Taitai6769/iStock via Getty Images

Investment Thesis

Steel Dynamics (NASDAQ:STLD) is putting its pedal to the metal and is deploying substantial capital back to shareholders. Its preannounced Q2 2022 total return points to an annualized 12% total return.

Simply put, Steel Dynamics is very cheaply priced and operates in a favorable pricing environment.

Paying 3x this year’s EPS is very attractive.

Here’s why I rate this stock a buy.

Steel Dynamics Near-Term Prospects

Two weeks ago, Steel Dynamics preannounced its Q2 2022 earnings. Steel Dynamics guided its Q2 adjusted EPS at the midpoint to reach $6.63, an increase of 95% y/y from the adjusted EPS of $3.40 last year.

That’s undoubtedly a strong increase in EPS. So why is the share price down since that preannouncement? In fact, it’s not entirely surprising that Steel Dynamics saw strong results.

Several of its peers had also preannounced or reported results, such as United States Steel, Nucor (NUE), and Algoma Steel (ASTL).

The results throughout the sector are looking very similar, we are seeing very strong revenues or even record revenues. And yet these stocks are going nowhere fast. Why?

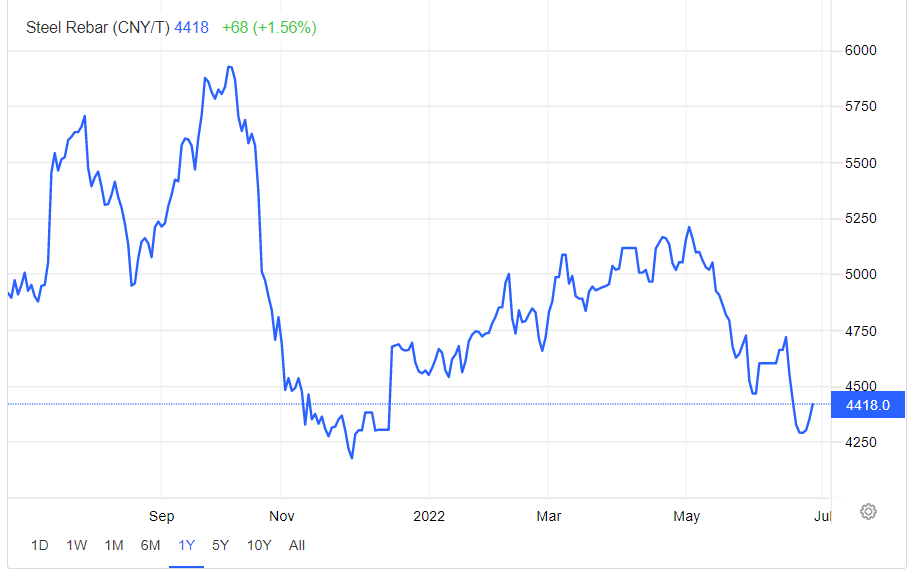

Investors are fearful that if we go into an economic recession, demand for steel will rapidly dwindle. And this argument has up to a certain point been reflected in steel’s pricing in the spot market.

Trading Economics

That being said, I’m not entirely sure that steel pricing in the spot market is looking all that weak.

Yes, pricing has come down by approximately 14% from the highs made 2 months ago, but I don’t get the impression that the spot market for steel is looking quite as gloomy as investors are viewing the equity for steel stocks.

The market appears to be indicating that steel peers will have a strong 2022. But then what? What happens after Q2 2022? Will steel demand tail off?

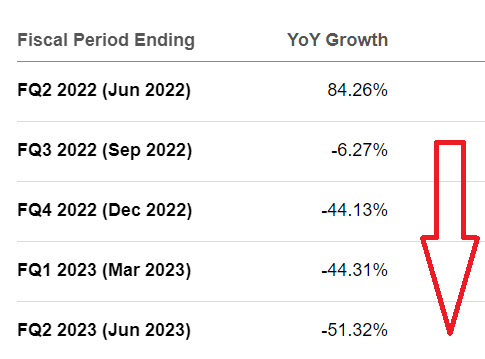

STLD EPS estimates

Above we see that analysts are estimating that once we get past Q2 earnings, Steel Dynamics EPS numbers fall off a cliff. Rapidly.

And I simply refuse to buy this argument. Why would steel demand dwindle? After all, doesn’t President Biden’s infrastructure Bill call for elevated steel demand?

Isn’t steel in everything that we require to build a country? Isn’t there so much pent-up demand for EVs? What about buildings? Isn’t there a reported shortage of housing?

Hence, I contend that even if interest rates come up slightly further, this will not dent the demand for steel.

What’s more, let’s rewind the clock back 20 years. Weren’t interest rates often significantly higher than they are expected to exit in 2022?

Thus, from several angles, I believe that Steel Dynamics is cheaply valued. And it appears that Steel Dynamics management does too.

Capital Allocation Strategy, 12% Combined Return

For context, Steel Dynamics’s balance sheet finished Q1 2022 with a net debt position of $2 billion and a 0.4x net debt to EBITDA ratio. Steel Dynamics ended Q1 2022 with some immaterial borrowings under its letters of credit. For all intents and purposes, the revolver remains undrawn.

STLD Q1 2022

Accordingly, Steel Dynamics’ balance sheet is very strong, with ample liquidity.

Altogether, this has allowed Steel Dynamics to announce a new $1.25 billion share authorization to be rolled out.

In fact, during Q2 2022, Steel Dynamics didn’t hesitate to buy back 2.5% of the company and deploy nearly $400 million worth of capital. This is nearly a third of its share repurchase program gone in 90 days.

Furthermore, when taken together with its 0.5% dividend yield, this puts Steel Dynamics on a path to annualized 12% combined capital returns.

Indeed, the point I’m making here is that Steel Dynamics has a share repurchase program and isn’t holding back from aggressively using it.

STLD Stock Valuation – 3x EPS

For H1 2022, Steel Dynamics is going to report approximately $12.37. Even if the analysts following the company are vaguely correct, and Steel Dynamics’ H2 2022 EPS turns south, it’s very likely that Steel Dynamics’ full year 2022 EPS could reach $20.25.

This puts the stock priced 3x this year’s EPS.

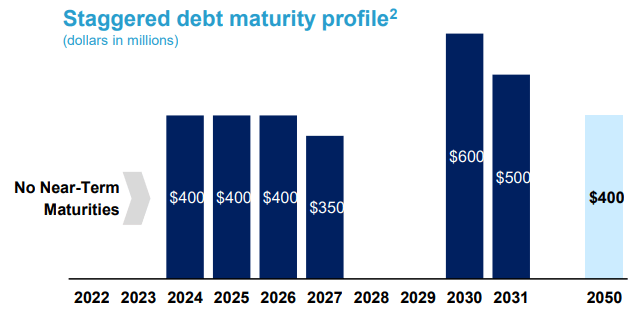

Remember, Steel Dynamics holds no near-term debt maturities and its balance sheet is notably strong. There are no hiding risks lurking in its debt structure.

The only question is will steel prices remain stable or will they rapidly fall off?

The Bottom Line

One big problem with investing in commodities is that they are very volatile, right? Well, guess what, investing in a tech company hasn’t been great either this past year.

The main difference between Steel Dynamics and many unprofitable tech companies is that with Steel Dynamics you are getting all your earnings up front, and there’s the question of whether or not in the future the business will continue to report attractive earnings.

While on the other hand, with unprofitable tech companies today, investors are paying very rich multiples, in the hopes that those future earnings at some point materialize.

There is nowhere to hide in my opinion. Consequently, you may as well recognize that there are many risks to investing and get paid a 12% combined yield while you see how the future unfolds. Whatever you decide, good luck and happy investing.

Be the first to comment