HJBC

Investment Rationale

TechnipFMC’s stock soared in the past year, outperforming its peers. Growing shale gas extraction is expected to boost the growth of the oilfield services market. The company’s underwater solutions give it an edge over its peer companies in the subsea market. The company’s growing presence through new project wins in offshore renewable markets is creating more opportunities for its future growth. This makes FTI stock attractive for long term investment.

About the Company

Headquartered in Houston, Texas, TechnipFMC (NYSE:FTI) operates across two business segments: subsea and surface technologies. The subsea unit provides services to oil and gas companies associated with offshore exploration and production and contributes around 83% of the company’s revenue. The surface technologies segment designs and produces systems and provides services catering needs of oil and gas companies in land and shallow water exploration and production of crude oil and natural gas. About 17% of TechnipFMC’s revenue comes from its surface technologies segment.

Subsea 2.0 – A Competitive Edge

TechnipFMC holds a business moat through its product platform namely Subsea 2.0, which it introduced a few years ago. The company gets an edge as this platform helps in optimization of product performance and reduction of costs after installation. Majority of the company’s orders are for Subsea 2.0. TechnipFMC’s Subsea 2.0 is a configure-to-order model, which helps it in doubling its throughput capacity via its facilities. The platform consists of pre-engineered products with the flexibility to accommodate customer needs and functional requirements. Improvement in deep water production and exploration activities is likely to increase the size of subsea equipment market in coming years. In an improving market, TechnipFMC’s unique platform is likely to see higher customer demand.

TechnipFMC

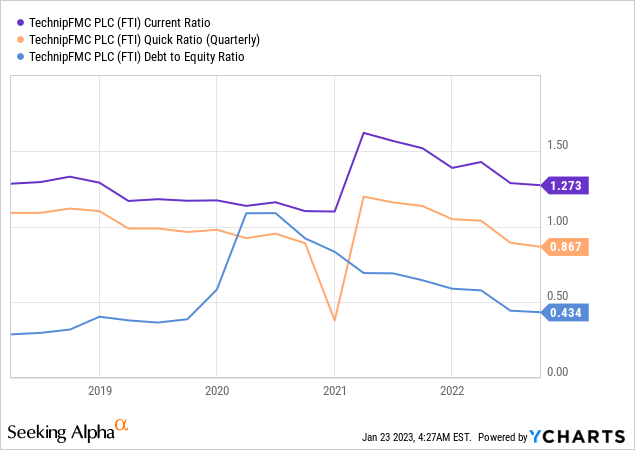

Comfortable Liquidity and Solvency Position

Healthy liquidity ratios like current ratio and quick ratio show TechnipFMC’s decent liquidity position indicating sufficient coverage for short-term liabilities. On the solvency front, a declining debt to equity ratio below 1 indicates lower risk. In 2021 and the reported three quarters of 2022, the interest coverage ratio is healthy.

Higher Inbound Orders Aided Strong Q32022 Results

In Q3, TechnipFMC reported a total company revenue of $1.7 billion, at par with Q22022. The recorded revenue was a major achievement amid the foreign exchange challenge posed during the quarter. Both the segments, subsea and surface, showed a sequential improvement in performance aided by project installation activity in Brazil and Guyana and higher international activity, including advancement in Middle East volume. The company recorded an attractive growth in inbound orders in both the segments along with a decent growth in backlog orders indicating higher demand.

TechnipFMC

Returning Value to Shareholders

Another highlight for Q32022 was authorization of a new share repurchase program allowing company to repurchase $400 million of its ordinary shares. During Q32022, TechnipFMC repurchased 5.8 million of ordinary shares for a total consideration of $50.1 million. The authorization of new repurchase program shows the company’s intent to return value to its shareholders through.

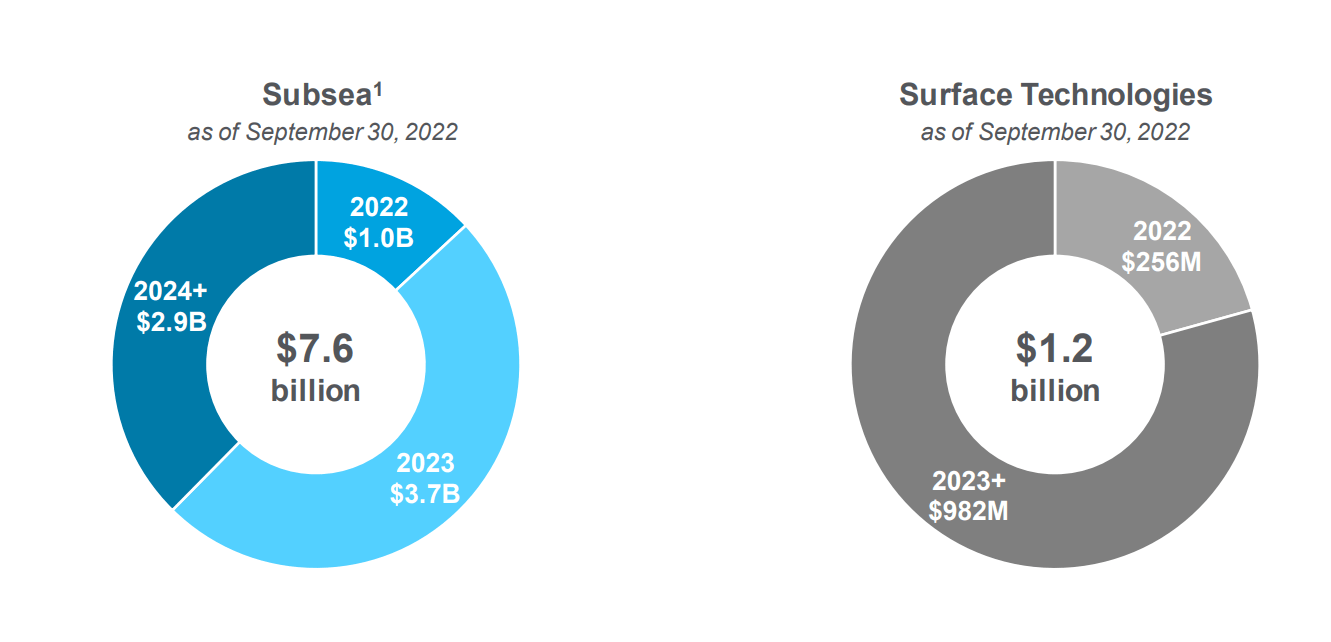

Scheduled Backlogs Providing Revenue Visibility

TechnipFMC calculates order backlog as the estimated sales value of unfilled, confirmed customer orders at the reporting date. The backlog shows prevailing expectations for the timing of project execution. Below pie charts illustrate the backlogs scheduled for 2022, 2023, and beyond 2024.

TechnipFMC

Due to the improved backlog of surface technology segment, the company expects an improvement in its international revenue in 2023. The company asserts that further investment in oil and gas resources would be enabled by offshore and subsea segments for the energy transition. This indicates a brighter outlook regarding future performance of both the segments of the company.

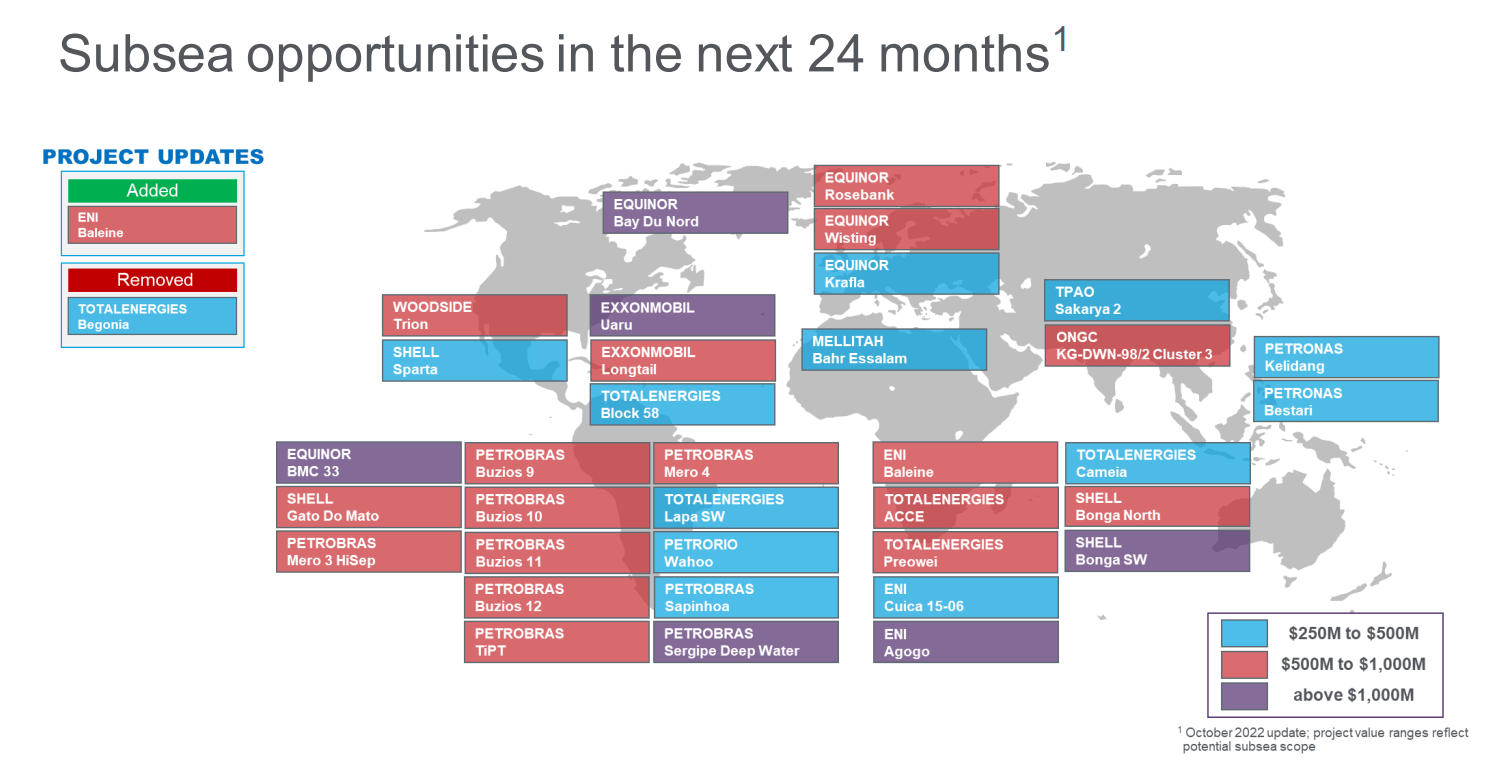

New Projects Fueling the Company’s Growth

Some of the notable projects which underpin the TechnipFMC’s future growth include-

- Procurement of 2 tidal energy contracts via partnership with Orbital Marine Power giving the company an edge in terms of floating tidal energy.

- Signing a lease agreement through its partnership, Magnora Offshore Wind, for installation of 33 floating wind turbines that can power more than 600,000 homes in UK.

- A contract awarded from TotalEnergies (TTE) for TechnipFMC’s Lapa Northeast field for reconfiguration and installation of umbilicals and flexible pipes in a new configuration that will further secure the production of the field.

The following image gives a brief overview of the prevailing opportunities in the Subsea segment for the company –

TechnipFMC

Attractive Valuation

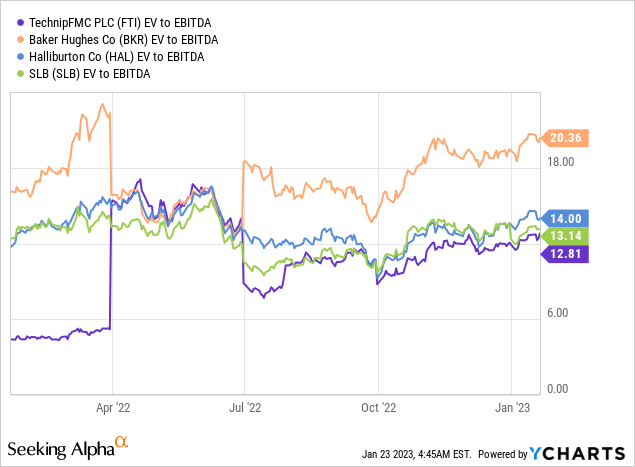

FTI stock has gained more than 100% in the past year outperforming its peer companies Baker Hughes (BKR), Halliburton (HAL), and Schlumberger (SLB). In terms of valuation, FTI stock appears to be undervalued based on EV to EBITDA ratio.

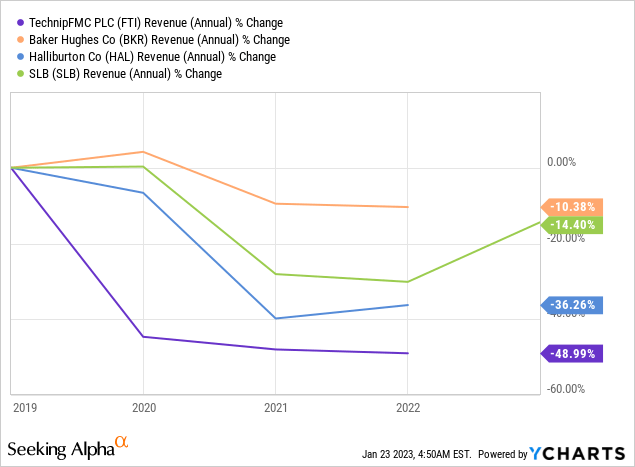

There are a couple of factors that explain TechnipFMC’s undervaluation. The company’s revenue growth has been negative and lower than its peer companies as shown in the graph below.

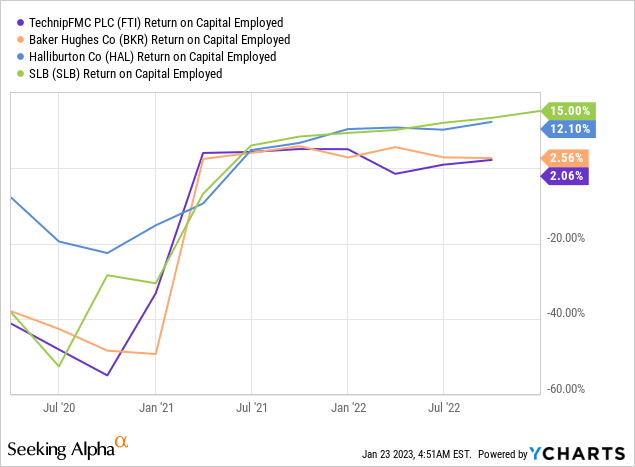

The company is offering comparatively lower returns on equity and capital employed than the returns offered by its peer companies.

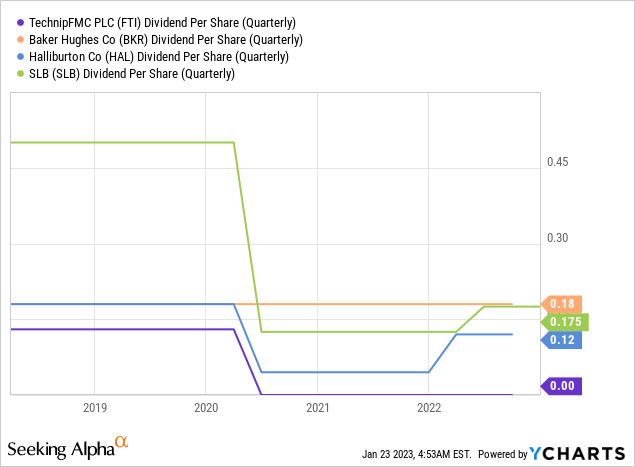

TechnipFMC is not paying dividends since Q22021, after it separated Technip Energies in February 2021 via a spin off. However, it has reaffirmed its commitment for a dividend and intends to start paying a dividend in the second half of 2023.

The company’s growth, its share repurchase plan, intention to initiate dividend payments, and a positive outlook for the demand for oilfield services hint towards a positive outlook for the stock.

Seeking Alpha’s proprietary Quant Ratings rate TechnipFMC as “hold.” The stock is rated high on the momentum factor, but low on the valuation factor.

Conclusion

TechnipFMC has 83% of its business through subsea equipment segment. It is decently positioned to benefit from the positive impact that the subsea equipment industry will have due to a growing number of maturing onshore oilfields. Also, the company’s unique Subsea 2.0 platform and configuration-to-order model will help in achieving further reduction of engineering costs for new projects of the company. FTI stock is relatively undervalued among peers and is also performing well in the equity market. Also, the company’s fundamentals look comfortable and growing, which makes FTI stock attractive for long term investment.

Be the first to comment