Daniel Balakov

Some of my followers already know that I am a technologist, scientist, water lover, and a believer in sustainable and environmentally responsible investing. I have also been around long enough to know that not everyone embraces those ideals, and not all businesses believe in ESG (environmental, social, governance) sustainability goals. Some of those goals include things like clean water and sanitation; sustainable cities and communities; industry innovation and resilient infrastructure; affordable and clean energy. It also includes good governance, which requires prudent management skills and effective risk management.

It has been demonstrated that stocks of companies that do adhere to ESG concepts tend to outperform with lower market risk than those which do not. This story from Forbes offers one example.

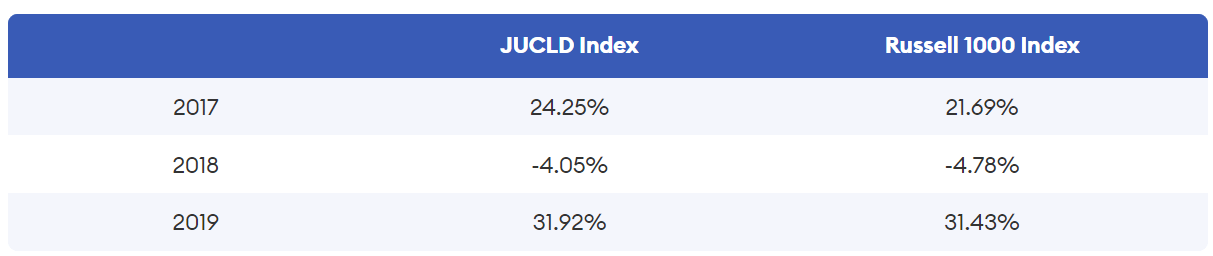

Take JUST Capital’s JUST U.S. Large Cap Diversified Index (JULCD), an index that tracks the performance of large, public companies with high ESG scores. It includes 50% of the large-cap public companies in the Russell 1000 index but excludes companies that lack a demonstrated commitment to things like the well-being of their employees, beneficial products, positive environment performance and strong communities.

JUST Capital’s JULCD index outperformed the Russell 1000 for three years in a row by at least a slim margin:

Forbes

So, when I come across a successful, innovative, and growing construction and infrastructure company like Sterling Infrastructure (NASDAQ:STRL), I am inclined to dig a little deeper into the company and its stock offering. I believe that STRL is a Buy given their recent business transformation and focus on ESG and Sustainability in their business practices.

In his recent post, long-term investor and Chairman of GMO, Jeremy Grantham, states that sustainability is going to be a growing concern over the next 5+ years:

For those with a longer horizon than average, say 5 years and above, I believe stocks related to addressing the problems of climate change and the increasing pressure on many raw materials have a substantial advantage over the rest of the economy as the world’s governments and corporations begin to accept the urgency of these problems, like the U.S. government did so emphatically with the Inflation Reduction Act.

Sterling recently published a 2022 Sustainability report that describes the Sterling Way – the way they conduct business and help to “build a better tomorrow”. The message from CEO, Joe Cutillo states:

Sterling has always been environmentally and socially conscientious. This report simply reinforces how everyone in the company and our subsidiaries, from the field to executive management to the Board, champions the cause of sustainability, Environmental-Social-Governance (ESG), and meaningful corporate responsibility. Each are critical to the way we conduct business. Therefore, taking the initiative to protect the environment, celebrate diversity, and perform ethically and transparently through strong governance are just some of the ways The Sterling Way informs everything we do.

According to a report from Deloitte, the 2023 outlook for the engineering and construction industry is for differentiated growth rates across industry segments and competitive pressures based on current market dynamics including inflation and ongoing supply chain issues. They identify five trends that companies will need to successfully compete. And one of those five trends is ESG and Sustainability.

Many customers are becoming more sustainability conscious and placing greater pressure on developers to lower the carbon footprint of new construction. The increasing global focus on climate change could incentivize construction companies to factor sustainability into their projects, construction processes, and designs.

About Sterling

Sterling is a market-leading provider of infrastructure services including transportation, building, and e-infrastructure solutions. They offer a diversified portfolio of services and end markets, especially in the Southern and Southwestern US, Rocky Mountains, Nevada, California, and Hawaii, with more recent expansion into the Southeast and Northeast by way of acquisitions.

Originally founded by two brothers in 1955 as the Oakhurst Company, Inc., they went public in 2001 as Sterling Construction Company, Inc. The company’s success according to the company website, is based on:

“… a platform to support strong growth via a mix of recurring and new project revenues, and continued execution and sustainability of the growth strategy which includes solidifying the existing client base, growing margin products, and expanding into adjacent markets while maintaining recurring revenues.”

Sterling has a strong management team, headed up by CEO Joseph Cutillo, that has established good cash flows and a solid balance sheet, efficient return on invested capital, and successful M&A transactions. From the company website, the recent name change from Sterling Construction to Sterling Infrastructure is explained thusly:

In 2015, we committed to transforming our organization from a business that was 95% Heavy Civil to a results-driven, growth-minded efficient machine.

After a series of M&A transactions, there are now a total of 7 subsidiary companies. The company service offerings are now divided into 3 categories.

E-infrastructure Solutions includes specialty services projects such as advanced, large-scale site development systems & services for data centers, e-commerce distribution centers, commercial, warehousing, transportation, energy, and more.

Building Solutions includes residential and commercial concrete foundations for single-family and multi-family homes, parking structures, elevated slabs, and other concrete work.

Transportation Solutions includes Heavy Civil infrastructure and rehabilitation projects for highways, roads, bridges, airports, ports, light rail, water, wastewater, and storm drainage systems.

Now based in The Woodlands, TX, Sterling made the Forbes 2023 Best Small Companies in America list. In more exciting news for the company and the stock, STRL was named a 2023 Barron’s Roundtable Stock pick.

Mergers and Acquisitions

In 2007 the company acquired Road and Highway Builders, LLC. Then, in 2009 they acquired Ralph L. Wadsworth and were named a Top 200 Contractor in the US by ENR. Banicki Construction joined the STRL family in 2011. In 2017 they acquired Tealstone Commercial and Residential Concrete based in the Dallas-Ft. Worth area. Plateau Excavation was the next acquisition target in 2019. Then in 2021 they acquired Petillo, a site development solution provider, expanding their geographic footprint to the Northeast and Mid-Atlantic, and Kimes & Stone, a soil stabilization business in the Southeast. In 2022 they rebranded as Sterling Infrastructure.

Sterling completed another new acquisition in December 2022, when they announced the purchase of a concrete company in Arizona for $22M. The company, Concrete Construction Services, or CCS, brought in annual revenues of about $70M prior to the acquisition.

“CCS provides residential single-family home concrete foundations, including the preparation, pouring and finishing of post-tension concrete foundations in new housing subdivisions in the Greater Phoenix area.”

Stock Performance

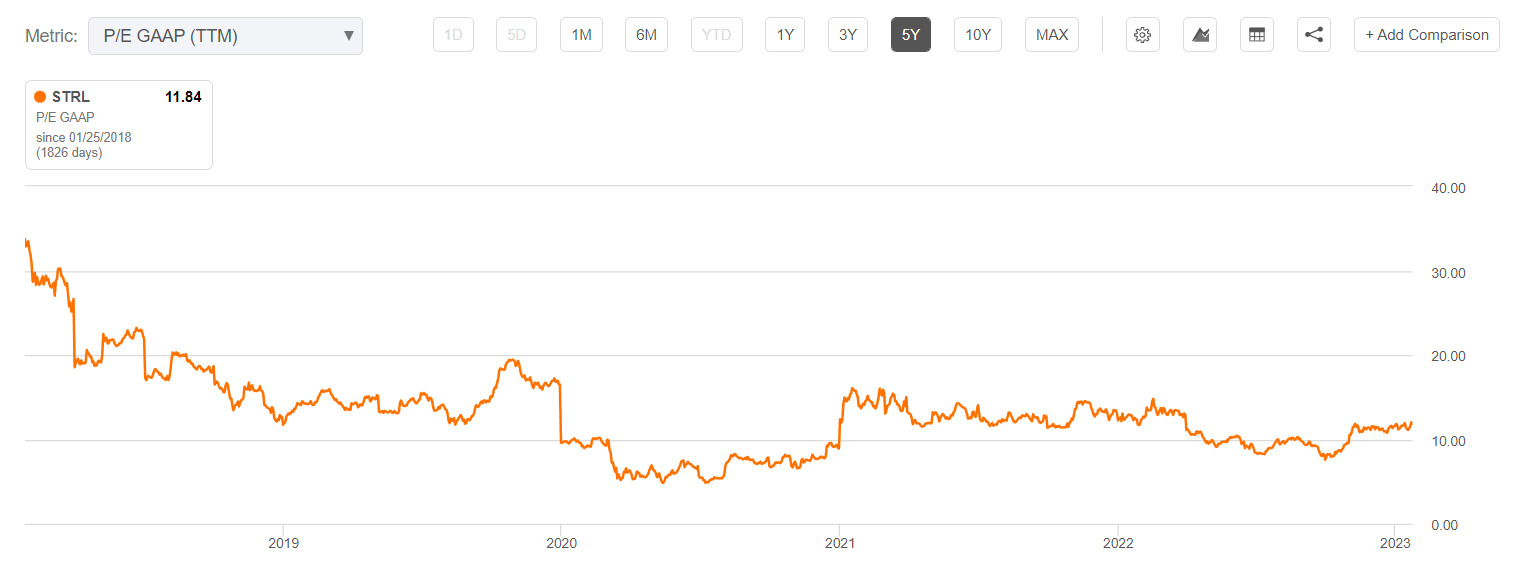

The STRL stock has performed very well over the past few years, yet still trades at an attractive valuation at just 10x forward earnings. With a current TTM P/E of about 12, the stock is trading below its 5-year average of about 16x, although it did trade even lower in 2020.

Seeking Alpha

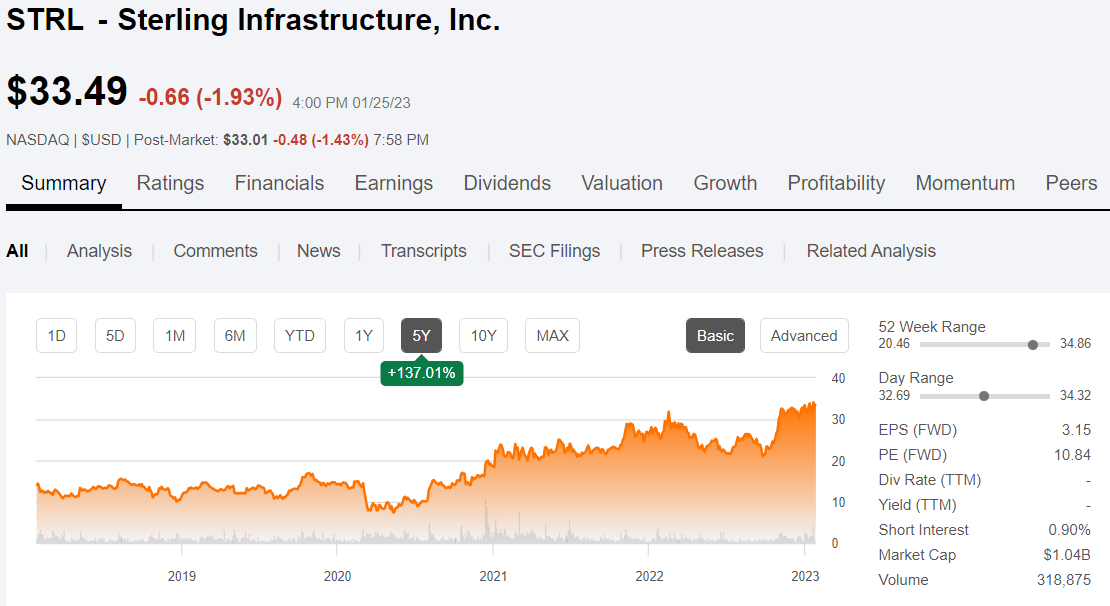

With a five-year price return of more than 137%, the stock is still trending higher as we approach the company’s 4th quarter 2022 earnings report.

Seeking Alpha

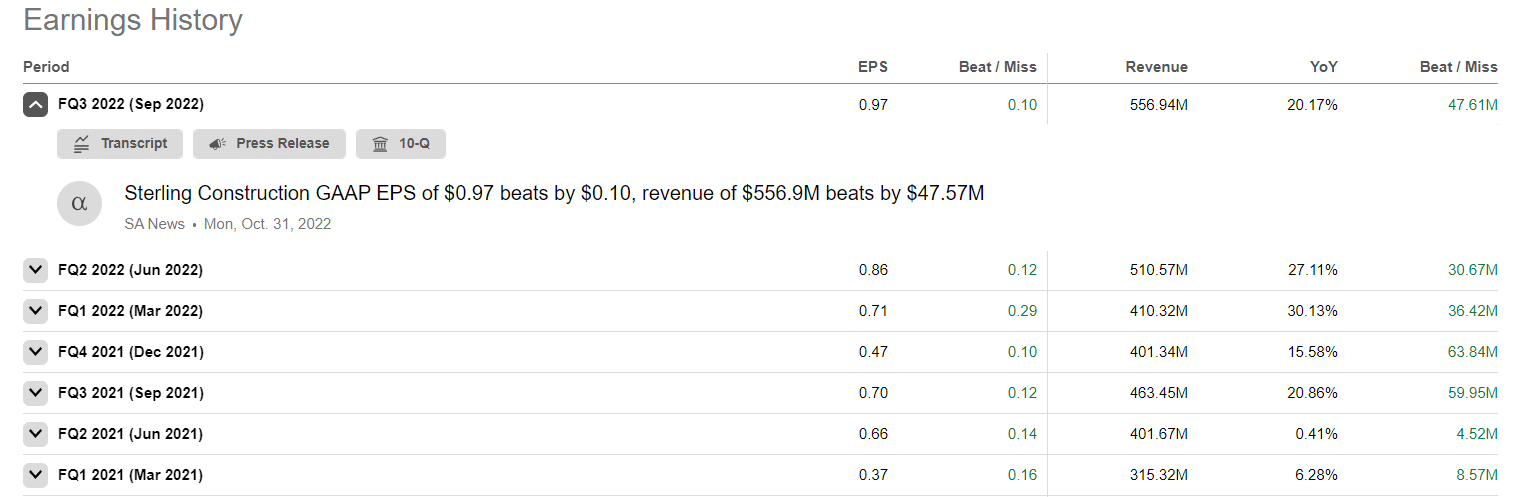

Looking at the last 2 years earnings reports, the revenues and earnings have been consistently beating estimates for at least 7 quarters in a row according to SA.

Seeking Alpha

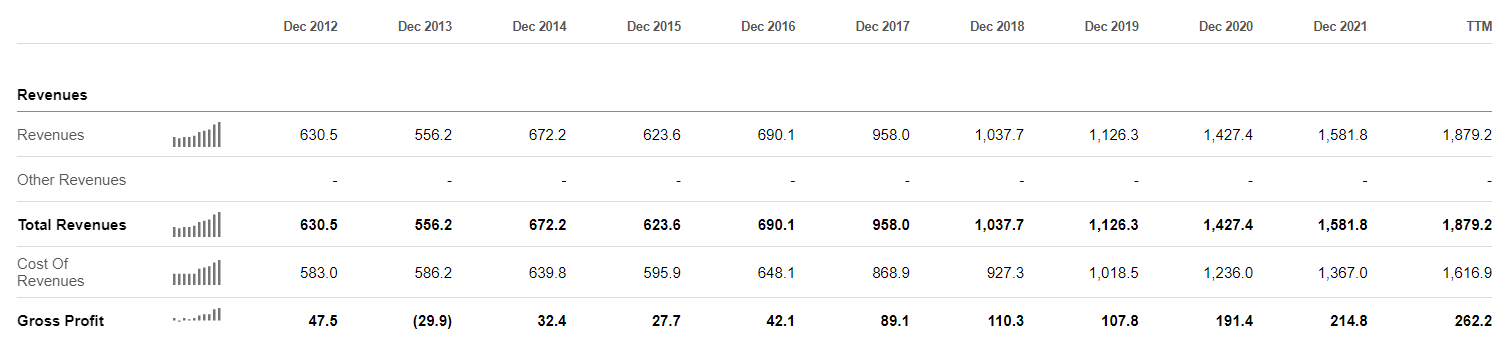

And by reviewing the balance sheet, it is quite evident that revenues and gross profits have been steadily growing, especially since 2015.

Seeking Alpha

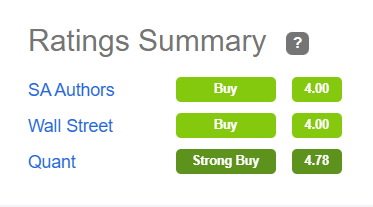

STRL is rated a Buy by SA Authors and Wall Street analysts and gets a Strong Buy rating from the SA Quant ratings.

Seeking Alpha

Recent Earnings Results and Contract Awards

On October 31, 2022, STRL reported Q322 earnings results that were very good in light of the broader economic malaise that was affecting most of the US in the summer and fall of 2022. The company press release highlighted the Q3 results:

- Total Revenue of $556.9 million, an increase of 20% compared to the third quarter of 2021

- Net Income was $29.5 million, or $0.97 per diluted share, an increase of 40% and 35%, respectively, compared to the third quarter of 2021

- EBITDA of $60.2 million, an increase of 50% compared to the third quarter of 2021

- Cash flows from operations was $96.1 million and $130.6 million for the third quarter and nine months ended September 30, 2022, respectively

- Cash and Cash Equivalents totaled $146.5 million at September 30, 2022

- Backlog at September 30, 2022 was $1.67 billion, an increase of 12% over December 31, 2021

- Combined backlog at September 30, 2022 was $1.90 billion, an increase of 25% over December 31, 2021

Since that time and after the end of the third quarter, several new contract awards have been announced. Those awards include:

- Sterling was awarded a $45M site development contract for the new Rivian (RIVN) EV facility in Georgia.

- A $20M IDIQ contract with US Customs Border Protection for critical infrastructure.

- A $45M award to the Ralph Wadsworth Construction company for airport redevelopment at Salt Lake City airport.

- Another $34M in contract awards for 2 new projects with the Idaho Transportation Department for infrastructure improvements.

Another recent bit of news included the divestiture of 50% of another construction company, Myers & Sons Construction, for $18M in cash. According to the press release:

The Company expects to present the operating results of Myers as discontinued operations in the fourth quarter of 2022 and anticipates recognizing an after-tax gain of $11 to $13 million on the disposition, primarily due to an extinguishment of a $15 million liability for members’ interest subject to mandatory redemption, partly offset by a $2 to $4 million loss on the sale of the Company’s 50% ownership interest.

Furthermore, and prior to reporting Q3 results, the company announced new E-Infrastructure awards totaling $309 million for the 3rd quarter.

“We continue to see strong demand in our E-Infrastructure Solutions segment and set a new booking record for the quarter,” stated Joe Cutillo, Sterling’s CEO. “Demand for large warehouses, data centers and e-commerce distribution centers were once again the top three categories. Additionally, our recently announced Rivian award, which will be added to backlog in the fourth quarter, illustrates the evolving incremental industrial opportunities which we believe will continue throughout 2023.”

Conclusion and Recommendations

Whether or not you are a fan of ESG initiatives and environmentally responsible investing, those market drivers are in place in the engineering and construction industry in 2023. And Sterling Infrastructure has been transforming its business to accommodate those needs and to grow their business successfully by implementing what they refer to as the Sterling Way, as explained in this message from CEO Joe Cutillo:

As infrastructure evolves and the industry becomes more diversified, we recognize more and more how our endeavors impact not only the environment but also society as a whole. This is why The Sterling Way, the way we conduct business, is now more important than ever. It reinforces our commitment to protecting and caring for our people, communities, customers, and investors.

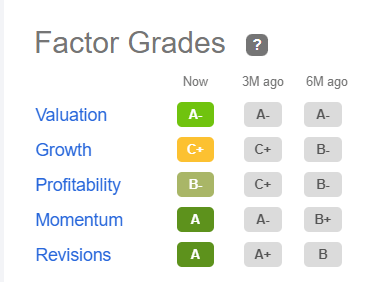

Recent contract awards and successful integration of newly acquired companies speak to the success of that initiative. The SA quant factor grades show A and B grades in most categories with a C in the Growth category.

Seeking Alpha

I would not be surprised to see the Growth grade improve to something better as we get further into 2023 and the revenues from recent contracts begin to be recognized, and as the US economy continues to recover from post-pandemic inflation and supply chain issues, and as Federal funding from the Infrastructure Bill starts to flow to the States. In fact, on the Q3 earnings call CEO Cutillo addressed the company’s growth prospects and is especially enthused about the E-Infrastructure segment:

E-Infrastructure, which remains our largest segment and represented 46% of our revenue and 66% of our segment operating income in the quarter, saw record bookings as data center, distribution center and warehouse demand remained high. In addition, we began seeing the first wave of onshoring a new manufacturing facility activity take place. A recent win of the new 500 acre plus Rivian Electric Vehicle plant in Georgia is yet another example of our ability to do large complex jobs in almost any end market. This new manufacturing activity, along with the continued strong demand for data centers and e-commerce warehouses continues to give us a positive outlook for 2023.

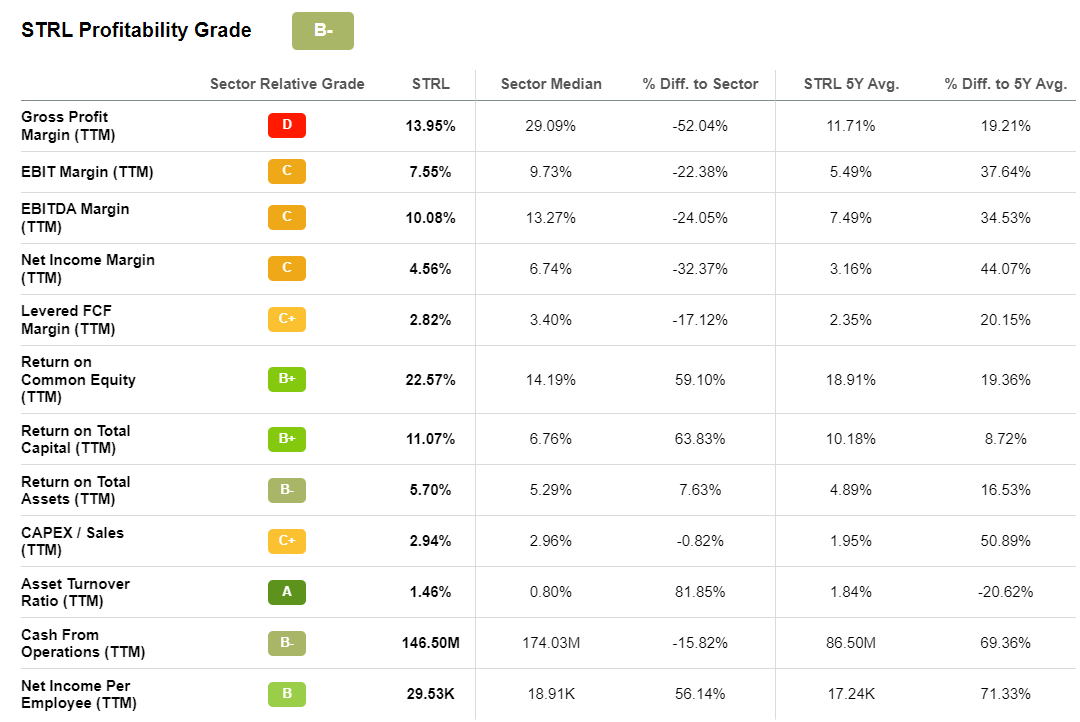

In terms of profitability, margins are a bit on the low side but are trending in the right direction as many of the recent M&A transactions are absorbed and the synergies of the combined companies begin to materialize into better profit margins and lower expenses going forward. Some of the erosion of margins in the 3rd quarter were due to inflation and supply chain issues such as the elevated cost of diesel fuel.

Seeking Alpha

With a market cap of only $990 million, the stock is thinly traded with considerable volatility, so I would not be surprised to see big price swings before and after the Q4 earnings report. If you are looking for a solid small cap stock with good long-term growth potential in a relatively under-followed company that is trading at a fair price, STRL is a Buy at the current price of $33.49 as of 1/25/23.

If the price should drop below $30 again, and depending on the Q4 earnings results, I would consider it a Strong Buy. With a projected FY2023 EPS of $3.45 at a relatively conservative 12x multiple, I expect the share price to approach $41.40 by the end of the year. The 2024 estimated EPS is expected to increase to near $4 and could potentially increase even more by the time we get to 2024. At that rate, and with a history of beating expectations, I would expect the target price to be closer to $50 by the end of 2024.

Be the first to comment