kellyvandellen/iStock Editorial via Getty Images

Dear readers/subscribers,

In this article, I continue my recent pattern of looking at Asian companies and specifically Japanese, by looking at Subaru Corporation (OTCPK:FUJHY). The business, with roots back to 1917 and its founding in 1953, was known as Fuji Heavy Industries, changing its name in 2017.

This business has both automotive, aerospace, and military exposures – it’s a licensed manufacturer of Boeing (BA) and Lockheed (LMT) helicopters and airplanes, as well as a global development and manufacturing partner.

Let’s look at what Subaru offers.

Subaru Corporation – What the company does

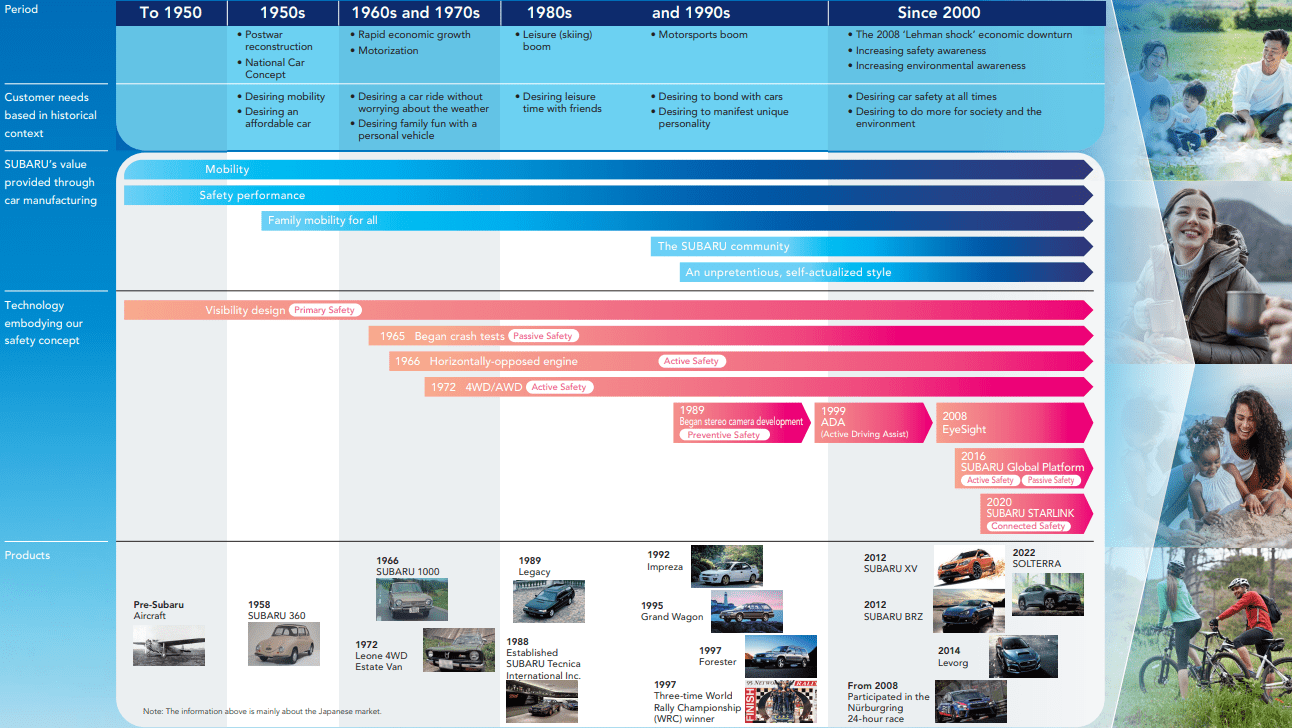

Subaru, or Fuji Heavy, traces its roots back to Nakajima Aircraft, which was the leading supplier of military planes to the government during WW2. It was broken up – like many of those businesses were after WW2, and was fully incorporated in -53, combining several former companies – Fuji Kogyo, Fuji Jidosha Kogyo, Omiya Fuji Kogyo, Utsunomiya Sharyo, and Tokyo Fuji Sangyo – into the largest transport manufacturer in Japan.

The company grew quickly, and by 1980, it was one of the largest suppliers of aerospace, railroad, and military equipment in Japan – but 80% of sales revenues came from cars. There was a crisis in the early ’90s and Fuji heavy had to essentially be “bailed out” by Nissan, before recovering.

Today, the Subaru corporation makes Subaru cars, and aerospace focuses on things like attack helicopters and utility products for the Japanese Army, as well as UAVs, components for Boeing jets, and for business jets.

Subaru has 94 affiliated companies with 2 automotive production sites, and 2 aerospace sites. Nearly 37,000 people work for Subaru, and the company has 440 automotive sales locations in Japan alone, with many more across 90 nations on the globe.

The company carries revenues of ¥ 2,744B, making an operating profit of that around ¥ 90B. This comes to a very low operating margin of 3.3%, but with a 53.4% equity ratio company-wide.

Subaru also comes with an A-rated credit.

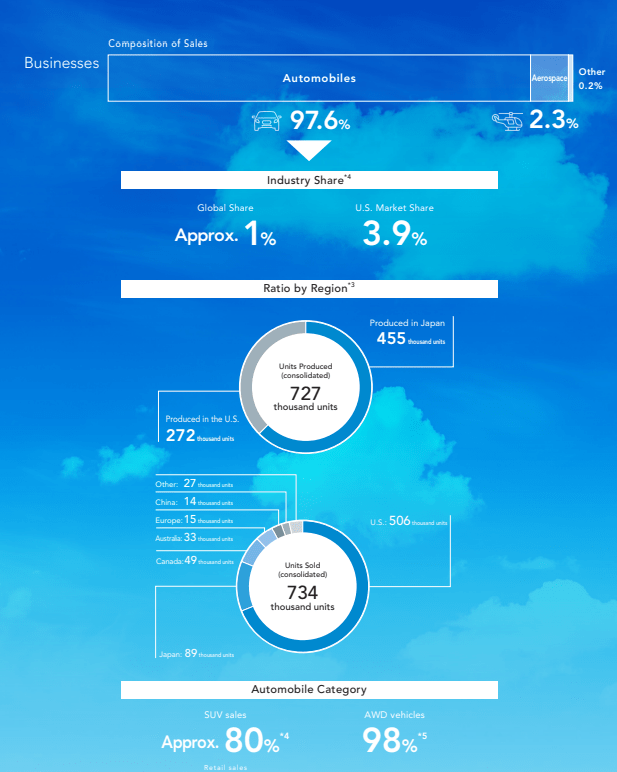

Subaru was 80% automotive in the 80’s – today it’s even more.

Subaru IR (Subaru IR)

What I consider when I think Subaru is “a great car”, but perhaps lagging the competition in terms of innovation, interior quality, and design as well as modern features. The sort of cars you use you live rurally, and need a quality, rugged SUV, or similar product – but not the car you typically go for as a first choice if you’re Joe everyman and looking for a new vehicle.

Still, Subaru has a very storied history of delivering safety as well as features to the market and is a major part of Japanese automobiles.

Subaru IR (Subaru IR)

The aforementioned railcar, utility and power, and industrial businesses no longer exist. They have been either transferred or discontinued. All that Subaru does today is Automotive and Aerospace.

In automobiles, the company’s focus is on SUVs, and its market focus outside of Japan is the USA. This makes sense because Subaru’s market share in Europe is barely worth mentioning. It was around 0.35%, which was actually a peak, back in -08, but has since dropped to below 0.3%. In Sweden, Subaru retail locations are usually co-existing with plenty of other brands that generate more interest.

As I said – there’s a specific set of customers that look for a Subaru – they have a reputation for rugged, utilitarian quality while compromising on design and features.

The best-selling model here has been the Forester AWD – again confirming this stereotype, and this model has actually shown relatively stable sales averaging around 12-16k units on an annual basis.

However, for Europe, the company’s sales have been looking even worse in 2022. It was less than 37 cars from selling less than 1,000 cars in a month in all of Europe back in July of 2022, selling 1,035, and it indeed even dropped to 777 cars sold back in April of 2020, during COVID-19. The 2020 sales numbers showed a 40.24% sales drop, and the company’s market share is now down to between 0.15% to 0.17%.

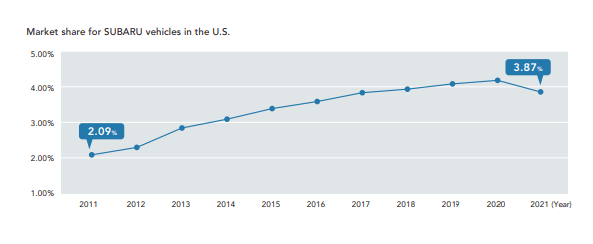

The USA is looking a lot better. The company has more than 22 times the European market share, coming to an impressive 4%+ in recent years. Subaru has actually been very successful in the USA in terms of growth, and in a single month, Subaru sells more than 5x the number of Cars than it does in an entire year in Europe.

So, the US focus makes sense outside of its home market of Japan. In fact, the USA is an even better market for the company than Japan is – where in 2021, Subaru sold 101,000 units, again less than 2-3 months in the USA. The best-selling car company in Japan is by far, with more than 2x to the second place, Toyota (TM).

So why is Subaru so successful in the states?

The company, after all, sold 5 times as many vehicles as in its home market, outperforming industry growth by a factor of 3-5x depending on the year. Subaru is small compared to other major automobiles, with a very limited product line with limited capacities.

So what gives?

Subaru IR (Subaru IR)

Well, Subaru managed to combine excellent marketing and focus on its values, which customers appreciate – a reputation for all-wheel-drive and safety, which all Subarus are reported to have. The key models were the Crosstrek, the Forester, and residual sales from the Outback. And, the company managed to get the pricing right.

The small crossover category was an excellent sales driver for Subaru as well, and models like the midsize Legacy Sedan also delivered sales, as well as the Impreza. The company’s products seem to be resonating with American customers.

Subaru spent resources trying to battle Toyota and Honda (HMC) – it could win neither battle, so instead it focused on what it knew – all-wheel drive and quality. This seemingly prevented Subaru from meeting the same fate as Saab, Suzuki, and Isuzu.

The USA is an impressive story for Subaru, and the company is leaning right into its customer interests, supporting organizations like ASPCA, International Mountain Bicycling Association, AIDS-fighting Dining Out For Life, and Sports Car Club of America.

Subaru IR (Subaru IR)

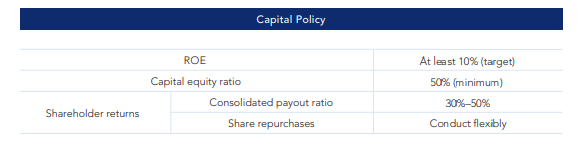

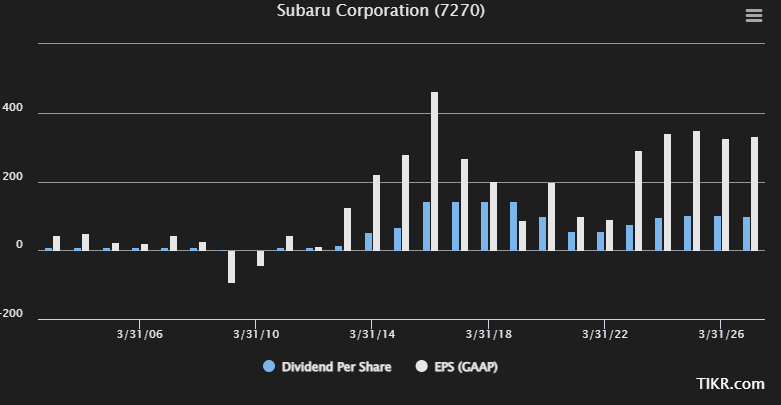

The company’s shareholder dividend has been an interesting story to follow – and it’s one that’s likely to improve for the next few years if you’re to believe the analysts forecasting the business.

Subaru EPS/Dividends (TIKR.com)

As you can see, recent results for the company have been positive – and 2022 will be a down year, but 2023 forecasts are significantly better. Other analysts’ forecast and the company’s quarterlies have been in line with these expectations.

Let’s take a closer look at the valuation trends for this mostly automotive business.

Subaru’s Valuation

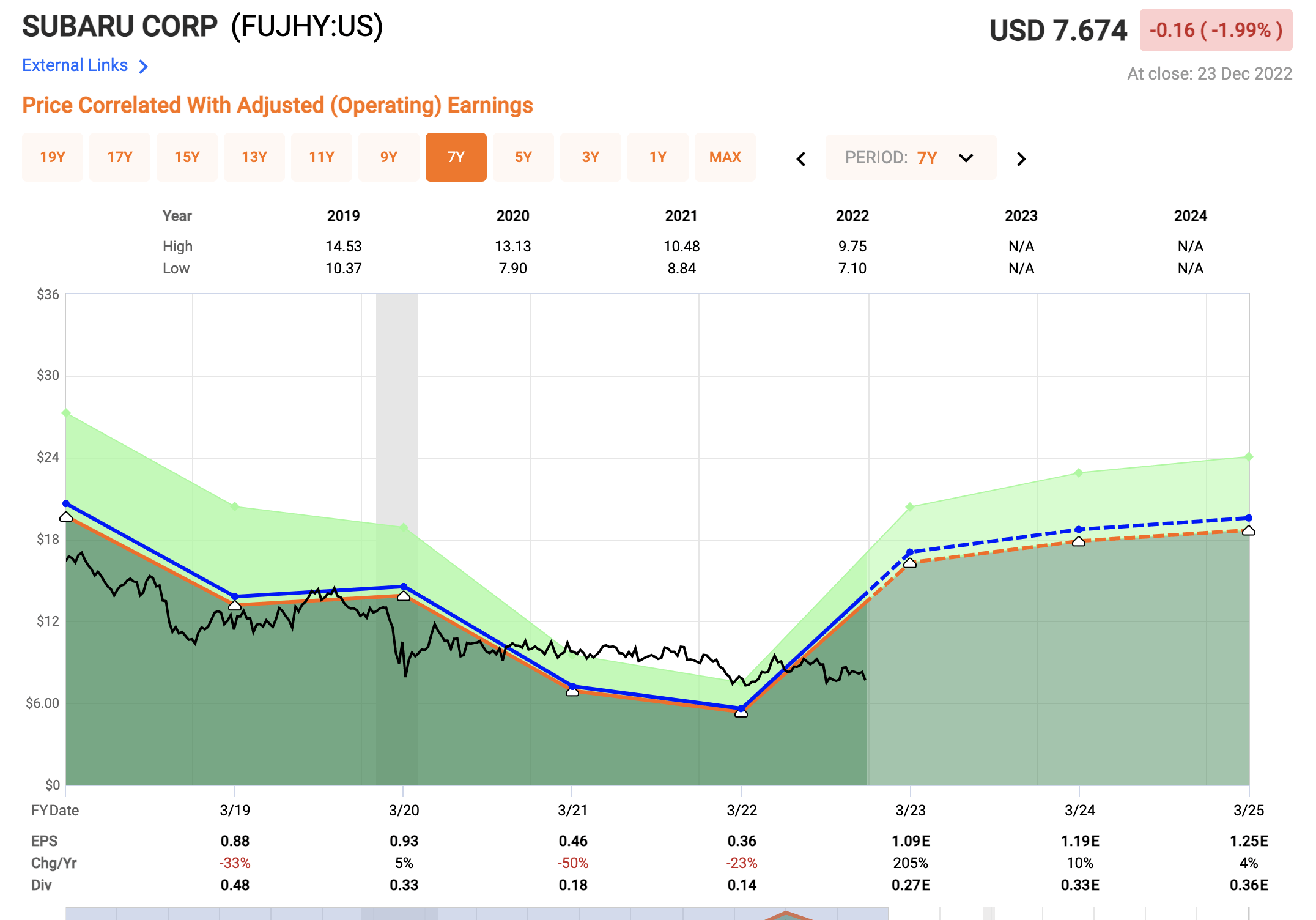

Subaru’s valuation is more representative of the past few years of results than it is representing the next few years of forecasts. The current forecasts call for the company, as you can see above, to improve its EPS significantly after 2022.

FactSet forecasts are very similar to the ones seen above.

Subaru valuation (FAST Graphs)

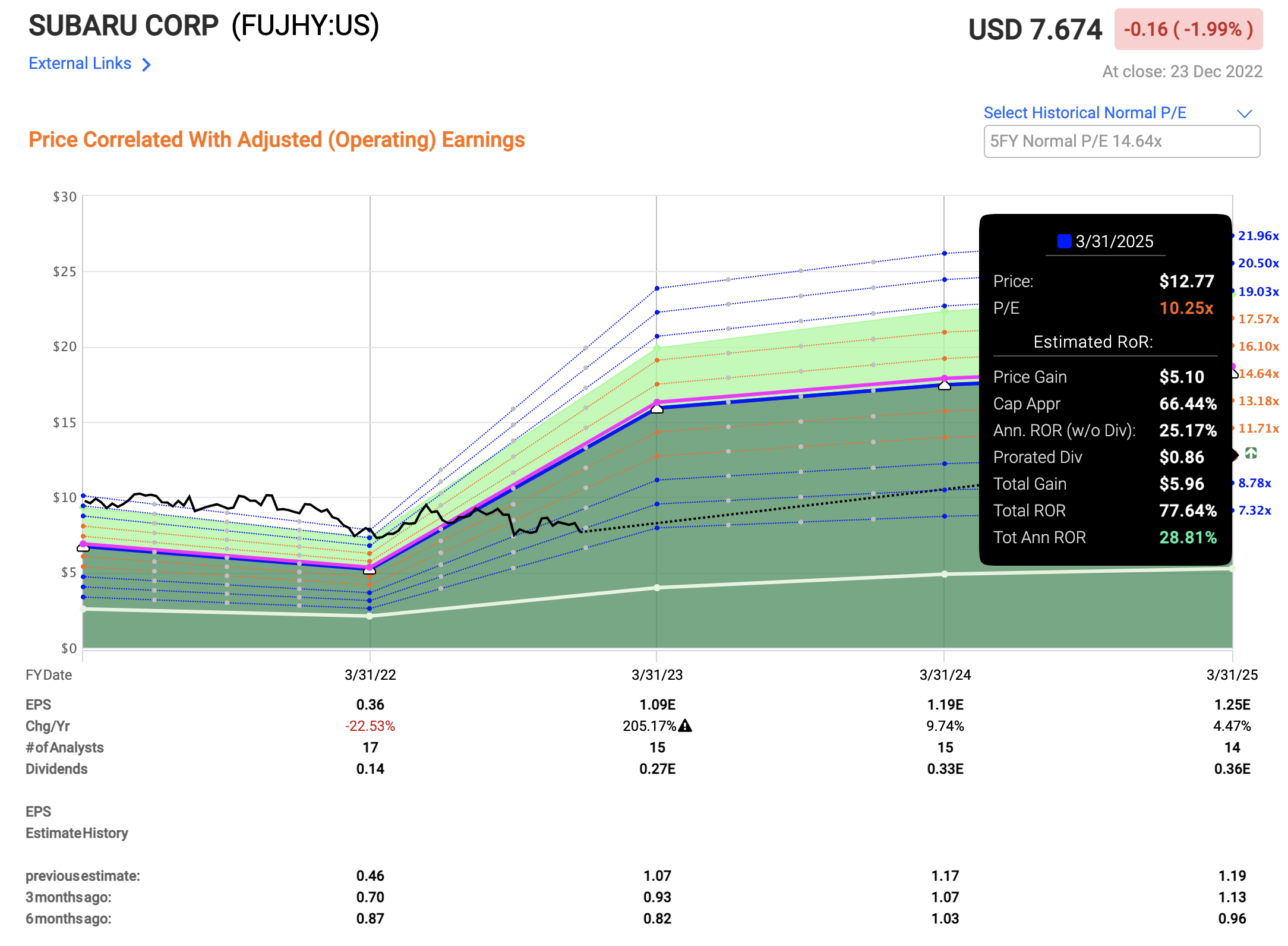

This trajectory means that we’re in exactly the right position to start heavily investing in Subaru. The company doesn’t yield much – 2% for the ADR currently, but that dividend is expected to increase, and you’re also investing in the company at a sub-9x P/E valuation for the ADR FUJHY.

The upside here is significant. Even if you only forecast the company at a 10x forward P/E, the potential RoR until 2025 is well into double digits.

Subaru Upside (FAST Graphs)

And it only goes upward from here. Based on average valuation ranges, Subaru as an investment could generate as much as 150% RoR in less than 3 years or 49.47% per year. So the theoretical upside here is massive if these earnings in any way materialize.

We want downside protection here – because the company’s forecasts are unstable and more than 40% of the time, with a 20% margin of error, the company doesn’t really manage it. Analysts weren’t able to forecast the depth of the drop Subaru has seen in EPS since 2016.

Eventually, things revert if the company in question has a solid base and solid foundations. I believe Subaru has this, and the time for that reversal has finally come. It may not be 200%+ as expected, but it will be significant, and I would expect the stock to reverse significantly in reaction to it.

Analyst targets confirm the overall significant upside to Subaru. 16 analysts follow the native 7270 ticker, which is the Japanese Subaru stock, trading at around ¥2,039 today. Ranges start at ¥2,000, and go up to ¥3,500 on the high end, with an average of ¥2,800. 8 analysts have moved to “BUY” or similar, which is up from less than 5 a year back. This target implies an upside for Subaru that’s almost 37%.

I go a bit more conservatively than this and would give Subaru a native PT of ¥2,500. I don’t really see any current fundamental risks that would cause a massive near-term deterioration – because sales numbers are fine, and the market looks fine.

That makes this company a “BUY” here.

The question becomes whether Subaru has dropped enough for the company to become appealing. My answer to this is that, yes, I believe it has. I don’t see any realistic downside in the company from this level, and for the long term.

The risk is perhaps that Subaru is a play on a volatile market – the US automotive market. Subaru is in favor at the moment, but it could drop again – and if the US market drops and Subaru’s market share drops, then we could see significant headwinds for this business.

However, I choose to follow the Bullish camp here and see Subaru as an attractive play.

Thesis

- Subaru is a USA-exposed automotive company with a small aerospace arm. It has fundamentally appealing products, perhaps suffering a bit from being behind some of its competitors, and having almost no market share in Europe. But overall, great products.

- The company has seen years of negative returns, reflecting a drop in earnings. However, this is expected to reverse in 2023 and forward.

- I give the company a native ¥2,500 PT, and an upside of at least 25% at today’s share price.

- Subaru is a “BUY” here.

Remember, I’m all about:

- Buying undervalued – even if that undervaluation is slight and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn’t go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

The company fulfills all of my investment criteria here – making it a “BUY”.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment