Annabelle Chih

Thesis

TSMC (NYSE:TSM) stock has recovered more than 30% since our post-earnings update urging investors to go on board and ignore the pessimism then. As such, it has significantly outperformed the S&P 500 (SPX) (SP500).

We believe buyers also joined the bandwagon as Warren Buffett (BRK.A) (BRK.B) unveiled his stake in the leading Taiwanese pure-play foundry. As such, semi-investors could have been emboldened to join the rush, not wanting to miss out on a solid opportunity.

TSMC has also upped the ante against Intel (INTC) and Samsung (OTCPK:SSNLF) as it unveiled grand ambitions in Arizona to maintain its foundry leadership against arch-rivals.

Accordingly, TSMC unveiled plans to increase its CapEx spending in Arizona from $12B to $40B, a massive increase, partaking in President Biden’s strategy to restore America’s long-lost foundry leadership, and reestablish its claim in the semi value chain.

However, such a tremendous move is not without significant risks, even though TSMC could have been “pressured” by the US and its most important customer: Apple (AAPL), to reshore semiconductor manufacturing in Arizona. TSMC founder Morris Chang has consistently highlighted the tremendous challenges in achieving total cost of ownership (TCO) advantages in US foundry manufacturing.

Intel was also not keen on having a “foreign” partner benefiting from the CHIPS Act, which could impact its IDM 2.0 roadmap for Intel Foundry Services (IFS) to retake foundry leadership after its reshuffled Internal Foundry Model.

Samsung has likely sensed increased competitive pressure, as the Korean media highlighted that Samsung is keen to thwart TSMC’s leadership by 2024 with a “dual track” approach, leveraging its enhanced 3nm GAP process to win back lost customers.

Hence, it has been an exciting and pivotal month for America’s foundry leadership ambitions and also for TSMC. However, while we believe the support from the Biden Administration should be constructive, we are also concerned with the cost curves of Arizona’s significant capacity upgrade. Hence, we urge investors to parse management’s commentary at its upcoming Q4 card on its CapEx guidance moving ahead.

Notwithstanding, we gleaned that the near-term optimism in TSMC’s recovery in 2023 has likely been reflected. With consumer electronics likely still in a digestion phase, we don’t expect the growth cadence that we experienced back in 2020/21 to materialize in the near term.

Wall Street’s consensus also suggests a more “normalized’ growth momentum is likely in play over the next couple of years. As such, we urge investors to be wary about chasing TSM’s upward momentum after the recent sharp surge and wait patiently for a pullback first.

Revising from Buy to Hold for now.

TSMC: Massive CapEx Upgrade In Arizona

Nikkei Asia reported earlier today that TSMC upgraded its CapEx spend projections in Arizona from $12B to $40B, with the aim of producing 60K wafers monthly (up from an initial target of 20K wafers).

Moreover, TSMC will also manufacture its 3nm process in Arizona, lending further credibility to the Biden Administration’s semi technological reshoring ambitions.

Notably, TSMC’s newly announced upgrades followed closely after a recent report indicating Apple wanted TSMC to focus more on its leading-edge production in Arizona. With Apple suffering the consequences of its China-heavy production strategy, the Cupertino company is likely pulling all levers to diversify its production risks further.

However, what does that mean for TSMC’s CapEx roadmap? We think it could be massive, depending on how much funding it will receive from the Biden administration for the upgrade.

TSMC founder Morris Chang highlighted in a November conference that the manufacturing costs in Arizona are “at least 50% higher” than its operations in Taiwan. However, he also stressed that “this will not stop the company from shifting more capacity to the US as the strategy is important and necessary for the country.”

But, TSMC investors should be concerned, as it should shift its CapEx costs curves significantly with such a massive upgrade.

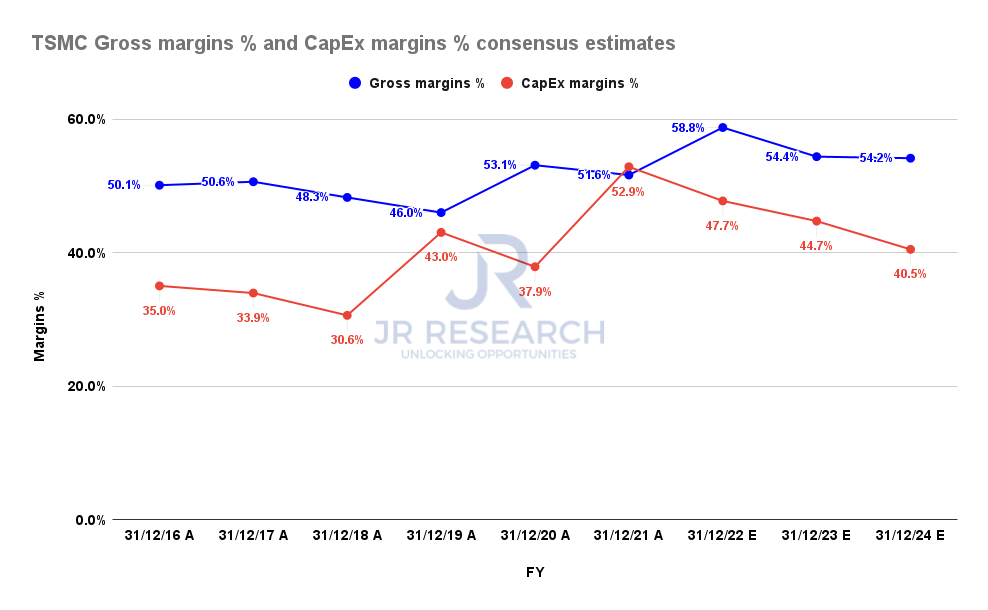

TSMC Gross margins % and CapEx margins % consensus estimates (S&P Cap IQ)

The revised consensus estimates for TSMC’s CapEx have been adjusted upward by less than 10% for its FY24 projections. Therefore, we believe the Street analysts have yet to reflect the full impact of TSMC’s $40B CapEx commitment in Arizona. Also, estimates through FY26 have also not been revised.

We need to glean the subsidies that TSMC has been offered and the cost curves that could impact its gross margins leverage, critical to supporting its profitability.

Hence, we believe TSMC’s estimates are likely due for significant revisions, given the higher manufacturing costs embedded in Arizona’s operations. As such, we postulate buyers would likely hold back adding more exposure as they assess the impact on TSMC’s bottom line.

Is TSMC Stock A Buy, Sell, Or Hold?

With the significant surge from its October lows, TSM’s NTM EBITDA multiples have normalized toward its 10Y average. Accordingly, TSM last traded at a NTM EBITDA of 7.4x, below its 10Y average of 8.2x.

Also, it’s in line with its foundry peers’ median of 7x (according to S&P Cap IQ data). Notwithstanding, given TSM’s foundry leadership, we believe the valuation premium is justified.

However, the undervaluation gap at its October lows has been astutely closed.

Hence, we urge investors to wait and assess TSMC’s revised CapEx guidance impact first while also waiting for an expected pullback before adding more to positions.

Revising from Buy to Hold for now.

Be the first to comment