katleho Seisa/E+ via Getty Images

Thesis

Sterling Check Corp. (NASDAQ:STER) is a leading provider of background screening services and one of the four largest providers, along with First Advantage (FA), HireRight (HRT), and Checkr. I remain positive on background screening as a whole, as the TAM is large and growing fast enough to support significant shares for all four leaders. For STER in particular, I like that management has placed an outsized focus on identity, bolstered by the company’s partnership with ID.me. I believe that this, combined with being the only fully cloud-native background screener, should lead to best-in-breed growth and justify a premium valuation. My $24.3 price target is based on a P/E multiple of 18x to my FY23 estimate.

STER Stock Price Movement (Seeking Alpha)

Why am I Bullish on STER?

Leading provider of background screening services for enterprise clients

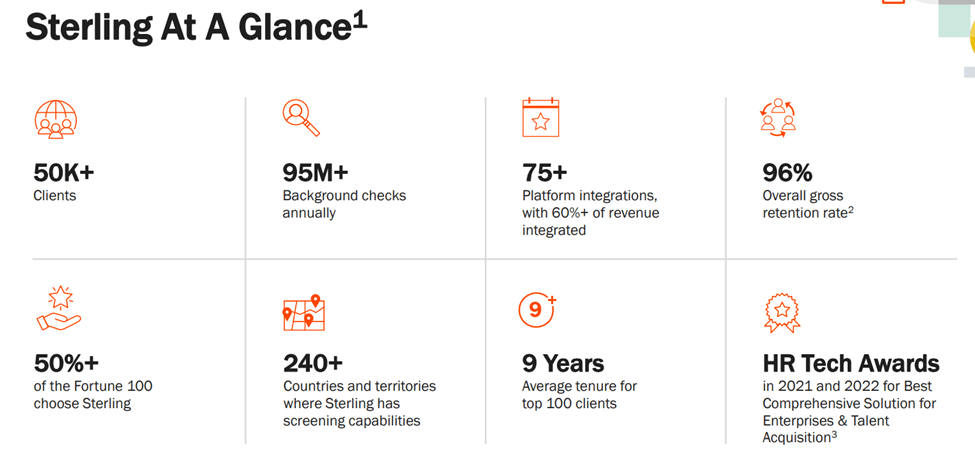

STER is a leading provider of background screening and identity verification services with offerings that include criminal background checks, identity verification, motor vehicle records checks, and social media searches. STER’s services are diversified across a variety of verticals, but the company has a notable presence in areas such as healthcare, industrials, government, education, and financial services. I am positive about the background screening market as a whole, given that the market is large and growing, supported by a study conducted by Acclaro Partners and Markets and Markets, which pegs the TAM at $9 billion ($16 billion when including identity verification) that is growing at a 12% clip. STER serves what I view as a largely blue-chip client base of more than 50,000 clients, which includes over 50% of the Fortune 100. The company’s revenue base is diversified, with no client being more than 3% of revenue, which I believe reduces customer concentration risk.

Sterling at a Glance (Company Presentation)

Solid organic growth

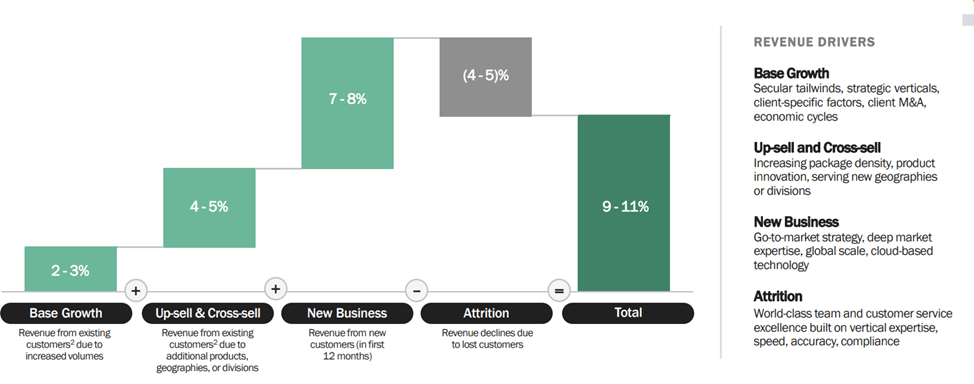

A core component of my constructive view on STER is a clear and reasonable set of building blocks that makes me comfortable with the company’s medium-term organic growth target of 9-11%. The growth outlook consists of 2-3% base growth (more volume with existing customers), a 4-5% lift from up-selling and cross-selling with existing customers, and a 7-8% contribution from new logos, partially offset by a 4-5% headwind from attrition as a small number of clients transition away from STER.

3-5 Year Organic Revenue Growth Target (Company Presentation)

I expect the contributions from new business and assumptions on attrition to be the key debatable points surrounding organic growth over time. Current LTM attrition (as of Q3 2022) stood at 96%, up from 94% in FY21, so I view the attrition assumptions as reasonable based on historical performance. I also believe that STER fully operating in the cloud and the steady roll-out of new products/ integrations should help keep attrition inside this band.

Focus on identity verification sets STER apart

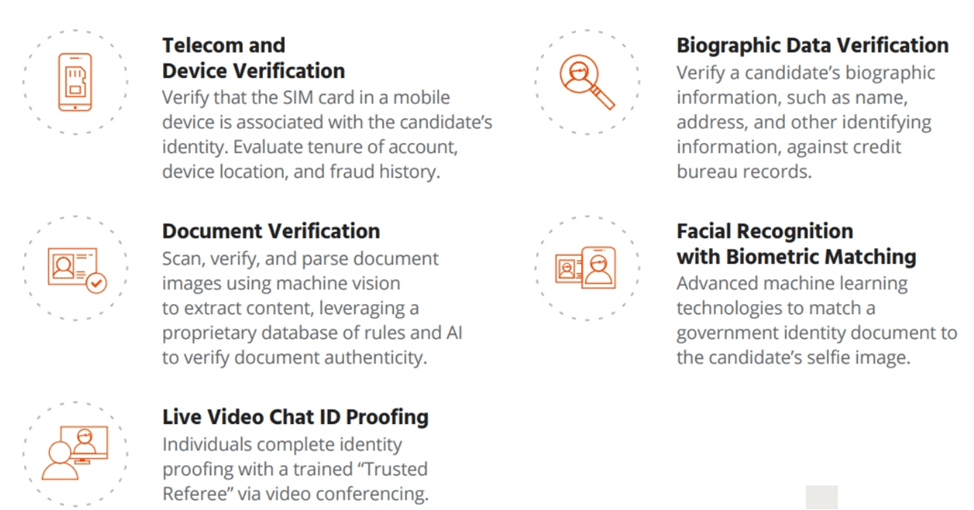

In addition to background screening, STER has an identity verification offering that significantly expands the TAM and is a natural strategic fit and complementary product for STER. STER partners with ID.me, a leading identity verification provider, to offer clients a way to integrate and verify personal information that candidates submit in background checks. I believe this sets STER apart from its closest competitors, as it allows employers to verify the identity of potential candidates during the application/interviewing process, rather than waiting to verify this information during the I-9/onboarding process.

Sterling/ID.me Identity Verification Offering (Company Presentation)

Financial Outlook

Topline

STER operates a delivery-based business model, with its revenue coming from its broad suite of services being sold either individually or bundled. The majority of STER’s revenue (~90%) comes from the company’s pre-employment offerings, which consist of background checks and verifications for new hires. STER has built a diverse client base over the years that spans industries including healthcare, financial services, business services, and industrials, and no customer accounts for more than 3% of total revenue. While STER derives the majority of its revenue in the US, the company is steadily expanding its international operations in regions such as Canada, and APAC.

STER has posted strong revenue growth in recent years, though in FY20, revenue dipped 8.7% due to significant pressure on the labor market at the onset of the pandemic. However, growth improved in 2H20 and accelerated in FY21, when revenue climbed 41.4%. I expect revenue growth will be driven by winning new clients, keeping attrition low (<5%), and by expanding client relationships through cross-sell and up-sell efforts. We also expect STER to be active on the acquisition front as the business continues to scale. We are forecasting revenue growth of 23.5% in FY22 due to the strong YTD performance and a full-year’s contribution from the EBI acquisition. In FY23, we are forecasting revenue growth of 9%, in-line with STER’s MT target (9-11%). In the figure below, we have shown <5%), and by expanding client relationships through cross-sell and up-sell efforts. I also expect STER to be active on the acquisition front as the business continues to scale. I forecast revenue growth of 23.5% in FY22 due to the strong YTD performance and a full-year’s contribution from the EBI acquisition. In FY23, I am forecasting revenue growth of 10%, in-line with STER’s MT target (9-11%).

STER Long-term Targets (Company Presentation)

Margins

While EBITDA and margins took a hit in FY20 due to the pandemic, which reduced the company’s revenue base and added incremental costs as companies shifted to remote work, profitability and margins rebounded significantly the following year as economies reopened around the globe and management effectively managed costs. I expect the EBITDA margin to deteriorate by ~40 bps (to 27.5%) in FY22 as the company absorbs public company costs incurred since its IPO in September 2021 and also faces higher third-party data costs that pressure margins but are passed through to clients based on contractual agreements. Starting in FY23, I expect margin expansion to come from existing client growth, further penetration in the existing customer base, customer retention improvement, and the retirement of some remaining data centers given STER’s shift to a cloud-based delivery model over the past few years. I am forecasting an EBITDA margin of 28.1% in FY23 and expect continued margin improvement as the business scales towards STER’s MT target of 29-32%+.

STER Forecasted P&L (My Estimates)

Attractive risk/reward given the company’s growth and margin profile

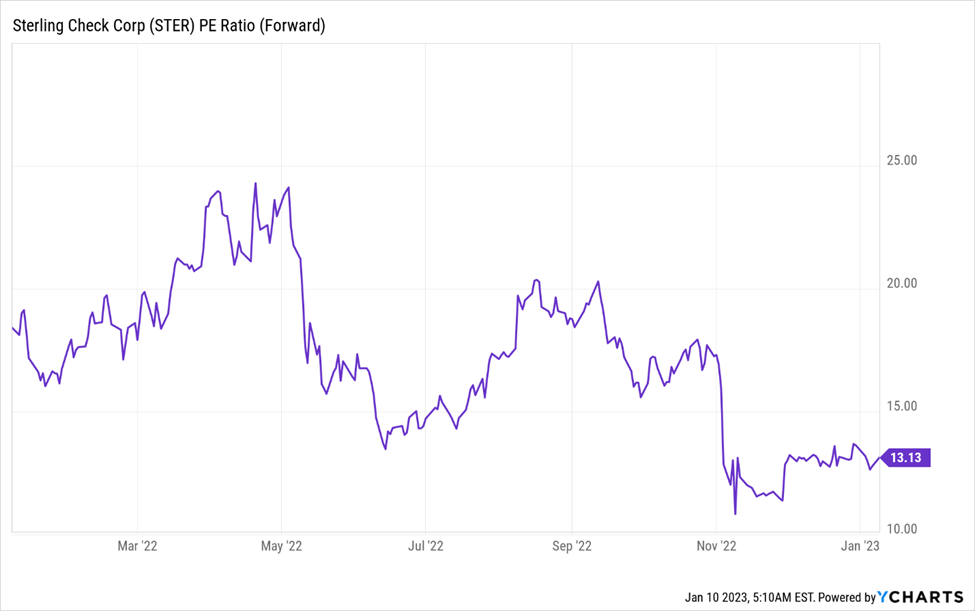

STER trades at a P/E multiple of 13x of FY23 earnings estimate, at a significant discount to the group of established information services companies such as Equifax Inc. (EFX), Fair Isaac Corporation (FICO), TransUnion (TRU), and Verisk Analytics, Inc. (VRSK). I believe the shares of STER can re-rate higher towards the multiples of the more established information services stocks over time as investors become increasingly comfortable with the growth, margins, and durability of the revenue and EPS streams. My $24.3 price target is based on a P/E multiple of 18x and my FY23 earnings estimate of $1.35.

STER Forward P/E (YCharts)

Risks

- STER could face liability based on its services and the information reported or failed to report in background screening, which may not be covered by insurance.

- Security breaches may result in the disclosure of personal/confidential information, which could negatively impact the business and/ or harm STER’s reputation.

- STER’s ownership is largely held by a large pre-IPO investor. If this owner elected to reduce its holdings, it could create NT selling pressure and weigh on the share price.

Final Thoughts

I believe that STER has entrenched itself as a leading provider of background screening and identity verification services, two complementary and quickly growing markets that help enterprise organizations onboard and maintain talent. My view is that the large and growing TAM and STER’s advantage as the only global background screening provider that fully operates in the cloud will enable the company to maintain its best-in-breed organic growth for the next several years. Therefore, I keep a December 2023 price target of $24.3 on the stock.

Be the first to comment