Orietta Gaspari/E+ via Getty Images

Investment Thesis: I take the view that Swiss Re will see low growth in the short to medium term.

Swiss Re (OTCPK:SSREY) (OTCPK:SSREF) has continued to see downside in 2022 – owing to broader macroeconomic risks and continued uncertainty over the ongoing situation in Ukraine.

investing.com

While I originally made the argument back in April that Swiss Re could be in a position to benefit from rising inflation due to appreciating real estate prices – I also cautioned more recently that this could prove to be a double-edged sword, as higher interest rates could instead curb property demand and hence demand for property insurance.

The purpose of this article is to examine Swiss Re’s business from a more holistic perspective, and determine whether the stock has scope to rebound given the current macroeconomic conditions.

Performance

Taking the growing macroeconomic pressures into account, investors are likely to pay more attention to cash flow, in order to ensure that Swiss Re can continue to finance its short-term liabilities while remaining profitable.

When looking at cash to short-term debt, we can see that while Swiss Re still has more than sufficient levels of cash to cover its short-term debts, the cash to short-term debt ratio has dropped. Long-term debt has increased slightly, but Swiss Re has also managed to raise its cash levels accordingly.

| Item | December 2021 | June 2022 |

| Cash and cash equivalents | 5051 | 5277 |

| Short-term debt | 862 | 1539 |

| Long-term debt | 10323 | 10633 |

| Cash to short-term debt ratio | 5.859 | 3.428 |

| Cash to long-term debt ratio | 0.489 | 0.496 |

Source: Figures sourced from Swiss Re Half-Year 2022 Report. Cash ratios calculated by author. All figures in USD millions except cash ratios.

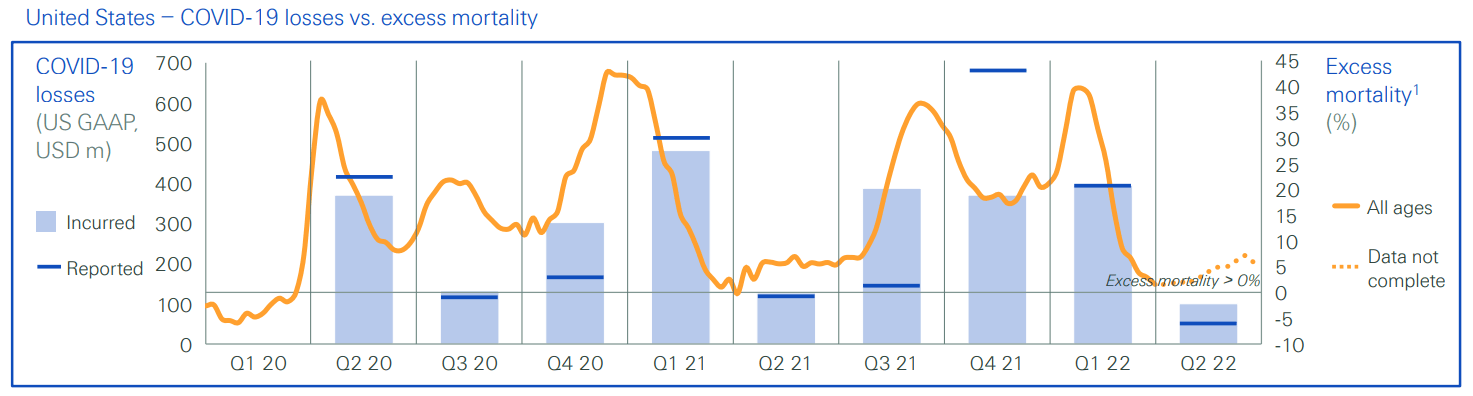

When looking at segment performance, we can see that the Life & Health segment benefited significantly from a drop in excess mortality across the United States in the second quarter.

Swiss Re Half-Year 2022 Results Presentation

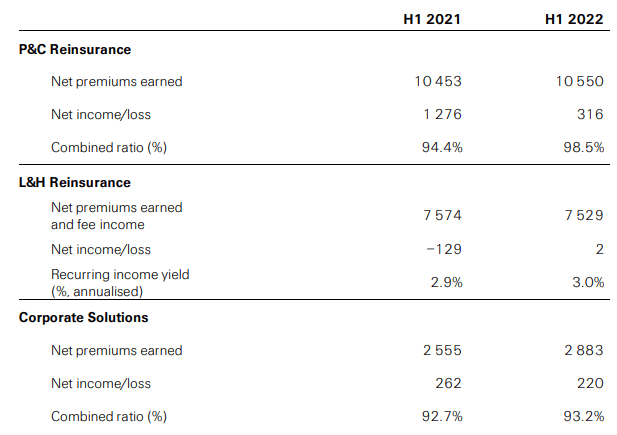

With that being said, we did see an increase in the combined ratio across the Property & Casualty segment – meaning that the amount of claims relative to premiums collected has increased.

Moreover, while we can see that the Life & Health segment has returned to profitability – net income as a whole still remained quite low for H1 2022:

Swiss Re Press Release H1 2022

From this standpoint, the Property & Casualty sector as a whole has become more expensive to insure in the past year. Moreover, while net income has come back into positive territory across Life & Health – this has only been marginal and cannot compensate for the drop in net income growth across P&C. Additionally, while excess mortality has dropped in the most recent quarter – there is a possibility that this metric could increase once again if the coming winter results in a greater degree of COVID-related outbreaks.

Looking Forward

While the Life & Health sector has seen an encouraging recovery, the possibility of further COVID outbreaks this winter could result in a rise in claims and thus place pressure on the sector.

Additionally, inflation and higher property prices mean that the cost of insuring such properties will also rise. We can see that while the value of real estate investments for Swiss Re has increased from last year, the overall return on equity for the group has been lower – which would be expected given the broader decline that we have been seeing in the equity markets:

Investment Real Estate

Swiss Re Half-Year 2022 Report

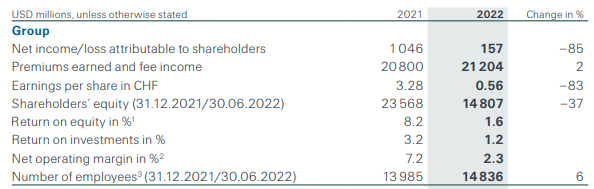

Financial Highlights

Swiss Re Half-Year 2022 Report

Given that inflation shows no signs of abating for the foreseeable future – I take the view that this trend could continue as we head into the rest of this year, and Property & Casualty could become more expensive to insure as a whole.

This, coupled with the potential for a greater number of claims across Life & Health could place pressure on net income growth overall.

Conclusion

To conclude, I take the view that while Swiss Re remains a fundamentally strong insurance company – macroeconomic pressures, inflation and low equity market growth could lead to greater expense for the company going forward.

For these reasons, Swiss Re could see low to modest growth for the remainder of this year.

Be the first to comment