Avosb

Investment Thesis

Suncor Energy (NYSE:SU) is an integrated energy company. Despite energy being a winning place to be in 2022, the second half of 2022 wasn’t great for Suncor Energy.

The reason for investors eschewing this name is that it holds a substantial amount of debt.

However, I declare that Suncor will ramp up its capital returns in less than 90 days to 75% of its free cash flow. And while investors wait, there’s a 4.62% dividend yield too.

Altogether, I show the math for why investors could get +15% combined yield in 2023. In sum, there’s much to be excited about here.

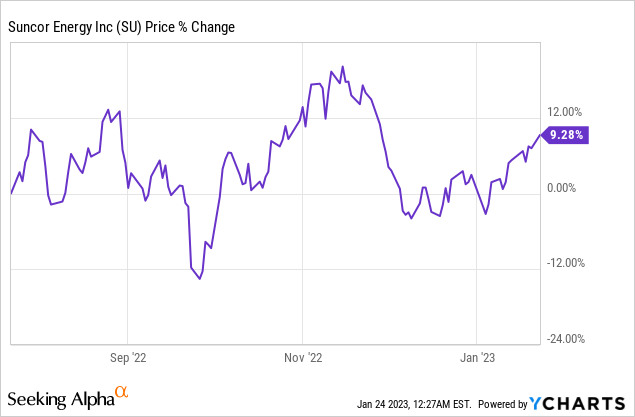

SU, A Very Volatile Stock

It would be an understatement to say that investing in Suncor over the past six months has been difficult. It has been heart-breaking, to put it more straightforwardly.

There are two aspects that have led to this volatility in its share price. In the first instance, oil prices had been noticeably weak into the end of 2022. Indeed, 2022 saw WTI end the year at the low price it had entered in 2022.

And the other blemish in this investment thesis is Suncor’s capital allocation potential, something we’ll soon discuss.

That being said, before discussing the blemish in this investment thesis, it’s worthwhile discussing the upside of investing in Suncor.

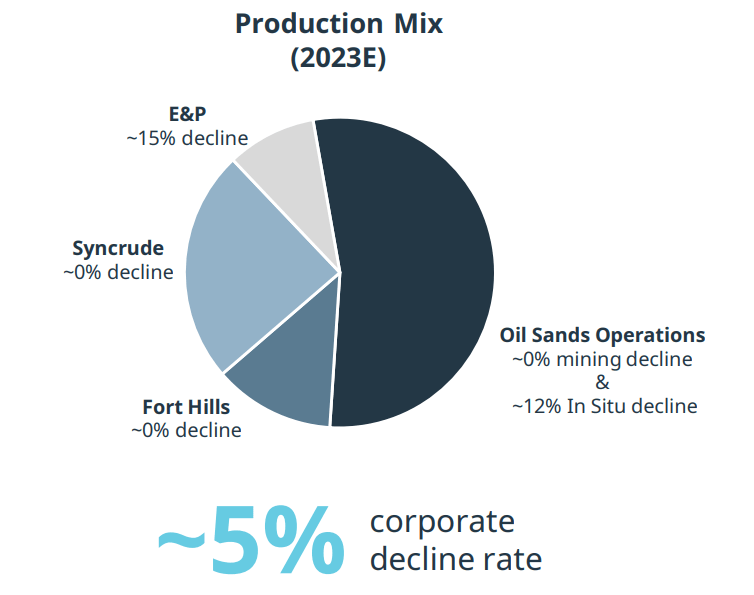

Oil Sands Advantages

SU, 29 November 2022 Investor Day

As you can see above, more than half of Suncor’s operations come from its oil sands. Oil sand mining has a notable advantage in that it has a low decline rate.

Furthermore, it’s a very reliable source of supply, as Suncor doesn’t need to dig around to find ”probable” oil. What you see is what you get.

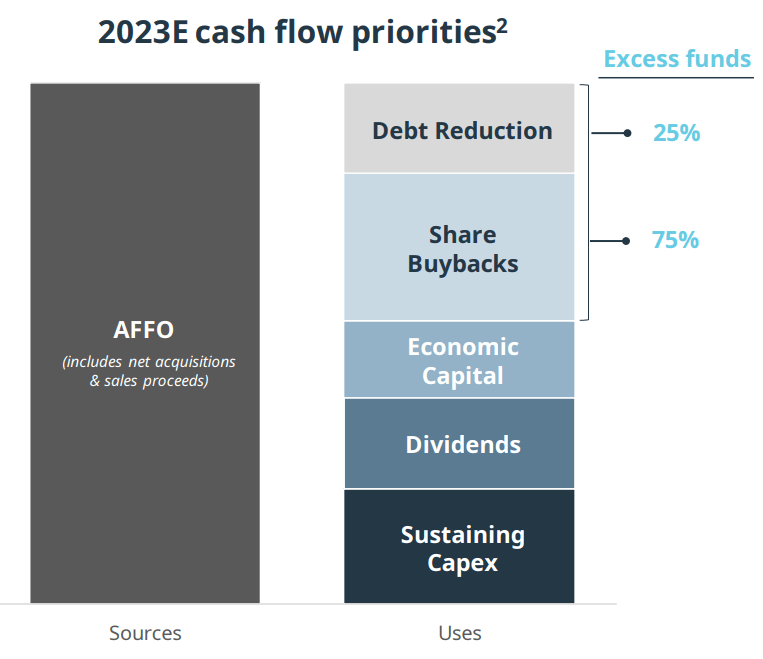

Capital Allocation Policy Discussed, +15%

Suncor’s Investor Day points to its 2023 capital allocation priority.

29 November 2022 Investor Day

Here’s the main blemish facing SU. While many of its Canadian oil peers are now very close to net debt-free, Suncor energy still carries a significant amount of debt.

More specifically, Suncor believes that at some point in Q1 2023, its net debt will fall below CAD$12 billion.

In practical terms, that means that Suncor will be in a position to start returning increased capital returns to shareholders within less than 90 days.

By the time Suncor enters Q2 2023, Suncor should be returning 75% of its excess free cash flow to shareholders via buybacks and the remaining 25% towards paying down its debt.

Consequently, Suncor will continue paying a 4.62% base dividend yield, that’s growing over time.

Plus, 75% of its excess free cash flow back to shareholders. This means that somewhere close to CAD$8 billion will be returned to shareholders via buybacks, which amount to approximately 13% yield.

Hence, via both dividends and buybacks, there could be a +15% combined yield starting Q2 2023.

In the next section, we’ll discuss what this means for shareholders.

SU Stock Valuation — Less Than 6x Free Cash Flow

I anticipate Suncor’s free cash flow to be around CAD$11 billion in 2023, just to be on the safe side. That means that the stock is priced just under 6x free cash flow.

For this figure, I have estimated that WTI stays around $80. Needless to say that this is an average figure.

Also, keep in mind that I’ve assumed that the refining margin trends back to $32 NY Harbor. Presently, the futures for refining margins are in backwardation, so there could be some further upside here. But I’ve not factored this into my +15% combined yield calculation.

The Bottom Line

Suncor has one blemish, it has a high debt load. But with oil prices and refining margins likely to remain strong in 2023, this stock should provide a suitable upside return.

Furthermore, the refining side of the business could get a further boost if it turns out that the Russian embargo on refining products has unexpected knock on effects on global diesel products.

Needless to say that the investment is not without risks. The main risk here is that if there’s a global economic slowdown, which could put a meaningful dent in oil prices, it means that Suncor Energy would not be immune to this volatility.

Nevertheless, I maintain investors have a wide margin of safety when they pay less than 6x free cash flow for Suncor.

Be the first to comment