Kativ/E+ via Getty Images

Introduction

When the calendar rolled over to 2022, disappointingly, the outlook for SunCoke Energy (NYSE:SXC) did not see not much to expect with management remaining too focused on deleveraging in my view, as my previous article discussed. Thankfully, they just announced a big dividend increase of one-third that lifts their yield to a moderate 4.43%, thereby alleviating this area of disappointment, as discussed within this follow-up analysis that sees ample scope for more to come in the future.

Executive Summary & Ratings

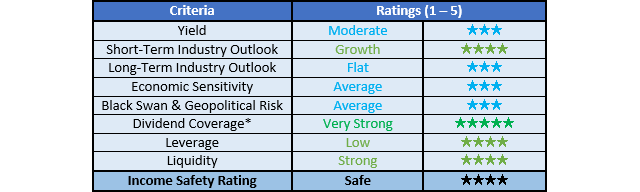

Since many readers are likely short on time, the table below provides a very brief executive summary and ratings for the primary criteria that were assessed. This Google Document provides a list of all my equivalent ratings as well as more information regarding my rating system. The following section provides a detailed analysis for those readers wishing to dig deeper into their situation.

Author

*Instead of simply assessing dividend coverage through earnings per share cash flow, I prefer to utilize free cash flow since it provides the toughest criteria and also best captures the true impact on their financial position.

Detailed Analysis

Author

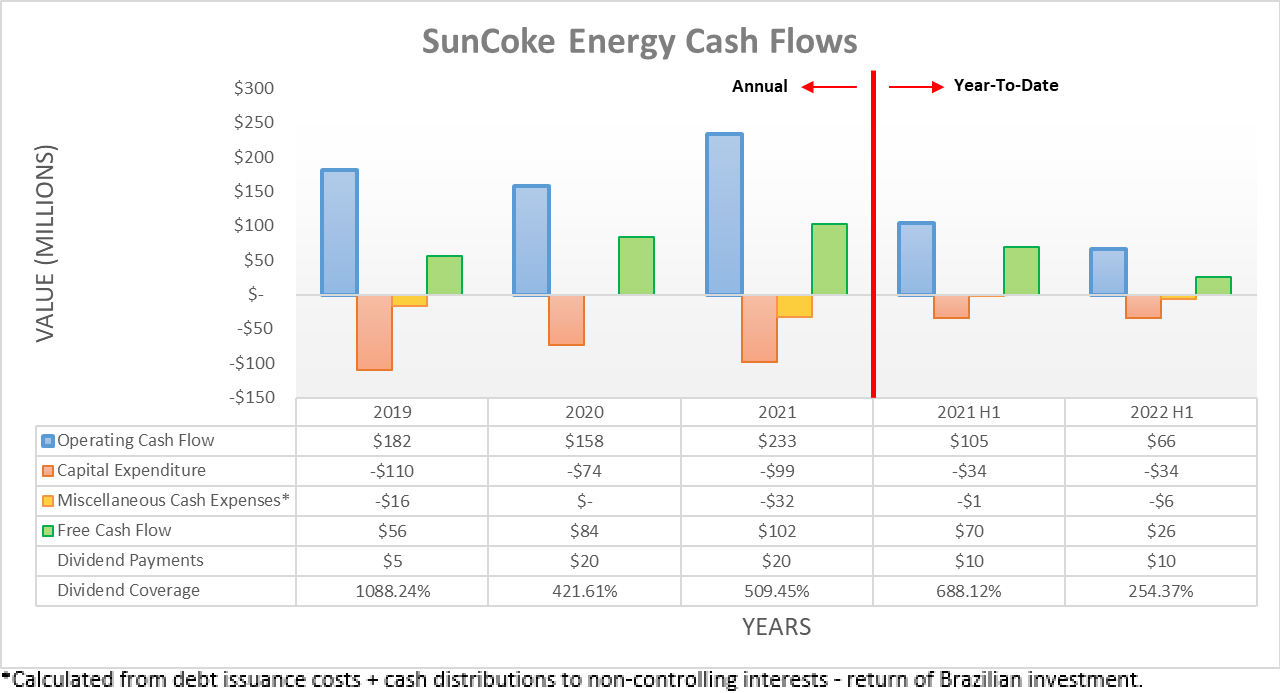

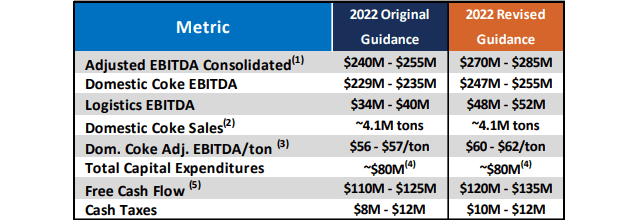

On the surface, it appears that their cash flow performance during the first half of 2022 was very disappointing, despite the strong performance during 2021. Thankfully, their operating cash flow of $66m was weighed down by a relatively oversized working capital build, which skews its comparison to their previous result of $105m during the first half of 2021. If these temporary working capital movements are removed, their underlying operating cash flow during the first half of 2022 was actually much stronger than the first half of 2021 at $131m versus $113m respectively, thereby representing an impressive increase of 15.93% year-on-year. Following this improvement on the back of the recent booming operating conditions within the metallurgical coal market, management has lifted their guidance for 2022 across the board, as the table included below displays.

SunCoke Energy Second Quarter Of 2022 Results Presentation

It can be seen that they now expect adjusted EBITDA of $277.5m at the midpoint, which is not only 12.12% higher than their original guidance but also now sits broadly in line with their previous result of $275.4m, which removes an element that tarnished their outlook at the start of the year, as per my previously linked article. Even more importantly, they have also lifted their free cash flow guidance to $127.5m at the midpoint, which is now even above the upper end of their original guidance but stems from stronger financial performance and not simply lower capital expenditure, as guidance for the latter remains unchanged at $80m. If achieved, this would amount to a forecast massive 20%+ free cash flow yield on their current market capitalization of approximately $591m, which speaks volumes to the desirable value their shares offer now that management seems intent on rewarding their shareholders. Since they only saw $26m of free cash flow during the first half of 2022, they should see far more during the second half of 2022 as their working capital build reverses.

Since their dividend payments only totaled $10.3m for the first half of 2022, the cost to fund their new one-third higher payments during the second half will be $13.7m, thereby bringing the yearly total to $24m and thus seeing at least $100m of excess free cash flow retained assuming they hit the midpoint of their guidance. Apart from indicating that further deleveraging remains on the cards, it also displays that they have ample scope to fund many more large double-digit dividend increases in the future.

Even though I personally expect the recent booming metallurgical coal market to soften going forwards given the risks of a recession on the horizon, they have traditionally fared relatively well versus the mining companies and thus this should not necessarily derail this outlook. To provide an example, 2020 was one of the toughest years in recent history, yet they still generated $84m of free cash flow and thus could still provide very strong dividend coverage, thereby leaving scope for significantly higher dividends in the future. Even though their financial position was problematic in the past, in light of their updated guidance and sudden change of course in regards to their dividends, I will nevertheless provide a refreshed analysis to offer context for any new readers.

Author

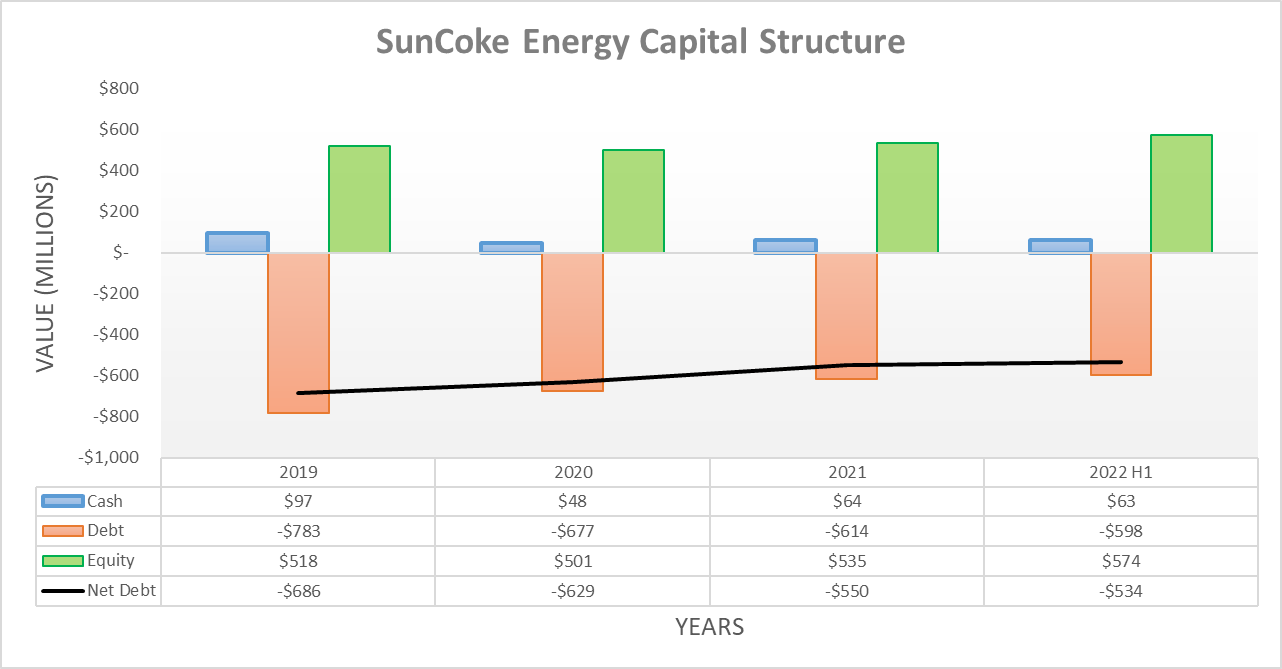

Despite seeing a relatively oversized working capital build, their barebones dividends still allowed their net debt to slide slightly lower during the first half of 2022 to $534m versus its previous level of $550m at the end of 2021. When looking ahead, the outlook for far stronger free cash flow during the second half of 2022 as their working capital build reverses stands to see this drop materially, barring any further increases to their shareholder returns. Since they generated $16m of excess free cash flow after dividend payments during the first half of 2022, given the previous estimation, it leaves another circa $84m for the second half, thereby estimating that their net debt will end the year at circa $450m or 15.73% lower.

Author

Quite unsurprisingly, their stronger financial performance saw their leverage decrease to a greater extent than their net debt with their net debt-to-EBITDA decreasing from 2.00 to 1.73, which now sits firmly within the low territory of between 1.01 and 2.00. Meanwhile, their net debt-to-operating cash flow also decreased from 2.36 to 2.04, which should easily fall into the low territory during the second half of 2022 given the outlook for materially lower net debt. Since this obviously poses no threat to their solvency, it clearly highlights the main point behind my disappointment when conducting the previous analysis, which is thankfully now alleviated with management providing a big dividend increase.

Author

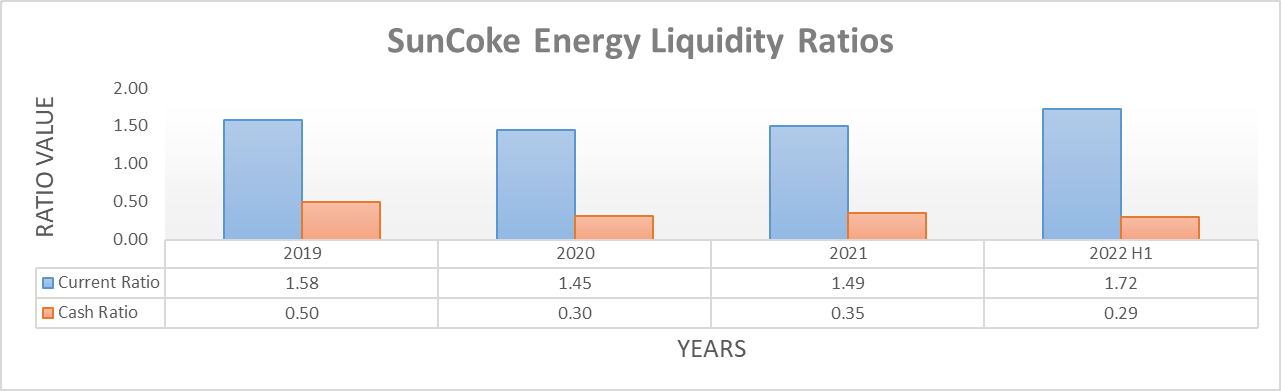

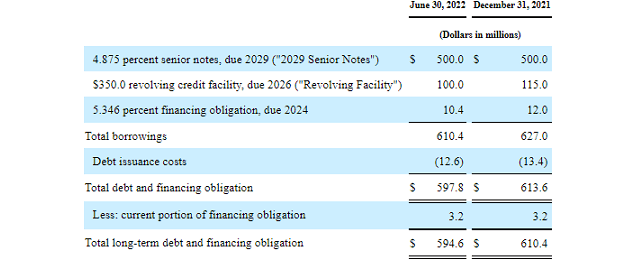

When moving onwards to their liquidity, it also saw improvements during the first half of 2022 with their current ratio increasing from 1.49 to 1.72 and whilst their cash ratio saw a small decrease from 0.35 to 0.29, it was immaterial in the grand scheme with their liquidity clearly remaining strong. They also carry an additional $250m of availability under their credit facility, which provides additional support if required. Meanwhile, the majority of their debt does not mature until 2029, which provides ample financial flexibility to reward their shareholders, as the table included below displays.

SunCoke Energy Q2 2022 10-Q

Conclusion

After starting the year disappointingly too focused on deleveraging despite already sporting low leverage, thankfully management ultimately seized upon their stronger financial performance to provide a big dividend increase with shareholders set to take home another one-third more than they were accustomed to receiving. Now that management seems intent on rewarding their shareholders more meaningfully, I believe that their forecast massive 20%+ free cash flow yield warrants upgrading my hold rating to a buy rating.

Notes: Unless specified otherwise, all figures in this article were taken from SunCoke Energy’s SEC Filings, all calculated figures were performed by the author.

Be the first to comment