sompong_tom/iStock via Getty Images

Stryker (NYSE:SYK) is one of the leading medical technology companies globally. It is well-known for its Neurosurgical and Advanced Guidance Technologies which focus on providing high-performance instrumentation and computer-assisted surgery systems. In fact, its MedSurg and Neurotechnology segment finished FY’22 with 14.1% growth on a constant currency basis, outperforming the 13.3% and 11.6% growth rates recorded in FY’21 and FY’20, respectively, despite today’s challenging operating environment. SYK continued to grow through acquisition, which helped its growing top line. Lack of share repurchase catalysts in FY’23 and a declining free cash flow (FCF) conversion trend, however, make SYK’s short-term prospects unattractive.

Company Overview

SYK operates under two segments, its MedSurg and Neurotechnology and its Orthopedics and Spine. Both segments ended FY’22 with positive organic sales growth of 11.8% and 7.0%, respectively. Surprisingly, according to the management, despite today’s inflationary environment, demand environment remains strong, as quoted below.

Additionally, demand for our capital products remained very healthy in the quarter, as seen from the double-digit organic growth of our Medical, Endoscopy and Instruments divisions. Even considering our finish, we exited the year with a very strong order book. Source: Q4 2022 Earnings Call Transcript

Additionally, the company’s well known robotic-arm assisted system, MAKO, has a development update:

Finally, we are making good progress with the development of our Mako spine and shoulder applications, and expect to have the initial launch of spine in the back half of 2024 and the initial shoulder launch at the end of 2024. Source: Q4 2022 Earnings Call Transcript

This positions SYK well in the highly competitive Orthopedic Surgical Robots Market. Overall, MAKO has an outstanding performance this quarter and continues to win share in the market.

The great progress of our Mako offense has resulted in strong growth of our installed base alongside continued increases in utilization. In the U.S., we saw approximately 55% of knees and almost 30% of hips performed using Mako in the quarter. Source: Q4 2022 Earnings Call Transcript

The management’s focus on filling product gaps is a positive catalyst for the company as it demonstrates a commitment to meeting customer demands, staying competitive in the market, and driving long-term growth. In fact, management said that they are in talks regarding potential acquisition of a company that specializes in the hemorrhagic segment that can provide additional growth opportunities for Stryker and help it to expand its product offerings and capabilities.

We still think it’s a great market. There’s still a lot of patients that are — that have not been treated. We are only treating a small percentage of people that have these large vessel occlusions in the brain. So, we do think it’s a good long-term market. We are launching a new coil called Tetra Coil here in the United States, which is exciting.

And we will continue to invest. We have a deal that’s pending. Obviously, regulatory clearances before it closes on a one and done for the hemorrhagic segment. We are very excited about that. acquisition. That will give us another shot in the arm. Source: Q4 2022 Earnings Call Transcript

Analysts predict positive long-term revenue growth, however, SYK’s expanding inventory and tougher pricing environment, particularly in its Orthopedics and Spine business, represent a concern. In fact, due to rising input costs, the company had a worrying gross margin trend, as seen in the graphic below.

SYK: Slowing Gross Margin (Source: Data from SeekingAlpha. Prepared by the Author)

Disruption in Share buyback Catalyst

SYK’s inventory build-up is one of the factors contributing to its decreasing cash from operations of $2,624 million, down from $3,263 million in FY’21 and $3,277 million in FY’20. Further to that, given its limited liquidity, the management does not plan to purchase their own shares in FY’23, preferring to focus on deleveraging their balance sheet. This will disrupt its consistent trend of share repurchases, which has been ongoing for the past ten years. Unfortunately, this will not help SYK’s valuation much in the near term. Additionally, looking at its slowing adjusted free cash flow conversion of 61.8%, down from its 85.5% recorded in FY’21 and 99.8% in FY’20 post some concerns which should be monitored.

A Bit Risky In Today’s Level

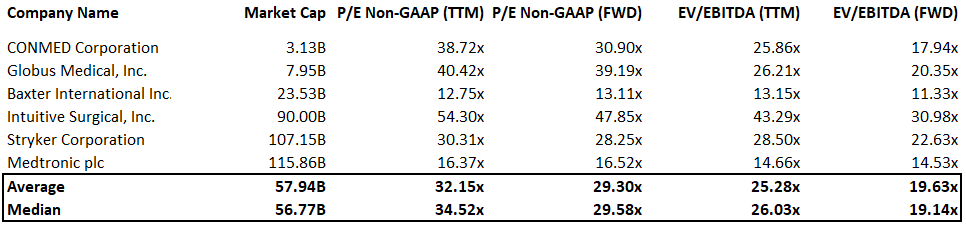

SYK: Relative Valuation (Source: Data from SeekingAlpha. Prepared by the Author)

CONMED Corporation (NYSE:CNMD), Globus Medical, Inc. (NYSE:GMED), Baxter International Inc. (NYSE:BAX), Intuitive Surgical, Inc. (NASDAQ:ISRG), Medtronic plc (NYSE:MDT)

Stryker appears to be overpriced at its present valuation, especially when comparing its trailing P/E of 30.31x to its 5-year P/E average of 27.07x. Furthermore, its projected P/E of 28.52x vs its peers’ forward P/E average of 29.30x does not represent a meaningful discount. This leads me to the conclusion that SYK is unappealing in the short run. However, in the long run, a forward P/E of 19.41x in FY’27 makes this company worth monitoring. In fact, SYK is trading at a higher trailing EV/EBITDA multiple of 28.50x than its 5-year average of 21.95x. Furthermore, the company’s forward EV/EBITDA of 22.63x trades unattractively compared to the peer average of 19.63x. Furthermore, based on the street’s average target price of $273.15, SYK appears to have no margin of safety, making it unattractive as of this writing.

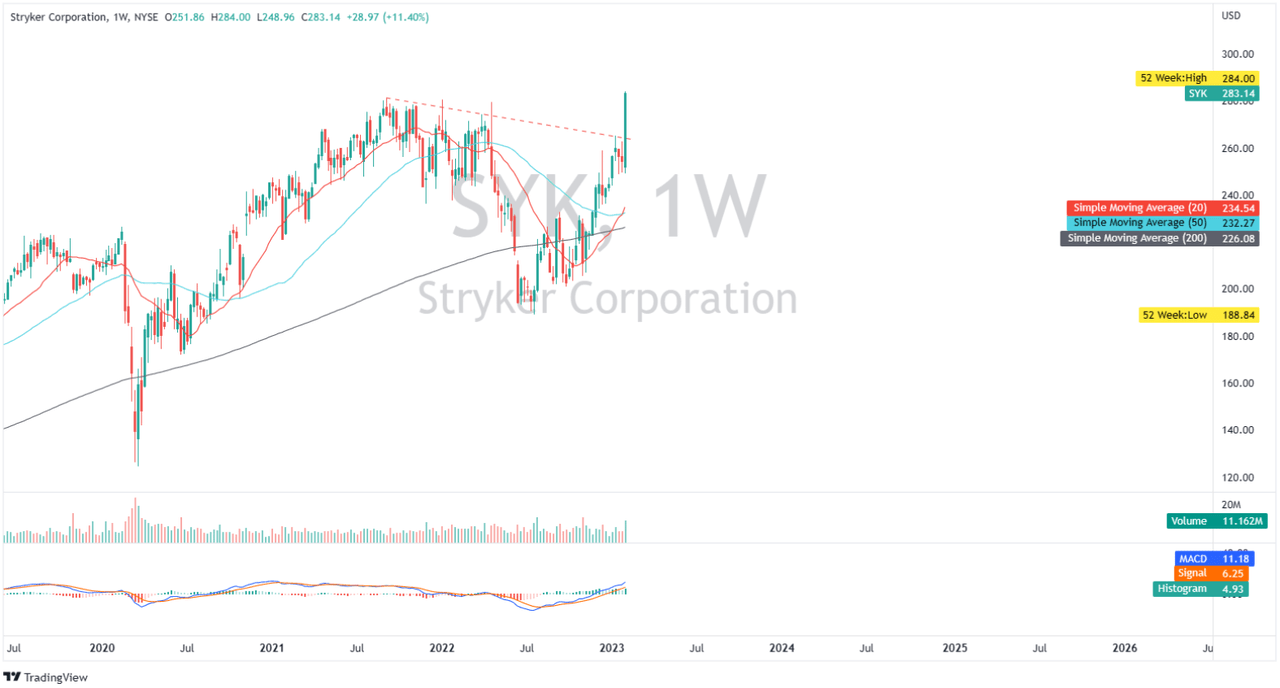

Breaking Out

SYK: Weekly Chart (Source: Author’s TradingView Account)

SYK recently broke its multi-month trendline, as shown in the chart above, and it is one of the few companies that manages to reach new highs in today’s bearish market. However, with its fundamental outlook, I believe the upside will be limited now. Hence, entering this breakout, in my opinion, is risky. Bullish signals from its 20-day and 50-day simple moving average bullish crossover, on the other hand, may induce the price to continue its bullish move towards $300 before it is exhausted. On the other hand, looking for a safer long entry, I usually wait for a pullback. This could be around $240 to $250, which I believe is the next logical support level. Its MACD indicator remains bullish above its signal line and above the zero line, supporting further price gains, but a potential bearish crossover, which would act as a confluence of price weakness, should be actively monitored.

Final Key Takeaway

A potential economic recession might put pressure on the recovery of procedural demand, thereby impacting demand for Stryker’s products. This might disrupt the company’s projected supply chain recovery, which the management is still confident about for 2023. But for now, I do not think you should worry about missing out and should wait for SYK to pivot from its declining profitability.

Thank you for reading and good luck!

Be the first to comment