filadendron/E+ via Getty Images

Having recently reviewed several restaurant companies, today I take a look at the leading supplier to the US foodservice industry, Sysco (NYSE:SYY). As I discuss below, Sysco is an excellent business which will likely get even stronger going forward.

While Sysco shares trade around my estimate of fair value, this is a business I’d love to own at the right price (I typically look to buy in at a 30%+ discount to my fair value estimate). With a looming recession and concerns over consumer spending, Mr. Market might give me a chance to own this business in 2023.

Competitive Strengths

Sysco is the market leader in food distribution to restaurants with an estimated market share of 17%, followed by US Foods (USFD) at 8% and Performance Food (PFGC) with 7% market share. Beyond these three leaders, the industry is highly fragmented. Sysco has steadily gained market share over the past couple decades both organically and through acquisitions.

Sysco Overview (Sysco Investor Presentation)

Sysco’s tremendous relative scale is a source of significant competitive advantage, including:

- Greater purchasing power – Sysco’s purchases nearly $60 billion worth of food related supplies annually.

- Operational efficiency, or the ability to leverage logistical and overhead costs. Sysco’s high market share ensures it has high route density, allowing it to serve customers at a lower cost per delivery. Similarly Sysco has built leading digital ordering and operating capabilities (again, lowering the cost to serve customers). Some of these lower operating costs are passed on in the form of lower prices (allowing Sysco to gain market share) and some are retained in the form of higher operating profit. This creates a virtuous circle where growth begets higher profitability (some of which can be reinvested) stimulating further market share gains and growth.

- Scope – Sysco has a broad product and geographical footprint. A nationwide platform allows Sysco to meet the needs of restaurant chains looking for a reliable source of consistent supply.

Food distribution is a ‘many-to-many’ distribution model. Sysco is not overly reliant on any one supplier of food, and no customer represents a significant percentage of sales. This limits the threat of disintermediation. Overall, I see Sysco as a well above average business.

Sysco’s strong financial position has also proven to be a source of competitive advantage as small local and regional competitors were forced to retrench during the pandemic when restaurant sales plummeted. As a result, Sysco picked up ~200 basis points of market share during this time. The company appears poised for continued share gains as it is better able to deal with cost inflation than smaller competitors.

Market Share Gains (Sysco Investor Presentation)

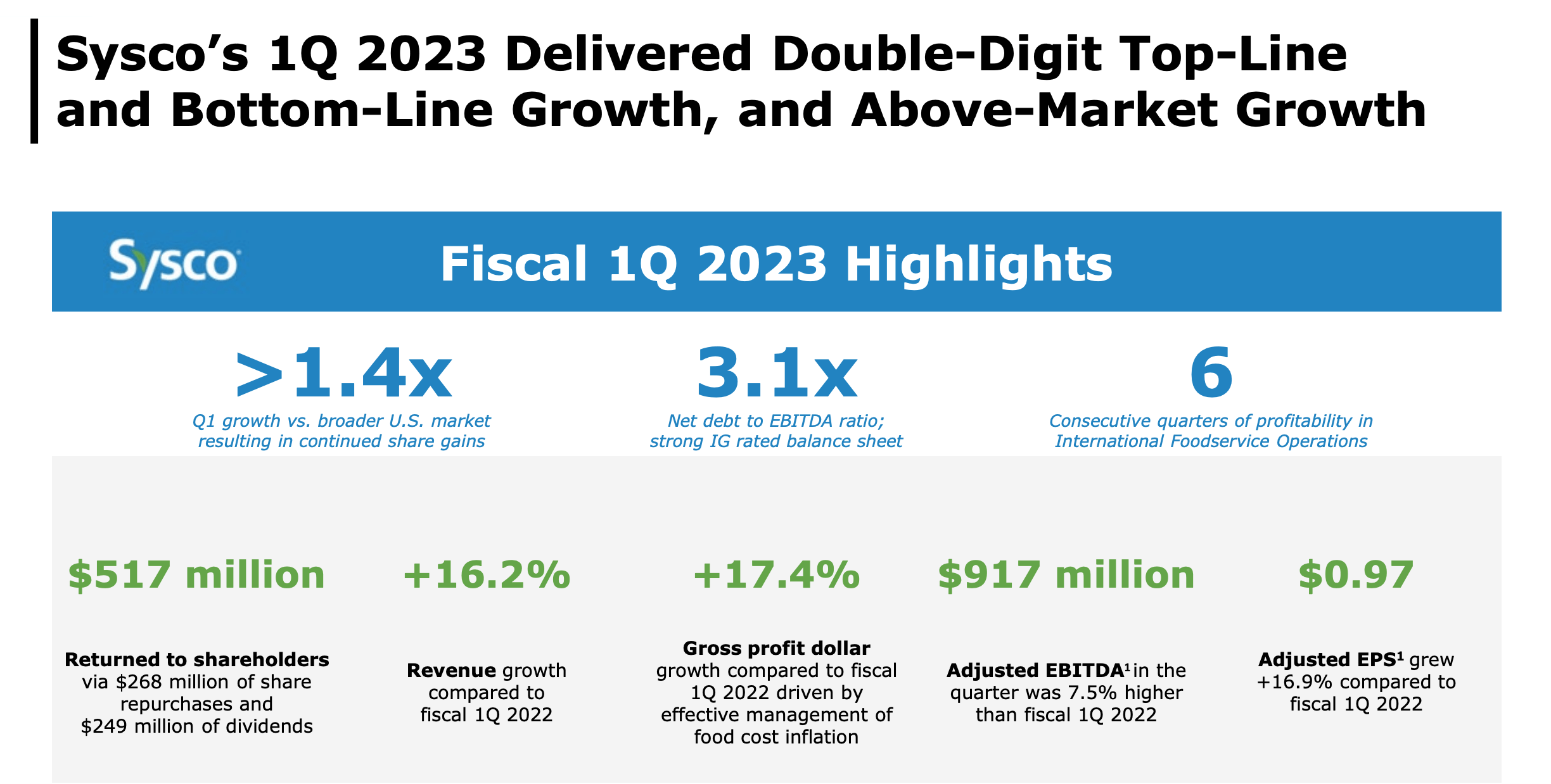

Current Results

Sysco 1Q Results (Investor Presentation)

As shown above, current results are strong. While Sysco is seeing modest contraction in EBITDA margins due to inflation, the company is doing a pretty good job of passing on commodity, fuel, and labor costs to its customers. In addition, Sysco continues to outgrow the industry (gaining market share). This all comes back to Sysco’s strong competitive position – as the industry leader, it is best positioned to deal with a challenging environment given its numerous competitive advantages (detailed above).

Sysco’s strength is in stark contrast to some of the restaurant operators like Shake Shack (SHAK), Portillo’s (PTLO), and Carrols Restaurant (TAST) that I’ve written up recently. Restaurants operate in a much more competitive environment (lower market share) and have struggled to pass along price hikes proportionate to labor and commodity cost increases.

Valuation

As we sit today, Sysco shares trade at 19x forward earnings and 13.5x EV/EBITDA. While these multiples are at the high end of Sysco’s historical trading range (16-20x P/E), I see the company as being slightly undervalued today as the business has gotten stronger and gained market share over the past several years (and will likely continue to do so).

Given its numerous competitive advantages, strong/growing market position, and fantastic (30%) returns on operating capital employed, I believe a 19-22x P/E is warranted for Sysco. This produces a fair value of range of $79-92 per share suggesting the company is somewhere between fairly valued and 14% undervalued.

Conclusion

If you’ve read this far, you have probably surmised that I very much like Sysco’s business. However as a value investor, I typically only purchase shares when trading at a 30% (or greater) discount to my $85/share estimate of fair value. As such, I will look to buy a position in Sysco should its shares trade below $60. With a looming recession and concerns over consumer spending, it looks like I might get a chance to own this business in 2023.

Be the first to comment