RandyAndy101/iStock via Getty Images

Author’s note: This article was released to CEF/ETF Income Laboratory members on December 19th.

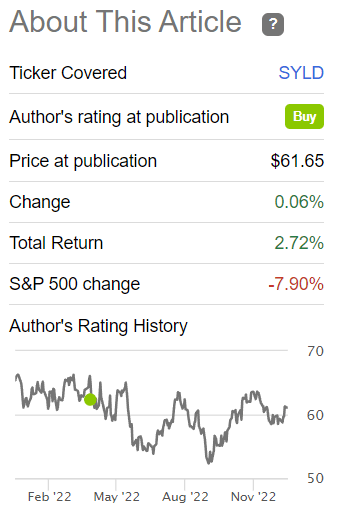

I last covered the Cambria Shareholder Yield ETF (BATS:SYLD), a U.S. equity ETF focusing on companies with above-average shareholder yields, in April 2022. In that article, I argued that SYLD’s diversified holdings, cheap valuation, and reasonably strong performance track-record, made the fund a buy. Since then, SYLD has significantly outperformed relative to the S&P 500, a strong showing for the fund.

Previous SYLD Article

Since then, SYLD’s fundamentals have improved as well, with the fund sporting a cheaper valuation and higher 2.1% dividend yield. SYLD remains a well-diversified, cheaply valued fund with a strong performance track-record, and so remains a buy.

SYLD – Basics

- Investment Manager: Cambria

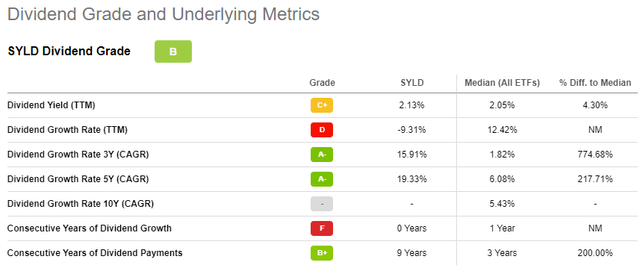

- Dividend Yield: 2.13%

- Expense Ratio: 0.59%

- Total Returns CAGR 5Y: 11.67%

SYLD – Quick Overview

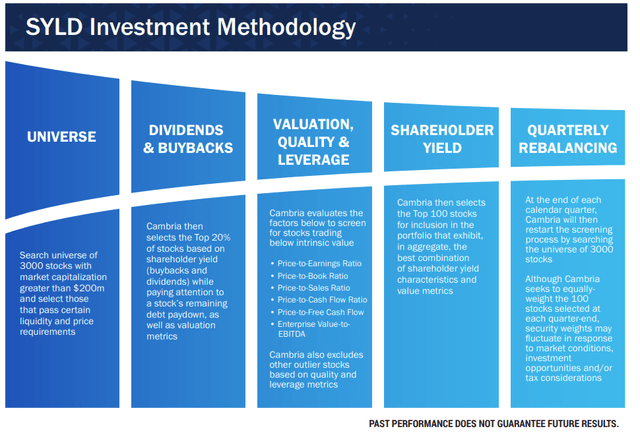

SYLD is a U.S. equity index ETF. Although the fund is actively-managed, it follows an explicit, detailed investment methodology, and so effectively functions as an index / smart beta fund. SYLD focuses on cheaply valued U.S. equities with above-average shareholder yields, or dividends plus buybacks. SYLD’s investment methodology is as follows.

SYLD

Although the fund’s strategy seems a bit complex, it is actually remarkably simple: the fund simply invests in cheaply valued U.S. equities with above-average shareholder yields. As with most strategies, applicable securities must also meet a basic set of inclusion criteria. The fund also screens for quality and momentum metrics when constructing its portfolio, but the focus is on value and shareholder yield. Securities are equal-weighted. The end result should be a fund with an incredibly cheap valuation, as is indeed the case.

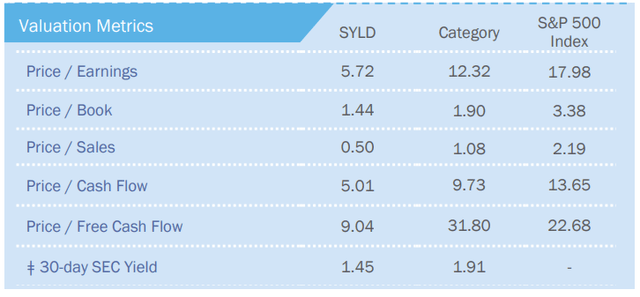

SYLD

As can be seen above, SYLD’s valuation is significantly lower than those of its peers, and of the S&P 500. The fund does not seem to provide investors with an estimate of the shareholder yield of its underlying holdings, an important oversight for a fund focusing on said metric. Still, I’m quite confident that the fund’s shareholder yield is higher than average, as is the case for the fund’s other valuation metrics.

Although the fund does not explicitly target or focus on mid-cap equities, these tend to trade with cheaper valuations than large-caps, so the fund ends up focusing on mid-caps. SYLD’s underlying holdings have an average market cap of $19 billion, compared to $25 billion for a mid-cap equity index, and $471 billion for the S&P 500. SYLD’s comparatively small holdings are somewhat riskier than average, as smaller companies are generally less diversified, and less resilient than their larger peers.

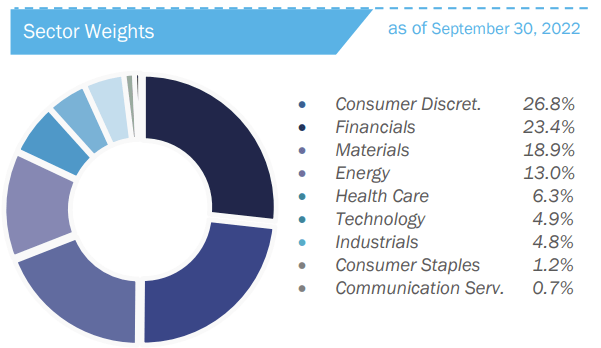

SYLD is a reasonably well-diversified fund, with investments in 100 equities, and with exposure to most relevant industry segments. Segments are as follows.

SYLD

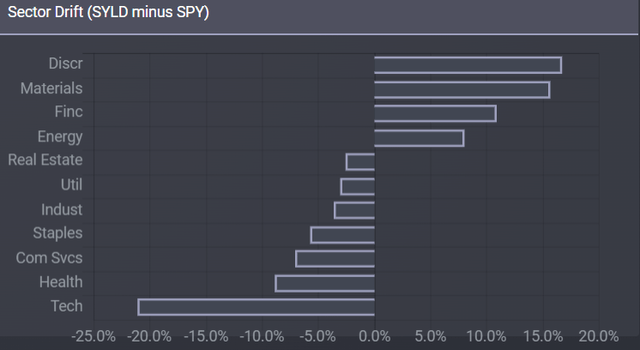

SYLD’s industry exposures markedly differ from those of broader equity market indexes, including the S&P 500. SYLD is significantly underweight tech, as said sector tends to sport comparatively expensive valuations. SYLD is significantly overweight some old-economy industries, including consumer discretionary and energy, as said sectors tend to sport comparatively cheap valuations. Industry exposures vis a vis the S&P 500 are as follows.

Etfrc.com

SYLD’s industry exposures have important effects on the fund’s relative performance. The fund tends to underperform when tech outperforms, as was the case prior to 2020.

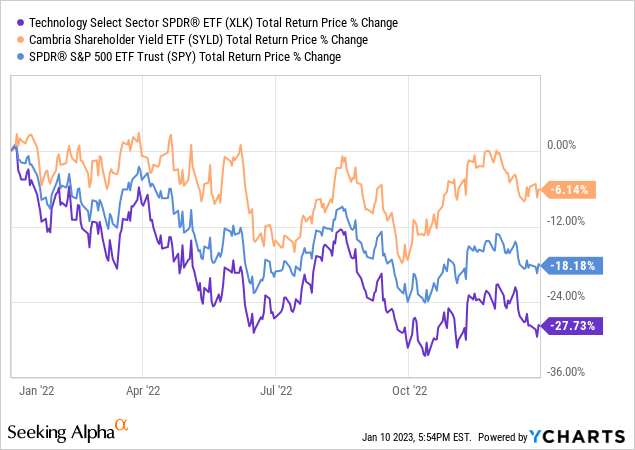

The fund tends to outperform when tech underperforms, as was the case in 2022.

In my opinion, SYLD’s industry exposures are neither a positive nor a negative, but they are an important fact for investors to consider. Tech bears might find the fund’s low tech exposure enticing, tech bulls might wish to consider other funds.

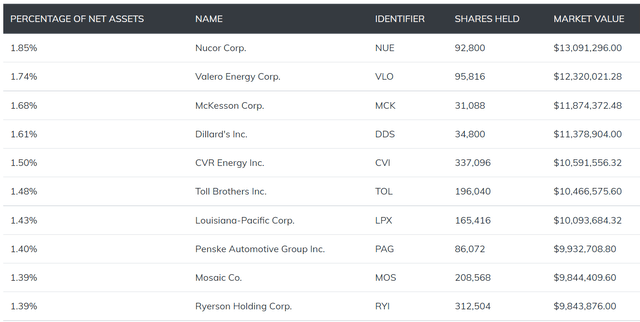

As a final point, thought to include SYLD’s largest holdings. As the fund is equal-weighted, these are simply the holdings which have performed best these past few months. I’m seeing materials, metals and energy, which have performed quite well indeed.

SYLD

In summary, SYLD focuses on cheaply valued U.S. equities with above-average shareholder yields.

SYLD – Improved Fundamentals

I’ve written for Seeking Alpha for a few years now, and as time goes on more and more of my articles are updates on previously covered funds. I’ve been meaning to focus on how fund fundamentals have changed when writing these updates, as doing so seems like a much more worthwhile endeavor than rehashing the same broad points. So, let’s do just that for SYLD.

Improved Performance Track-Record

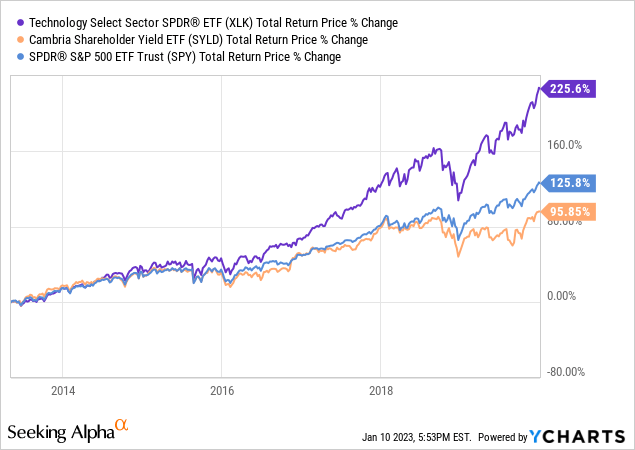

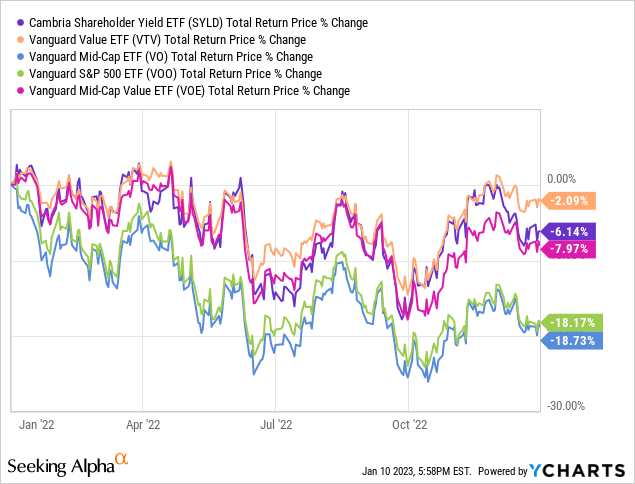

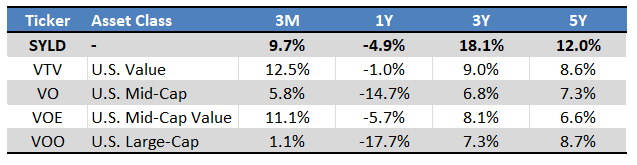

SYLD’s performance track-record has improved since early 2022, with the fund moderately outperforming relative to most relevant equity market indexes for the year. On the other hand, SYLD underperformed relative to broad large-cap value equity indexes, but not significantly so.

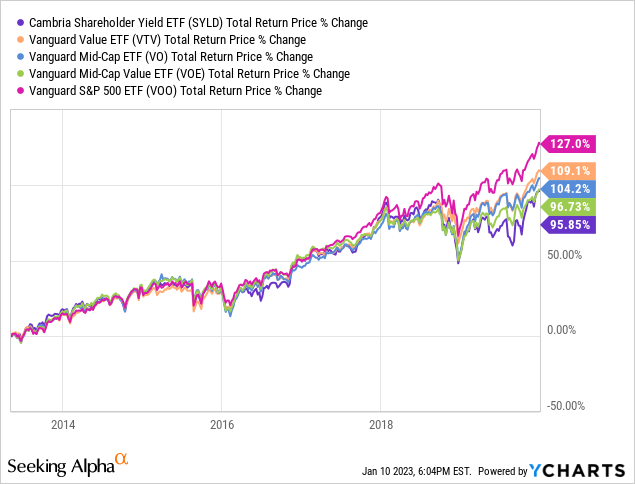

SYLD’s long-term performance track-record remains strong, with the fund slightly outperforming relative to most of its peers since inception / long-term.

SYLD

Although the figures above are accurate, I feel they overstate the consistency of SYLD’s performance. Fund returns are quite volatile, sometimes markedly differ from those of its peers, sometimes significantly lower. As an example, SYLD consistently underperformed its peers before 2020, a period of strong tech outperformance.

SYLD’s performance track-record is quite strong, but volatile, and investors should expect renewed underperformance if tech soars once more.

Improved Dividend Yield

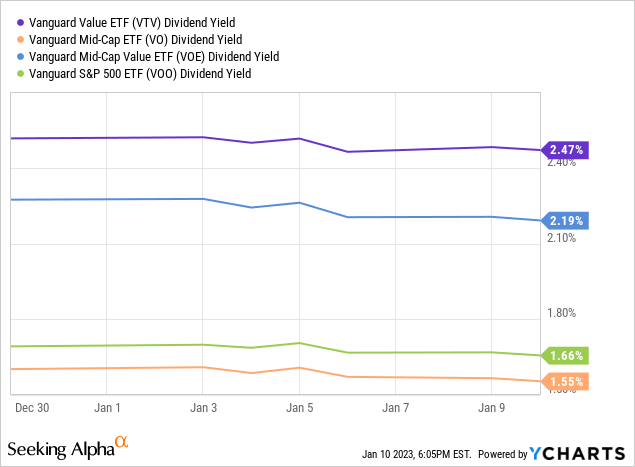

Although SYLD is not a particularly effective income vehicle, the fund does provide investors with an above-average, growing 2.1% dividend yield. Excluding an abnormally large dividend late in 2021, the fund’s dividends grew 36.6% last year.

SYLD’s dividend yield is slightly higher than that of the average equity index fund, but slightly lower than that of the average value equity index fund.

SYLD’s long-term dividend growth track-record is materially stronger, with the fund growing its dividends at a double-digit annual growth rate since inception, versus high single-digits for its peers. SYLD’s strong dividend growth track-record is a benefit for all investors, but should prove particularly impactful for long-term dividend growth investors, who would likely see strong long-term yield on cost from the fund.

SYLD

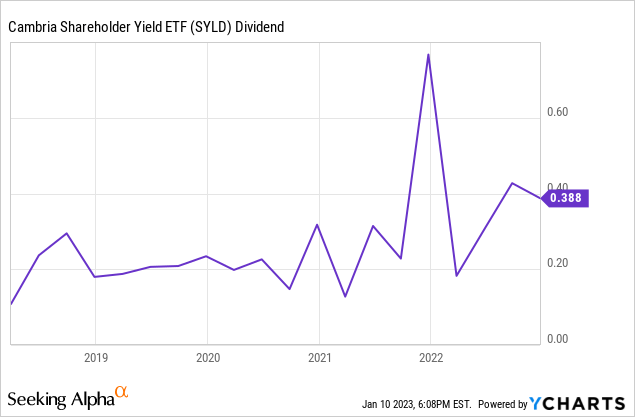

On a more negative note, SYLD’s dividends are somewhat volatile, quite a bit more than average.

The volatility itself is a negative for many investors, and it also makes it very difficult to ascertain the fund’s expected yield / dividend growth. As an example, 5Y yield on cost metrics for the fund went from 5.1% to 3.3% in the span of two weeks, as these went from including the abnormally high dividend in late 2021, to excluding the same. From what I’ve seen, dividends have grown even after accounting for said volatility / the most recent dividend spike, but it is obviously difficult to separate actual dividend / dividend growth from volatility.

Improved Valuation

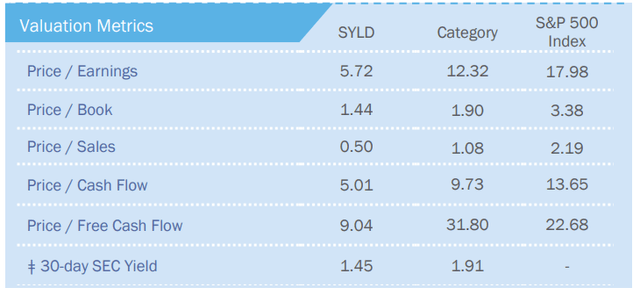

SYLD’s valuation has improved these past few months, product of a stagnating share price plus strong earnings growth. The fund’s PE ratio improved from 8.1x to 5.7x, and its PB ratio improved from 1.7x to 1.4x. Both are sizable reductions, but of about the same magnitude as those of the broader equity market / most of its peers.

SYLD

SYLD remains a cheaply valued fund, which could lead to strong capital gains and market-beating returns moving forward. Due to the fund’s low yield, returns are strongly dependent on market sentiment. Share prices could drop if sentiment worsens, and the fund lacks the dividends to cover any such drop effectively. Sentiment could worsen for a myriad of reasons, but worsening economic conditions seems the most plausible. Significant capital losses are likely if the U.S. enters a recession in 2023, which seems possible.

Notwithstanding the above, I remain bullish, as the market itself has been bullish about value stocks since early 2022, and as economic conditions remain adequate. A recession is possible, especially if the Fed is forced into further significant rate hikes to combat inflation, but far from certain.

Conclusion

SYLD’s fundamentals have improved these past few months, and it remains a diversified, cheaply valued fund with a strong performance track-record. SYLD is a strong investment opportunity, and a buy.

Be the first to comment