Michael Ver Sprill

If you have been looking for that Santa Claus rally, you may be disappointed. The latest data from the Federal Reserve shows that the Fed’s balance sheet contraction continues while the reverse repurchase – REPO – facility usage climbs heading into year-end. The combination of quantitative tightening and the use of the reverse repo facility has sent reserve balances back toward the year’s low and is likely to fall further this week.

Falling reserve balances and rising rates could send stocks sharply lower for the final trading week of the year.

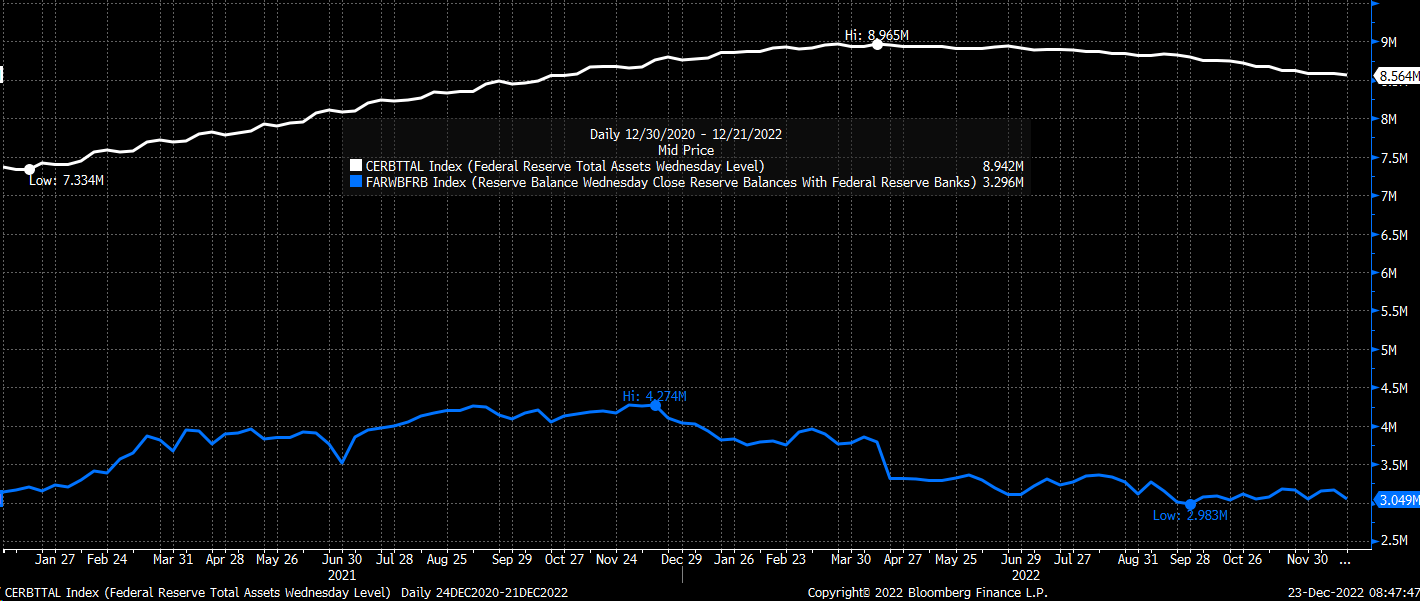

Reserves Have Been Falling

For the week ending December 22, the Fed’s total balance sheet fell to $8.56 trillion this past week, and its reserve balances fell to $3.05 trillion, just slightly higher than the $2.98 trillion low on September 28.

Bloomberg

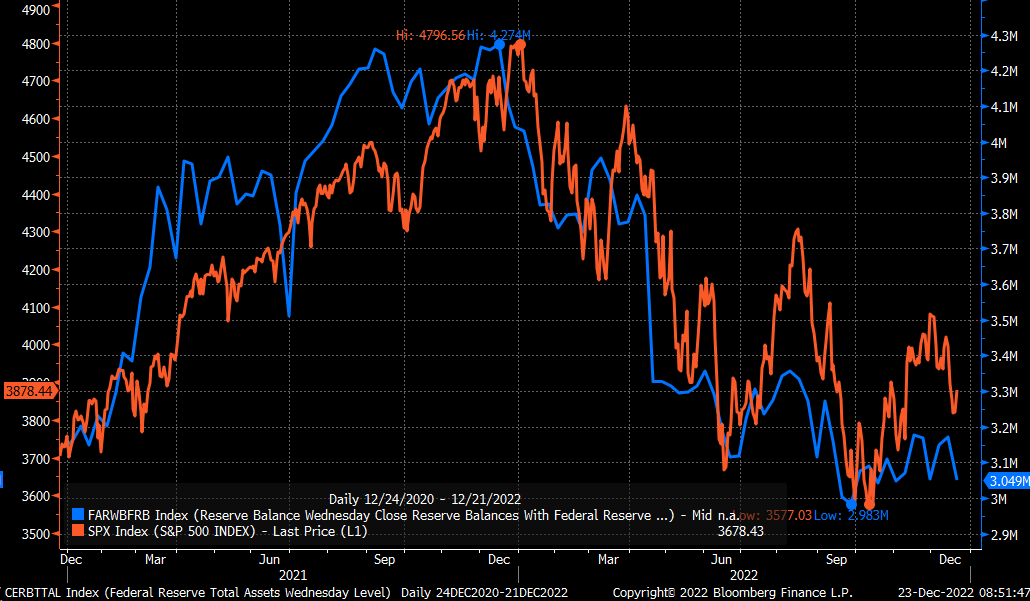

Changes in reserve balances have a positive and negative impact on the stock market as liquidity enters and exits. Part of the reason the S&P 500 has stagnated and been range-bound since the October low is primarily due to reserve balances that have been range-bound.

Bloomberg

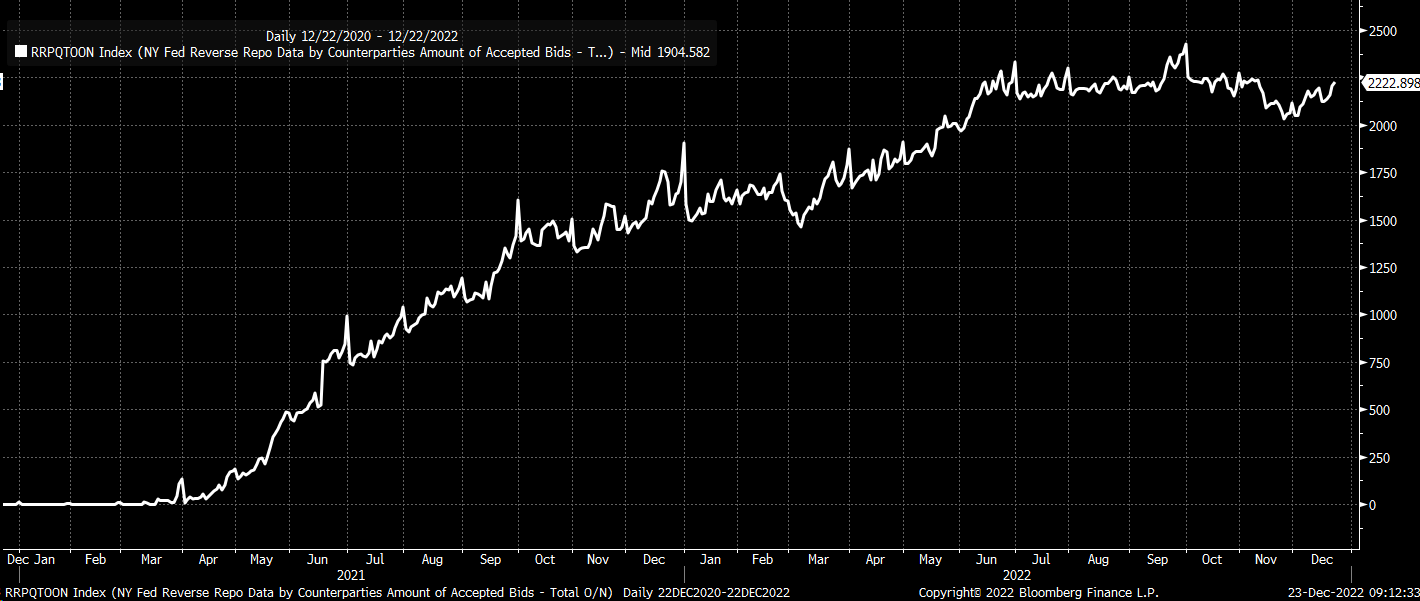

Heading into year-end, we will likely see the reverse repo facility usage increase, as it has been doing in recent days. How high the facility usage goes will partially determine how low the reserve balances fall and how much liquidity is drained out of the equity market over the rest of this week.

Bloomberg

Reserve balances are published using Wednesday’s ending value, and as of December 21, reverse repurchase agreements were at $2.206 trillion. If that number should continue to rise as we head into year-end, it should result in reserve balances falling further, draining more liquidity from the market over the next week.

Historically, there’s a spike in facility usage heading into the quarter’s final day. In December 2021, the use surged to a new high; if we see a higher at the facility again this year, then it could result in the facility rising to the levels seen in September, just shy of $2.4 trillion or higher.

A push that high in the repo facility could result in the reserve balances dropping below $3 trillion this week, which would be a substantial form of stress on the S&P 500 and the equity market.

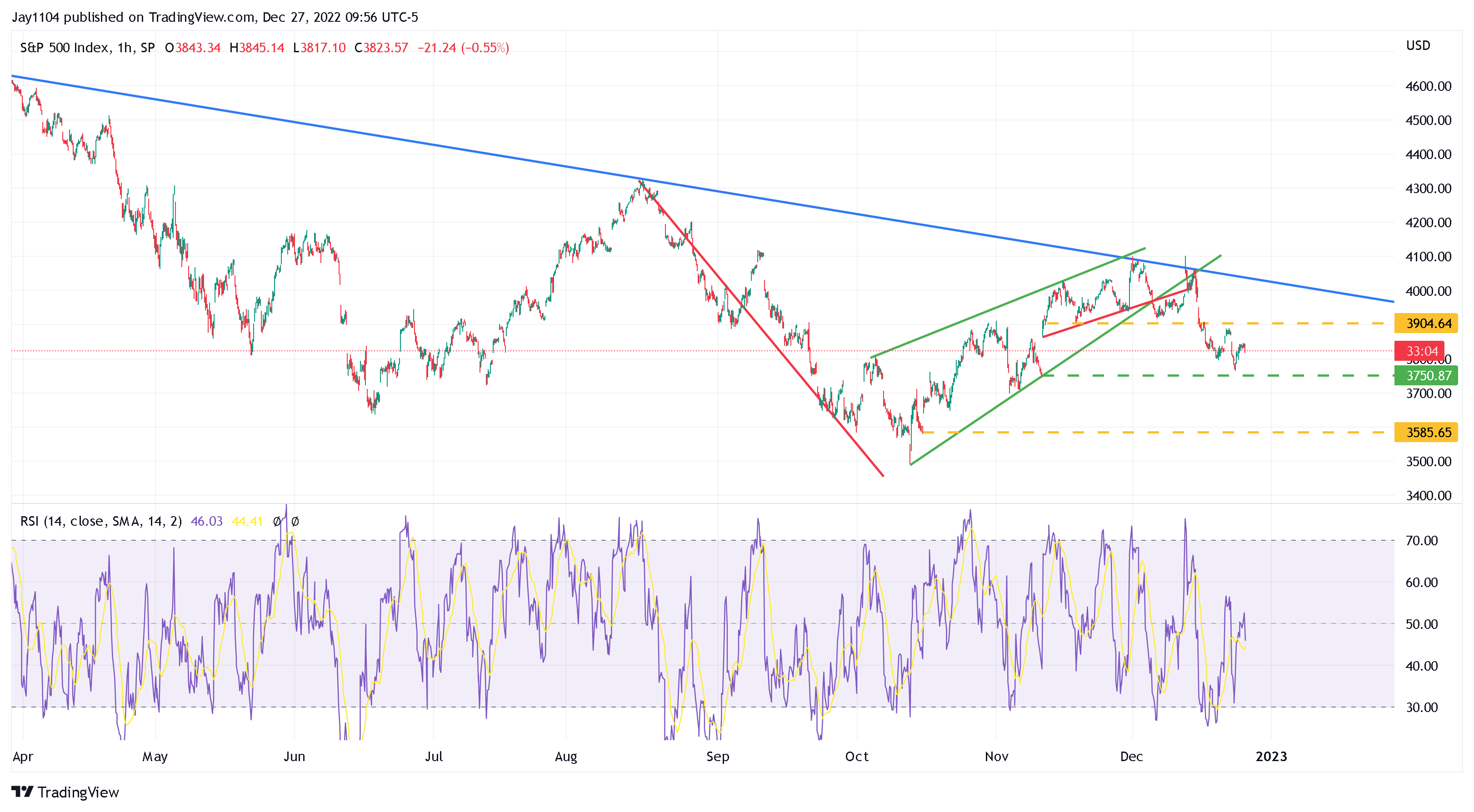

Technical Trends Shift

But more important, the technical trends in the S&P 500 remain bearish since the completion of a rising wedge pattern following the December FOMC meeting. This has put support at 3,750 in play already once last week, and if tested again this week, that support is likely to break, opening a path to around 3,580, and pushing the index back to the lows seen in October.

TradingView

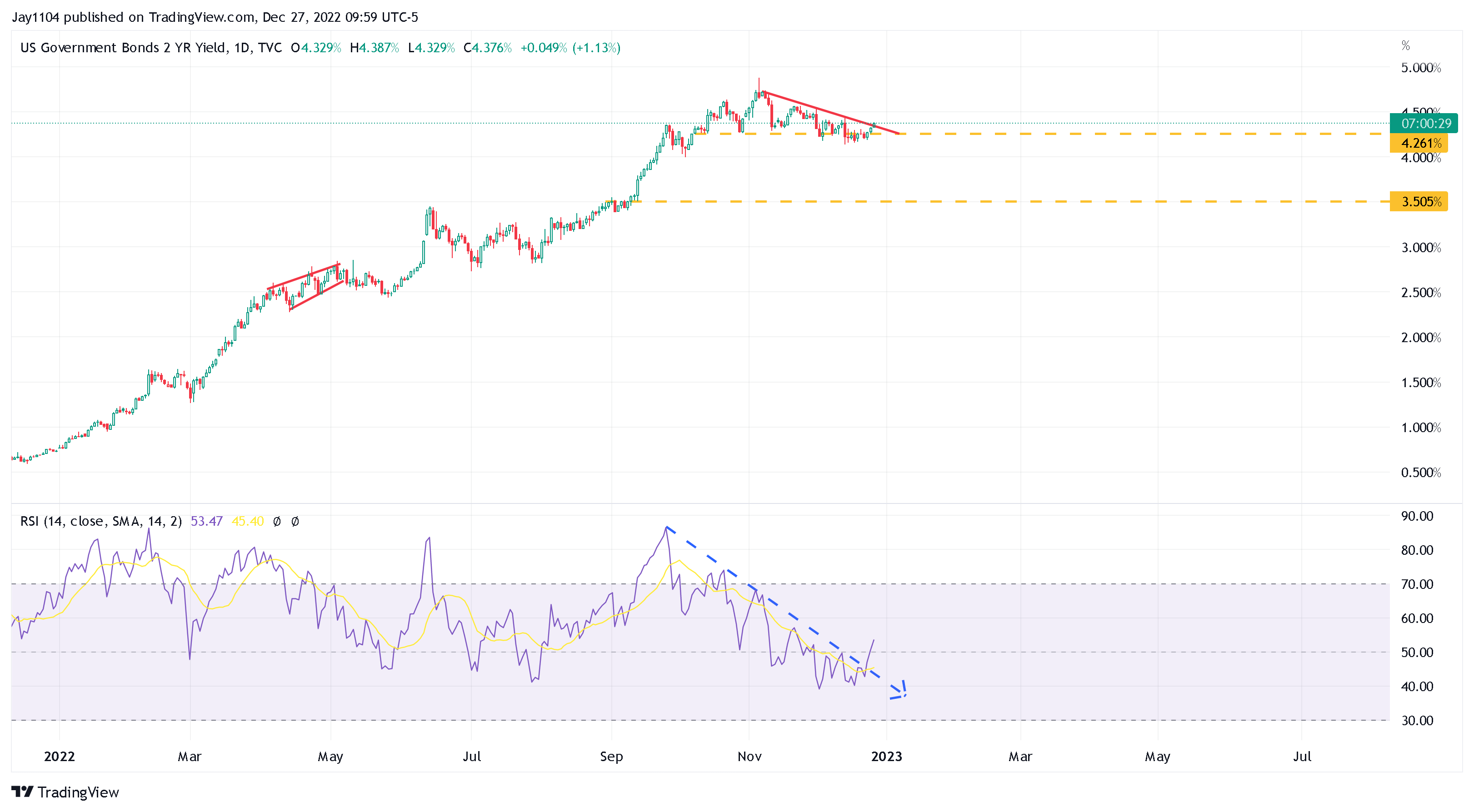

Additionally, adding to the declines in the S&P 500 will be rising rates, with the US 2-year rate now breaking out of a consolidation pattern and the potential to push significantly higher in the coming weeks and potentially back to its highs around 4.9% seen on November 4. Additionally, the relative strength index is also breaking above a downtrend, suggesting a change in trend from falling rates to rising rates.

TradingView

If rates continue to push higher and liquidity is sucked out of the market this week heading into year-end. Then the stock market will probably have a rough final week of trading in 2022, which is not much different than what was witnessed the entire year.

Be the first to comment