RiverNorthPhotography

Comment on Q4 2022

After a strong 45% climb from the lows, T. Rowe Price (NASDAQ:TROW) has collapsed again and now seems close to reaching strong support around $107 per share.

TradingView

Analysts expected revenues of $1.53 billion versus $1.52 billion reported; while expected EPS was $1.71 versus $1.74 reported. Overall, revenues and EPS more or less met expectations, however, the problem is that the company expects headwinds to persist into 2023, prompting analysts to lower their expectations for future quarters.

Falling AUM

As explained in my previous articles, AUM is a key element in the profitability of this company, as a large part of its revenue is derived from it. The higher the AUM, the more T. Rowe Price earns.

In any case, after a terrible performance in 2022 for stocks and bonds, investor confidence failed and the collapse of AUM was inevitable.

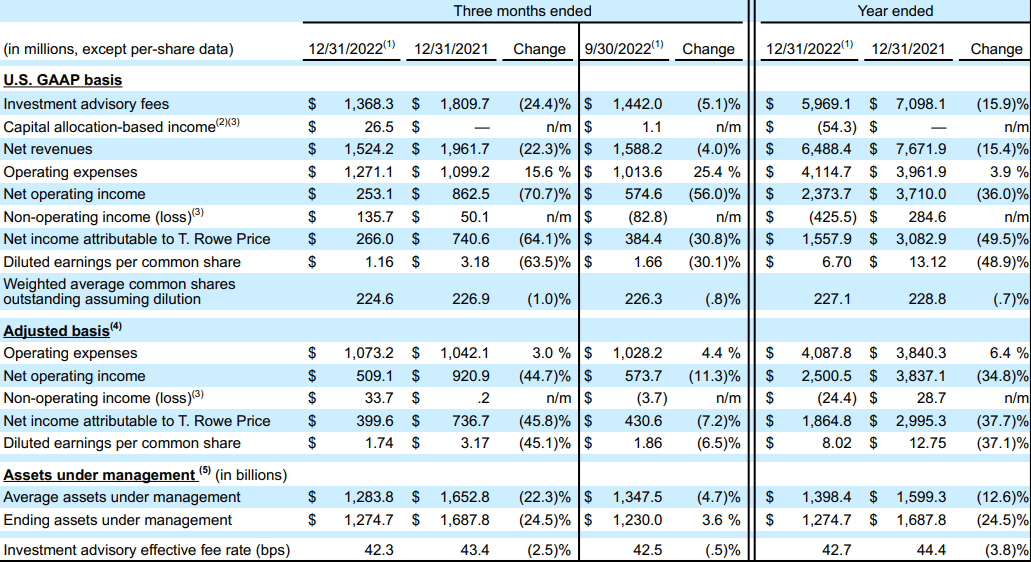

T. Rowe Price Q4 2022

As can be seen from this table, the average AUM for Q4 2022 was $1.28 trillion, while the year before it was $1.65 trillion, a 22.3% drop. This is an extremely negative result, however, I think it is useful to contextualize under what macroeconomic scenarios these two results were achieved.

- At the end of 2021, the stock market was extremely euphoric as was the bond market. So, not surprisingly, it was a very good year for T. Rowe Price in terms of new clients and increased AUM.

- At the end of 2022, the stock and bond markets together had one of the worst performances, all due to very high inflation, sudden rise in interest rates, and the Russian-Ukrainian war.

It is therefore clear that as of today the company is suffering from the over-positivity of 2021, and in my opinion the downward trend in AUM could continue in 2023 as well, albeit at a slower pace.

In any case, this may not necessarily happen since there are already some small signs of recovery. The stock market is rebounding strongly from the lows and there are also small signs of recovery in AUM. In fact, if we compare the ending AUM of Q4 2022 and the ending AUM of Q3 2022 we can see that there has been a small increase of 3.60%. This could be the beginning of renewed confidence toward the financial markets or yet another bout of positivity in a bearish underlying trend.

Managing expenses

With a struggling AUM pulling down revenues, T. Rowe Price is intent on reducing its expenses in order not to hurt its margins too much. On this issue, CEO Rob Sharps provided a rather exhaustive response.

To address this decline and to protect our capacity to invest in strategic initiatives, we focused on controlling expenses by cutting third party spend, initially slowing the pace of hiring, and ultimately reducing our headcount by about 2%. GAAP expenses for the year were $4,115 million, while non-GAAP expenses were $4,088 million, up 6.4% over 2021 due to the addition of OHA. We remain committed to managing expenses in light of the current market environment while thoughtfully investing in our strategic growth initiatives.

As T. Rowe Price is a company with historically very low debt, it is critical that profits do not decline too much, otherwise it may no longer be possible to self-finance.

Shareholder remuneration

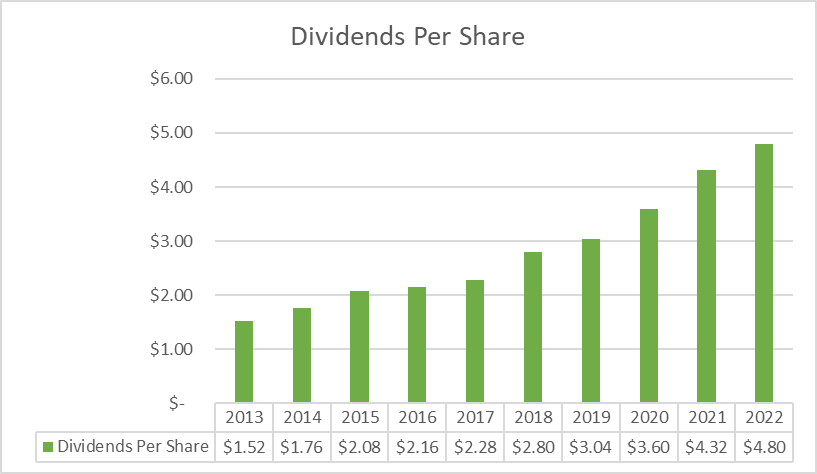

Despite a subdued 2022, T. Rowe Price shareholders were once again amply rewarded through buybacks and dividends.

- As for the buyback, 6.8 million shares were purchased in the full 2022 for $855.30 million, reducing the weighted average number of shares outstanding to 224.3 million.

- As for dividends, $1.10 billion was distributed in the full 2022, bringing the dividend per share to $4.80. The pace at which this company increases dividends is impressive.

TIKR Terminal

Moreover, despite recent increases, the dividend is still largely covered. Cash provided by operating activities was $2.35 billion in 2022, well above both the dividend issued ($1.10 billion) and capex ($216 million).

Final considerations

2022 was not a positive year for T. Rowe Price, and Q4 still showed signs of weakness. AUM is struggling to grow, and as a result the company is far from the all-time highs achieved in 2021. However, as argued in previous articles, I consider these difficulties to be only temporary, and once positivity returns to the financial markets T. Rowe Price will return to growth. In any case, being a shareholder of this company is not that bad even during such a complex period since it continues to increase its dividend (sustainably) and continues to make buybacks. For those who do not know, we are talking about a very high dividend yield of over 4%. In my opinion, this company remains a good investment at the current price, especially for those with a long-term view focused on dividends.

Be the first to comment