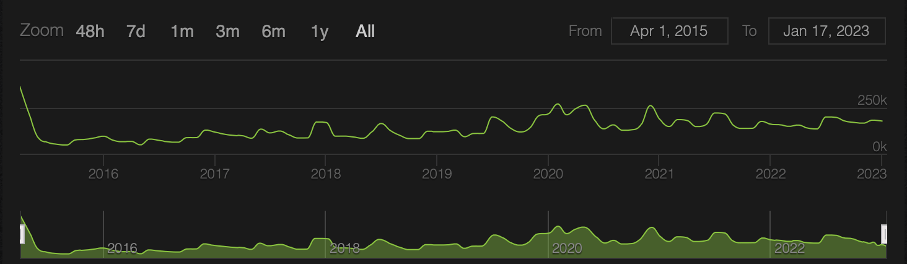

To show that this engagement is resilient, we can also have a look at the trends of GTA V players on steam. Steam is the video game digital distribution service and storefront created by Valve. It is only focused on PC games. Even if steam only accounts for a small portion of GTA V players, it tells us that the trend remains resilient.

Steam Charts

On September 9th, NBA 2K23 has been released and has been a huge success with nearly five million units sold. The game also saw significant growth in virtual currency sales and a higher average selling price compared to NBA 2K22. The engagement of the players has been remarkable, with more than two million daily active users and an impressive 4% growth in average days played. This success is expected to continue as the game becomes a year-round experience. Furthermore, the NBA 2K22 Arcade Edition remains the number one game on Apple Arcade, and a new 2K23 Arcade title has been recently released. According to venture beat, In China, NBA 2K Online continues to be the top PC online sports game in the country, with an amazing 59 million of players.

Supply chain issues are easing on the PS5 segment

Major supply chain issues on chips segments had important impacts on the possibility to see new inflows of players from the PlayStation 5. However, according to Sony Interactive Entertainment CEO, Jim Ryan: The PS5 Shortage is close to an end.

At the Consumer Electronics Show (CES) that took place in early January in Las Vegas, he stated according to FORBES:

Everyone who wants a PS5 should have a much easier time finding one at retailers globally, starting from this point forward

Good news when we know that the majority of GTA V Rockstar / 2K games are PlayStation players.

According to Polygon this time, he also confirmed the strong demand for the PlayStation 5 and said:

PS5 supply improved toward the end of last year, and I’m happy to share that December was the biggest month ever for PS5 console sales and that we have now sold more than 30 million units to consumers worldwide

I expect the easing of the supply chain constraints on the chip segment to benefit to Take-Two as it will generate new inflows of potential customers who don’t have some of TTWO games yet or simply want to buy it twice in order to have it on their next generation console. Note that at the same time of commercialization, the PS4 had 5 million more of units sold, as the supply conditions ease, this gap should be closed bringing new potential clients for TTWO.

Strong pipeline incoming: GTA VI as a “game” changer?

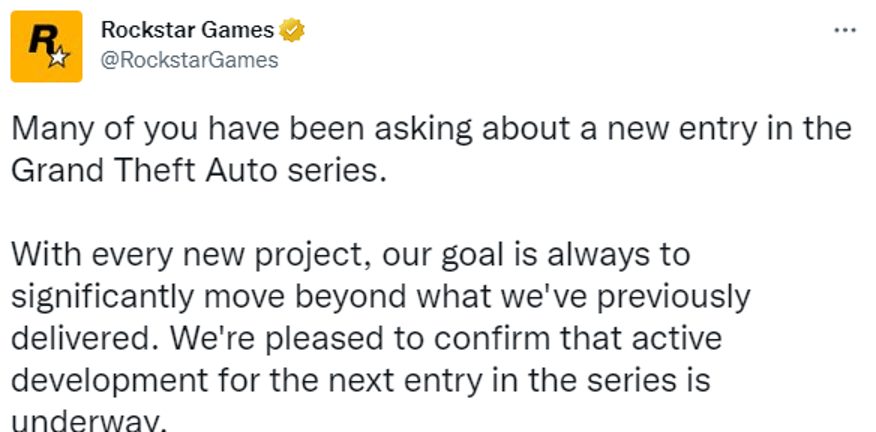

Grand Theft Auto is one of the most popular and critically acclaimed video game franchises of all time and a key resource for Take-Two Interactive. However, people are eagerly awaiting the release of GTA VI in a sense of anticipation that has been building up over many years since the release of GTA V in 2013. Long anticipation implies important expectations and thus, TTWO and Rockstar games are waited around the corner.

The combination of the franchise’s popularity, the sense of anticipation that has been building for several years, and the developer’s reputation are why many people are eagerly awaiting the release of GTA VI. However when looking at this Tweet published by Rockstar Games, the studio seems to be aware of the huge fan’s expectations.

Twitter

In this context, I expect Rockstar Game and TTWO to deliver once again. The studio rarely disappointed and has produced at 5-year intervals, two games that are in the world’s Top 10 in terms of Units sold.

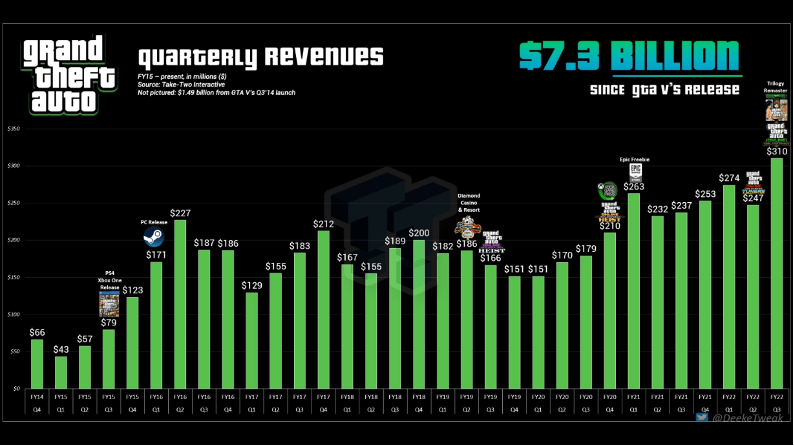

Due to this fan’s high anticipation, I expect the game to do at the minimum as good as GTA V did in terms of revenues, which could represent approximatively $8billions in revenues smoothed over the upcoming 9-10 years.

@deekeTweak on Twitter

Referring to TTWO Investor presentation:

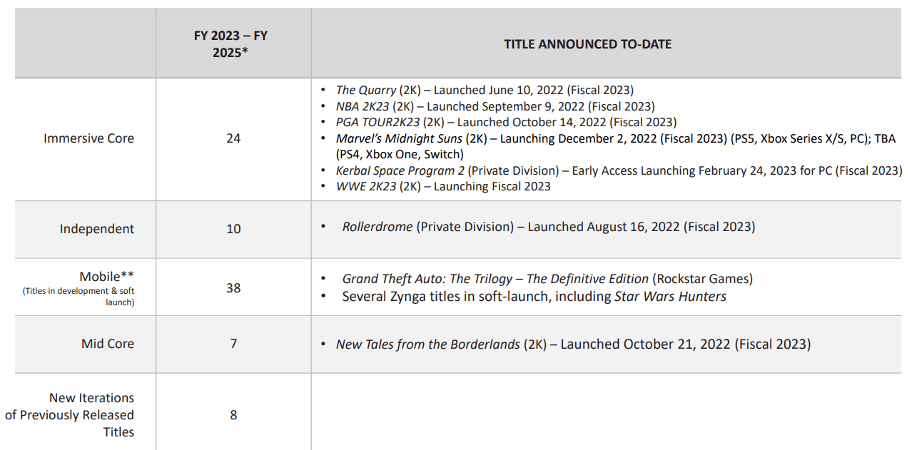

The firm plans to launch 87 products including 24 Immersive core games (Titles that have the deepest gameplay and the most hours of content.), 10 Independent games (Externally developed Private Division releases), 38 mobile games, 7 Mid core games (Titles that are either an arcade title or games that have many hours of gameplay but not to the same extent as an immersive core title.), 8 ports and remastered titles.

With such an agenda, TTWO will have a lot of challenges, but I believe that the firms and its development studios will face them with success and respect the vast majority of its deadlines and clients’ expectations.

Take-Two Interactive

Zynga M&A Deal : Short Term concerns are understandable

On the 23rd May 2022, TTWO completed the acquisition of the mobile game giant Zynga for an amount of $12.7B.

According to TechCrunch

Under the terms of the merger agreement, Zynga shareholders received $3.50 in cash and 0.0406 shares of Take-Two common stock per share of Zynga common stock.

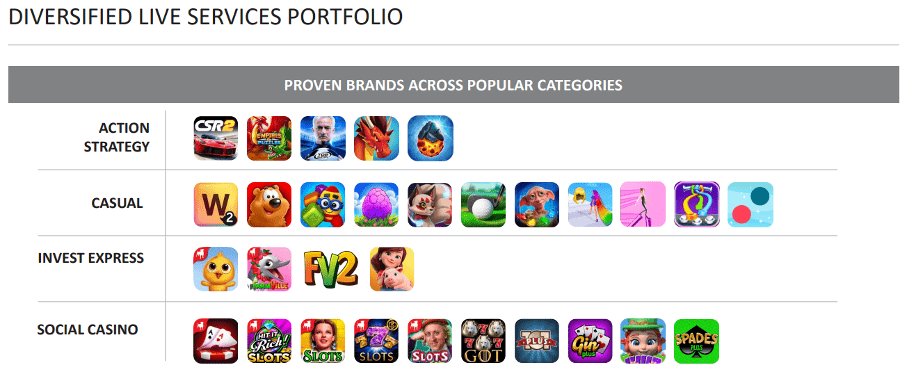

Through this deal, TTWO wants to play a major role in the Mobile Game segment. Indeed, through it, TTWO will be in a good position to become a top tier mobile game publisher, with a diverse portfolio and a strong player base with a presence in more than 175 countries.

Take-Two Interactive

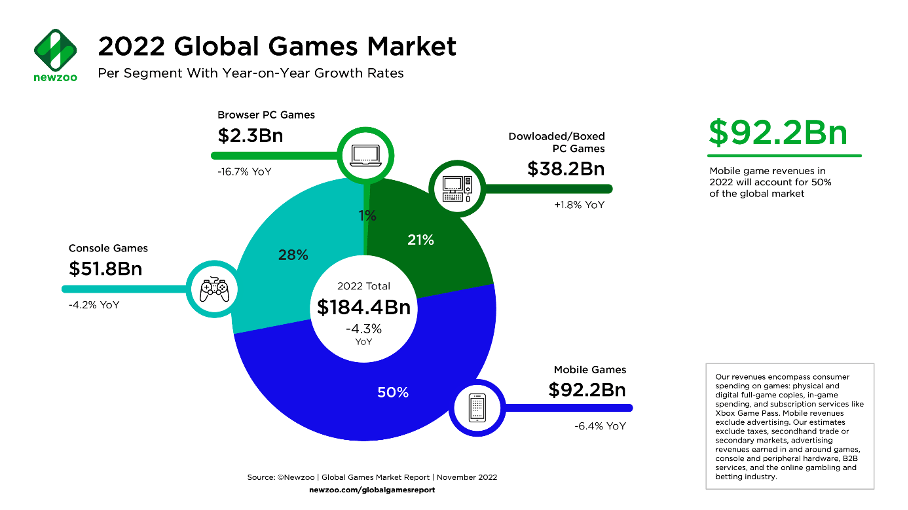

Mobile game revenues declined for the first time in history in 2022. According to Mat Piscatella, NPD game director:

Some of the drivers of the decline include the return of experiential spending, higher prices in everyday spending categories such as food and fuel, the uncertain supply of video game console hardware and certain accessories such as gamepads, and a lighter release slate of games, among others.

However, despite short-term headwinds on the mobile gaming segment (-6.4% Growth YoY) justified by a Tough macroeconomic context, I expect this transaction to be very beneficial for TTWO on the Long-Term Horizon. Indeed, I expect the firm to capitalize on its strong and diverse mobile gaming portfolio while unlocking significant revenue opportunities and cost synergies that have the potential to meaningfully enhance Take-Two’s profitability.

Newzoo

Financials and Valuation

Created by author using data from Bloomberg

In terms of financial position, TTWO does have a short-term liquidity position that is a bit weaker than its peer average with a current ratio of 1.84 vs 3.77. However, a current ratio greater than one is still suitable so nothing to worry about here. In terms of debt relative to assets or Equity, TTWO is in the best position with a Debt/Assets of 3.82 vs 11.66 for the Peer average while it stands at 6.57 in terms of debt/Equity vs an average of 18.52.

Despite the fact that TTWO has lower margins than its peers, which is largely justified by higher development costs, what clearly should attract your attention is the undervaluation of TTWO in terms of P/Sales and EV/Sales relative to its peers. Indeed, in terms of Price / Sales, TTWO is trading at a 92% discount compared to the peer median and trading at a 25% discount when looking at the EV/Sales Median.

Such a discount is not justified. In my view it is mainly explainable by the market pessimism about Zynga Deal, underpricing of the incoming pipeline and GTA VI potential, macro-economic concerns, higher interest rates. To me, the stock has been over-penalized. Furthermore, despite a Top to Bottom profitability that is under the peer’s average, it remains still suitable in my view as the firm is known for spending more than its competitors whether in time or money in the development of its qualitative games. I expect the firm to improve its profitability in the short and medium term, benefiting from cost synergies in the Zynga Deal, a strong incoming pipeline led by a GTA VI that will create unanimity.

In my view, the firm should come back at least to its average 5Y multiple, that is 5.20 for the P/Sales and 4.90 for the EV/Sales implying a 30% upside and a Target Price of $ 140.

Risks

TTWO is facing important endogenous and exogenous risks. They are both composed of several elements that are important to consider.

Endogenously, we should mainly consider the risk of a poor synergy with Zynga and delays/disappointment linked to video games release (GTA VI being the most awaited one).

Exogenously, there is still a risk for the Fed to keep its interest rates higher and for a longer period which would put pressure on valuation. The Forex risk also has to consider, as 35% of TTWO revenues come outside the U.S.

Endogenous risks mentioned above might affect way more the price action more than the exogenous ones that are in my view priced in.

Conclusion

TTWO has been strongly penalized last year with a drawdown of -48% since its ATH on the 2nd of February 2021. This performance is in my view not representative of the firm LT potential that will be driven by major catalysts that are soon to come. The strong firm current pipeline and its track record showing an ability to deliver top tier content will in my view allow the firm to perform well in 2022. I expect a 30% upside for 2023 and initiate on TTWO with a Buy rating with a target price of $138.

Be the first to comment