NicoElNino

The Quarter

SVB Financial (NASDAQ:SIVB) reported Q4 EPS of $4.62, which missed consensus estimates of $5.27. Beats versus guidance in NIM (net interest margin), results from the securities division, and the tax rate was offset by higher-than-expected expenses and loan loss provisions, which almost doubled from Q3 2022.

The company also guided to 2023 NIM at a range of 1.75-1.85% versus estimates of 1.89% as more deposits shifted from NIB (non-interest bearing) to IB and the deposit rates increase.

Normally, these results would not be the reason to celebrate. However, the company also added that client cash burn moderated in Q4. For 2023 management expected continued burn moderation, a modest recovery in venture funding, as well as low-double digit loan growth despite mid-single digit deposit decline and year-over-year income growth in SVB Securities. This guidance, which in my opinion is highly unlikely to play out, combined with what I believe were people shorting into the earnings report led to ~a 20% pop in the stock despite a greater than 10% earnings miss. I think this pop is likely to reverse for a number of reasons.

Problems with SIVB’s Quarter and Guidance

Q4 earnings would have been even worse had the company not marked up its warrant portfolio to the tune of $28 million versus $40 million gains in Q3. The warrant portfolio stood at $383 million, so Q4’s markup was about 8%. It also added about $.38/share to earnings. Nasdaq was down about 4.5% and flat in Q3 and Q4, respectively. I have not seen VC firm marks for Q4, but every Q3 mark I saw was down. Given that backdrop, call me crazy, but gains in warrants of largely startup/technology companies in Q3 and Q4 are hard to believe.

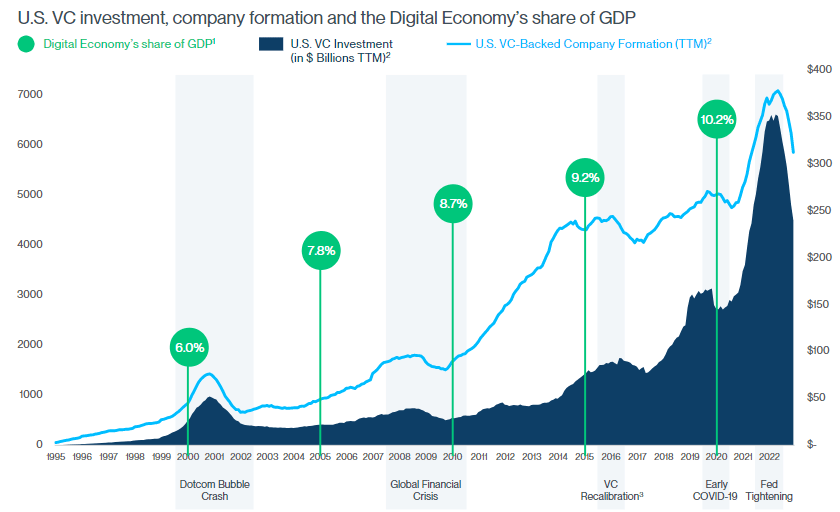

Sticking with the VC theme, I also find it hard to believe that the VC investment environment will materially improve this year. There was a massive spike in VC investment between 2018 and 2021. If you look at the chart below, the first major spike in VC investment occurred at the tail end of the dot com bubble. Close inspection reveals that VC investment plummeted afterward and then stayed at a low level for the subsequent 5-6 years. Furthermore, VC investment did not recover to 2000 levels until around 2015. That fact pattern does not give me much faith that VC Investment will rebound in short order, particularly given how logarithmic the spike was from 2018 to 2021.

US VC Investment (SVB Financial Presentation)

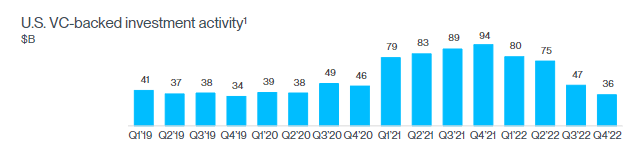

Indeed, VC investment in Q4 was down 60% from Q4 2021 as you can see in the chart below. This dynamic does not bode well for client deposits.

US VC Investment by Quarter (SIVB Presentation)

The other consideration of the spike in VC investment is the valuations that likely accompanied that tidal wave of capital. Those valuations are important as they are a basis for SIVB’s loans. Usually, the LTV (loan to value) is based on the last VC equity valuation. If valuations come down with VC investment, then LTV’s go up organically and become more susceptible to loss. In my last write-up (which admittedly looks way early), I called out that I thought the biggest risk to SIVB was potential losses in the loan to early-stage/start-up companies. I believe that this risk remains.

Valuation

The analysts’ earnings range for 2023 is $19-28. I think the top end, which represents greater than 10% earnings growth, is going to be virtually impossible given deposit trends and NIM. Frankly, given what I discussed above, I see the low end as perhaps aspirational. But if $19 turns out to be the earnings number, then this stock is incredibly overvalued in my opinion at close to 1.5x book value and over 15.5x earnings. The bank ran an efficiency ratio of 66% and an ROE of 8.9% in Q4. Remember, that’s with a mark-up of warrants. Those metrics combined with likely earnings declines this year do not warrant a premium valuation. If management’s rosy scenarios for year-end do not play out, I don’t see why this stock does not drop to a tangible book value of ~$200, which would also represent about 10.5x likely earnings. That’s 30% lower.

Risks

The main risk to the short is a major recovery in VC Investment and pop in valuations of technology companies. I think we’re likely to see the opposite but certainly could be wrong. Another risk is continued multiple expansion like we saw after the Q4 earnings. That likely depends on overall risk taking in the market.

Conclusion

I continue to see this bank as majorly overvalued, if not a candidate to start seeing major impairments from its loan book. I believe at the very least we will see a continued bleed in VC investment, continued cash burn at early-stage companies and continued mark-downs from prior funding rounds. Moreover, I believe this dynamic is likely to last for years, not quarters. In that environment, I see SIVB trading at a discount to book value and a low multiple of earnings (to the extent they exist), which implies ~30% downside from current levels.

Be the first to comment