Techa Tungateja

Introduction

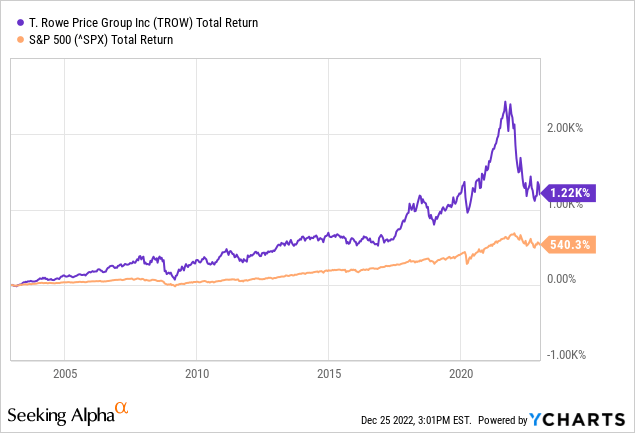

Total return for T. Rowe Price (NASDAQ:TROW) over the last 20 years has averaged 13.7%, significantly higher than the S&P 500’s total return of 9.0% over the same time period. Since the beginning of this year, the stock has been in a bear market, falling by over half from its all-time high.

As a result of the recent price drop, shares of this company are now reasonably cheap. Despite this, several analysts have reduced their earnings forecasts due to slowing investment advising fees and falling assets under management against a background of unpredictable financial markets.

Although I predicted a broad decline in stock prices back in August, I haven’t changed my mind. While falling markets are bad for T. Rowe Price, they won’t last forever.

The Stock Market Will Not Drop Indefinitely

T. Rowe Price’s AUM income is negatively impacted by falling stock prices. As inflation rises, more and more investors flee the market. Unfortunately, the market downturn shows no signs of abating.

I predicted a recession in an article I published early this year. When compared to recent highs, the S&P 500 (SP500) is currently down considerably. I expect further price decreases in 2023 due to the inverted yield curve and the low earnings yield of the S&P 500. Despite the recent rebound, the stock market is still in “bear territory.”

The yield curve has inverted, indicating a recession is highly likely to occur within the next 12 months based on past history. If the yield curve inverts, the S&P 500 may drop by more than 20% from its high to low.

The 2023 projected 5% interest rate is now equal to the S&P 500′ earnings yield. Since investing in the stock market entails more danger than investing in government bonds, the 2023 earnings yield will need to exceed the interest rate of 5%. The earnings yield of the S&P 500 rises as the index falls.

One bright spot is that analysts expect the S&P 500’s earnings to grow by 5.1% next year. The S&P 500’s PE ratio is 15.4 if we apply a premium of 1.5% to the interest rate (earnings yield = 6.5%). By the end of 2023, I anticipate the S&P 500 will have fallen to $2800.

Asset Under Management Is Showing Signs Of Improvement

The company’s third-quarter results were mixed, as it continued to see a slowdown in investment advising fees and a decline in assets under management in the face of volatile financial markets.

The $1.59 billion in revenue was higher than expected, yet this was still a 22% year-over-year decline. Earnings per share fell to $1.86, a decrease of 43% from the previous year. Net client outflows were $24.6B, up from $14.7B in Q2, and investment advising fees fell 20.5% to $1.44B.

Compared to the same period a year ago, managed assets decreased by 31% to $1.23T by the end of Q3.

Despite what seems like gloomy third-quarter numbers, AUM is actually on the upswing. The total value of assets under management (AUM) hit $1.28T by the end of October and rose to $1.34T in November, an increase of 4.7%.

Though ten analysts have lowered their earnings forecasts for T. Rowe Price, I believe they are being overly negative about the company’s near-term prospects. The current increase in AUM is excellent news for the firm. In 2023, the direction of the S&P 500 is anyone’s guess, therefore high volatility is to be expected. On the long run, the business is a solid long-term investment.

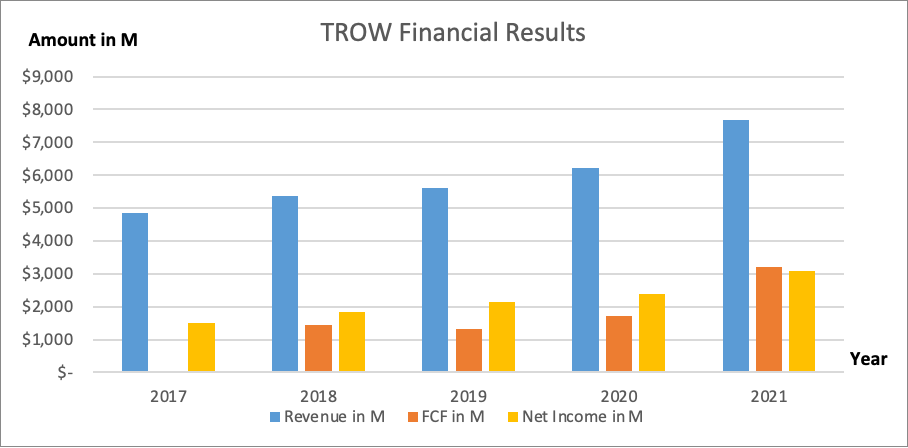

During the previous three years, T. Rowe Price has had significant growth, with yearly sales increases of 12% on average. Free cash flow was only $43M in 2017, but has grown significantly to $3213 in 2021. Net income grew strongly by 10% yearly.

Strong management and consistent execution have led to the company’s consistent growth throughout the years. I anticipate this high standard of performance to persist for the foreseeable future.

T. Rowe Price Financial Results (SEC and author’s own graphical representation)

Dividends And Share Repurchases

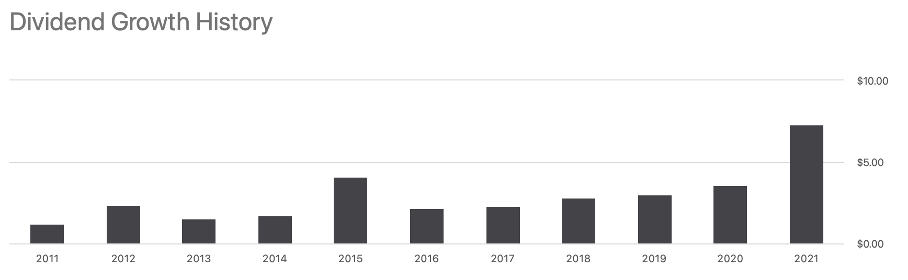

Over the past ten years, dividends have seen significant growth, indicating average growth of more than 14.5% (excluding the impact of any special dividends). The company’s dividend yield is 4.3%, and the dividend rate is currently set at $4.80.

Dividend growth history (Seeking Alpha TROW ticker page)

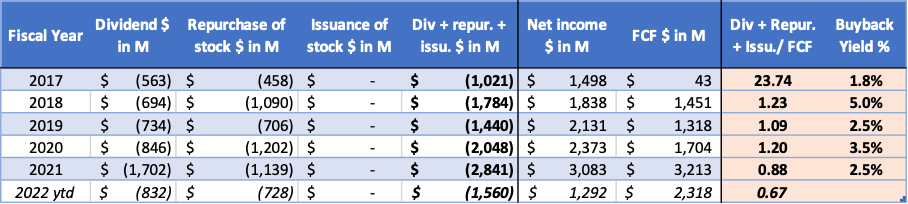

If we dig into the cash flow statement, we can see that the company also repurchases shares. This is beneficial to shareholders because it increased dividends per share. And the decreased supply and increased demand should lead to a rise in the stock price.

The company returned in 2021 about 88% in value to shareholders, a figure that seems sustainable for the long term.

T. Rowe Price Cash Flow Highlights (SEC and author’s own calculations)

The Stock Is Into Buying Territory

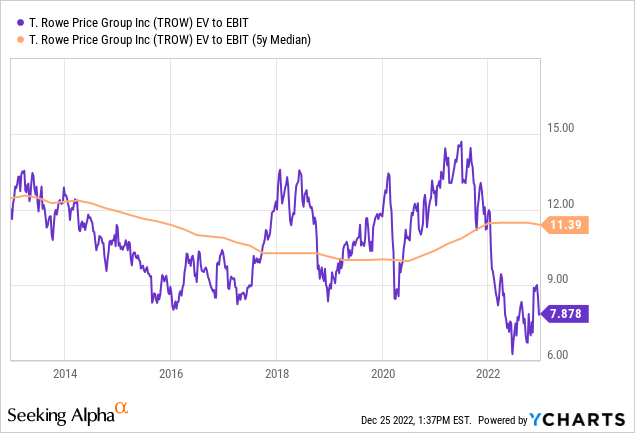

Finally, we arrive at the valuation figures. The Enterprise Value to EBIT ratio is useful because it factors in both cash and debt when determining a company’s valuation. The current EV/EBIT ratio of 7.9 is a deep discount when compared to the company’s historical EV/EBIT ratio of 11.4.

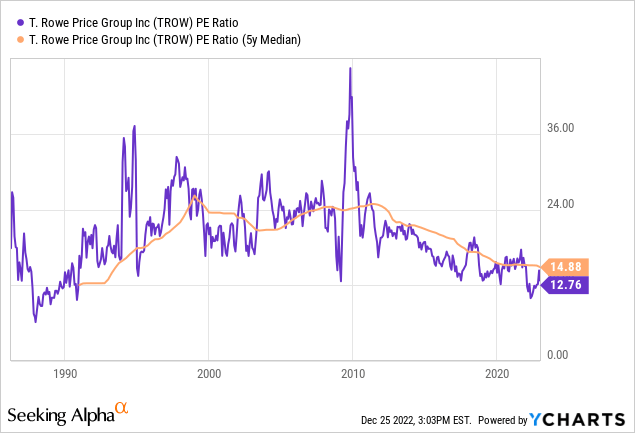

The PE ratio is another metric used to help value stocks. The price-to-earnings ratio for T. Rowe Price is 12.8, which is lower than the average PE ratio of 14.9 seen over the past five years. Despite the falling interest rate since 2010, its 5-year average PE ratio has been falling since 2010. This is odd because due to the interest rate cuts, asset prices should rise.

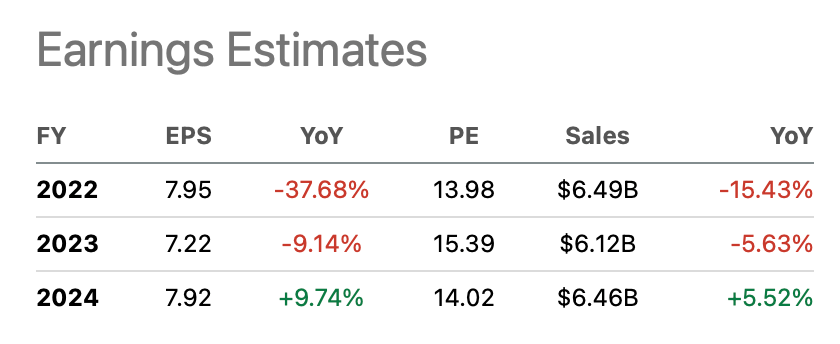

Forecasts for its EPS in the near future are met with skepticism. Ten analysts recently revised earnings per share downward. The stock appears to be fairly priced at a PE ratio of 15 based on projections for the fiscal year ending in 2023. However, when the EV/EBIT ratio is considered, the stock is favorably valued. Although it is currently impossible to tell whether earnings per share will fall after 2023, the company is very cheap relative to its historical PE ratio and attractive EV/EBIT ratio. For this reason, investing in the stock is a sound decision.

T. Rowe Price Earnings Estimates (Seeking Alpha TROW Ticker Page)

Conclusion

Price decreases in the stock market will continue until 2023 due to the inverted yield curve and low earnings yield of the S&P 500. A recession is highly likely to occur within the next 12 months based on past history. If the yield curve inverts, the index may drop by more than 20% from its high to low. The company’s third-quarter results were mixed, as it continued to see a slowdown in investment advising fees and a decline in assets under management.

T. Rowe Price has expanded greatly, with average yearly sales growth of 12 percent. Strong annual growth of 10% was seen in net income.

Dividends have grown at an average rate of more than 14.5% over the past ten years. The company’s dividend yield is 4.3%, and the dividend rate is currently set at $4.80 per share. T. Rowe Price’s price-to-earnings ratio is 12.8, which is lower than the average PE ratio of 14.9 seen over the last five years.

Despite analysts’ gloomy predictions for the stock, it’s a good investment due to its solid growth record, competent management, and reasonable price.

Be the first to comment