njpPhoto/iStock Unreleased via Getty Images

Overview

Stanley Black & Decker (NYSE:SWK) is the manufacturer of power tools with a worldwide reach, a long and storied history, and a rock-solid history of annual dividend raises. As such, it has long been a darling of the dividend crowd. Recently, however, things have taken a turn for the worse. Inventory levels have grown to unsustainable highs, and company leadership has had to slash production. In the midst of this turnaround effort, the company has taken on more and more debt, which could imperil the company’s historically stalwart dividend if turnaround efforts are not successful. Furthermore, negative macro headwinds could create a perfect storm for the company. The current management at SWK is new, and we will be watching their turnaround efforts closely.

No Longer In The Black

Black and Decker operates in three business units, the most visible and largest of which is the Tools & Storage segment, which accounts for 82% of the company’s roughly $17 billion of annual sales. Next in line is the Industrial segment at 16%, and the Security Solutions unit which constitutes about 2%.

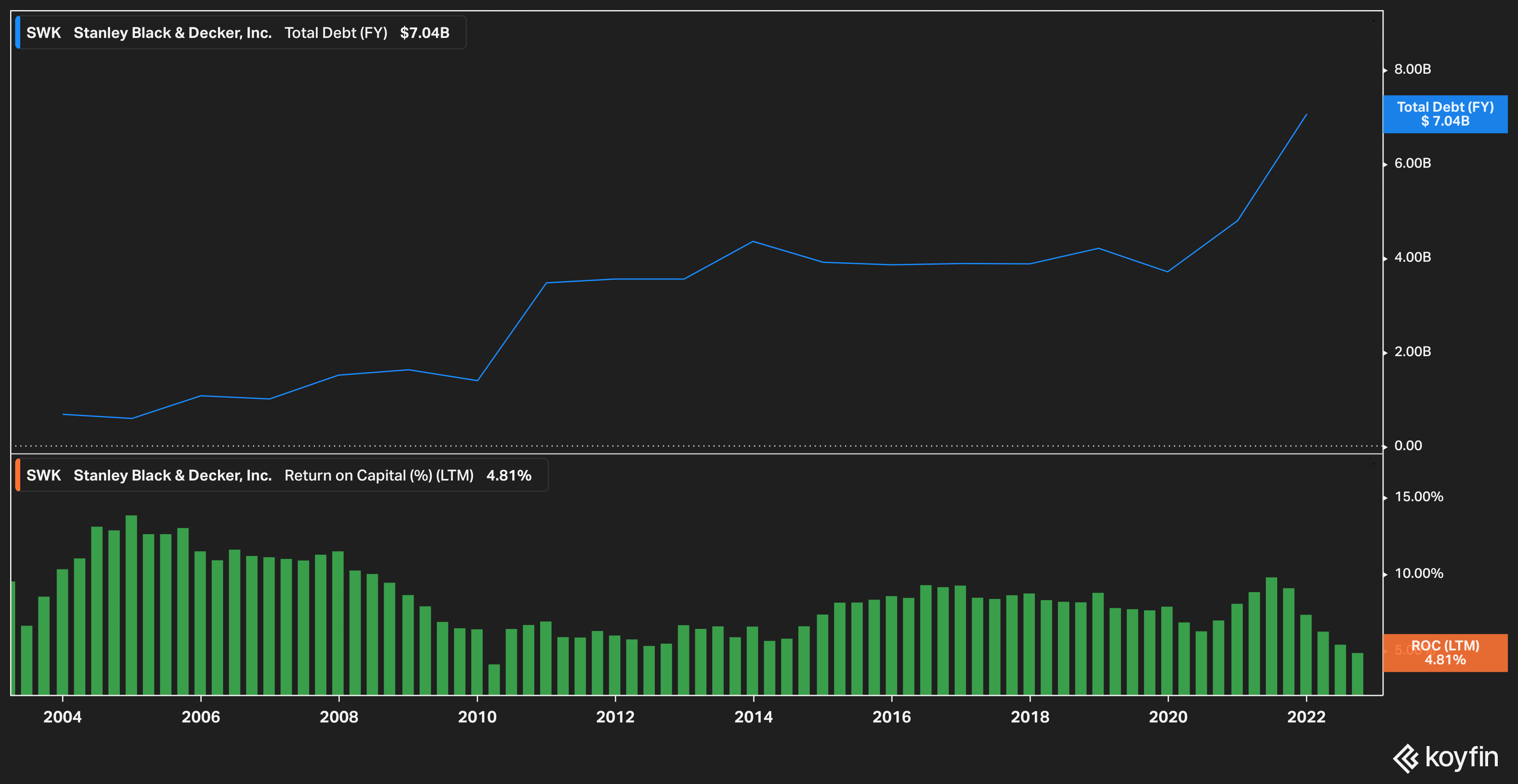

The company is being battered on all sides: rising inventory levels, softening consumer demand both in the United States and abroad, inflation impacting costs, supply chain issues, and, perhaps most importantly, rising mortgage rates. The company has also been active in M&A over the last several years, taking on a debt load that has reached new heights (see chart below), while concurrently generating the lowest return on capital in over 10 years. In the midst of it all, Black & Decker has empowered a new management team to turn things around, promoting Donald Allen Jr, formerly the company’s finance head, to CEO on July 1st 2022.

SWK Debt & ROC (Koyfin)

While the debt may not currently be at unsustainable levels, the company was free cash flow negative in Q3 2022, and its dividend payout ratio spiked to 32%. Management took great pains to assuage investors on the Q3 call that this margin and profit compression and negative free cash flow was temporary and the result of painful destocking (reducing inventory levels), but the concerns remain the same: if management is unable to pull off their strategy, then SWKs dividend could be imperiled.

The rising debt levels have not gone unnoticed by the ratings community. In December 2022, Moody’s downgraded SWK’s debt from Baa2 to Baa1. Moody’s states the current concerns quite well:

The downgrade of Stanley’s ratings to Baa2 from Baa1 and negative outlook results from the company’s inability to generate meaningful cash flow for debt reduction, limiting liquidity and materially delaying deleveraging goals. Moody’s estimates that Stanley will have about $2.1 billion of short-term debt ($8.8 billion total adjusted debt) outstanding at year-end 2022 versus previous expectations that all short-term debt would be repaid. Moody’s now projects adjusted debt-to-EBITDA of about 4.8x by late 2023 (2.5x previously) and 3.7x by late 2024, which includes $1 billion of short-term debt being repaid in each year from free cash flow and a material improvement in profitability.

More immediately concerning, however, is the steady, multi-year decline of Black & Decker’s return on capital. At its current level of 4.8%, SWK is currently under-earning its estimated cost of capital, which we peg at around 11% (utilizing the current prime lending rate of just over 7% and SWK’s recent credit downgrades). Companies that cannot earn more in return on their invested capital than the cost of said capital run the risk of eventually cannibalizing themselves and falling into a nasty debt spiral. This is disappointed to see from Black & Decker, since it wasn’t all that long ago that the company was consistently delivering double-digit ROC figures.

Management hasn’t simply been laying around while all this happens, of course. The company announced cost-cutting measures and headcount reductions that saved $65 million in the third quarter, and management expects that its efforts in the long run will save the company $1 billion in 2023. While this is certainly nothing to sneeze at, we wonder if it will be enough.

Fighting The Tide

While inventory levels, headcount, and dividend payouts are all things that company leadership can affect, the harsh truth remains that outside forces are likely the largest driver of negative news for Black & Decker. With a recession almost certainly on the horizon around the world coupled with rising interest rates, Black & Decker is uniquely positioned to suffer with its Tools & Storage business unit (again, 82% of sales) taking the brunt of it as consumers tighten the purse strings and hold back on home improvement projects.

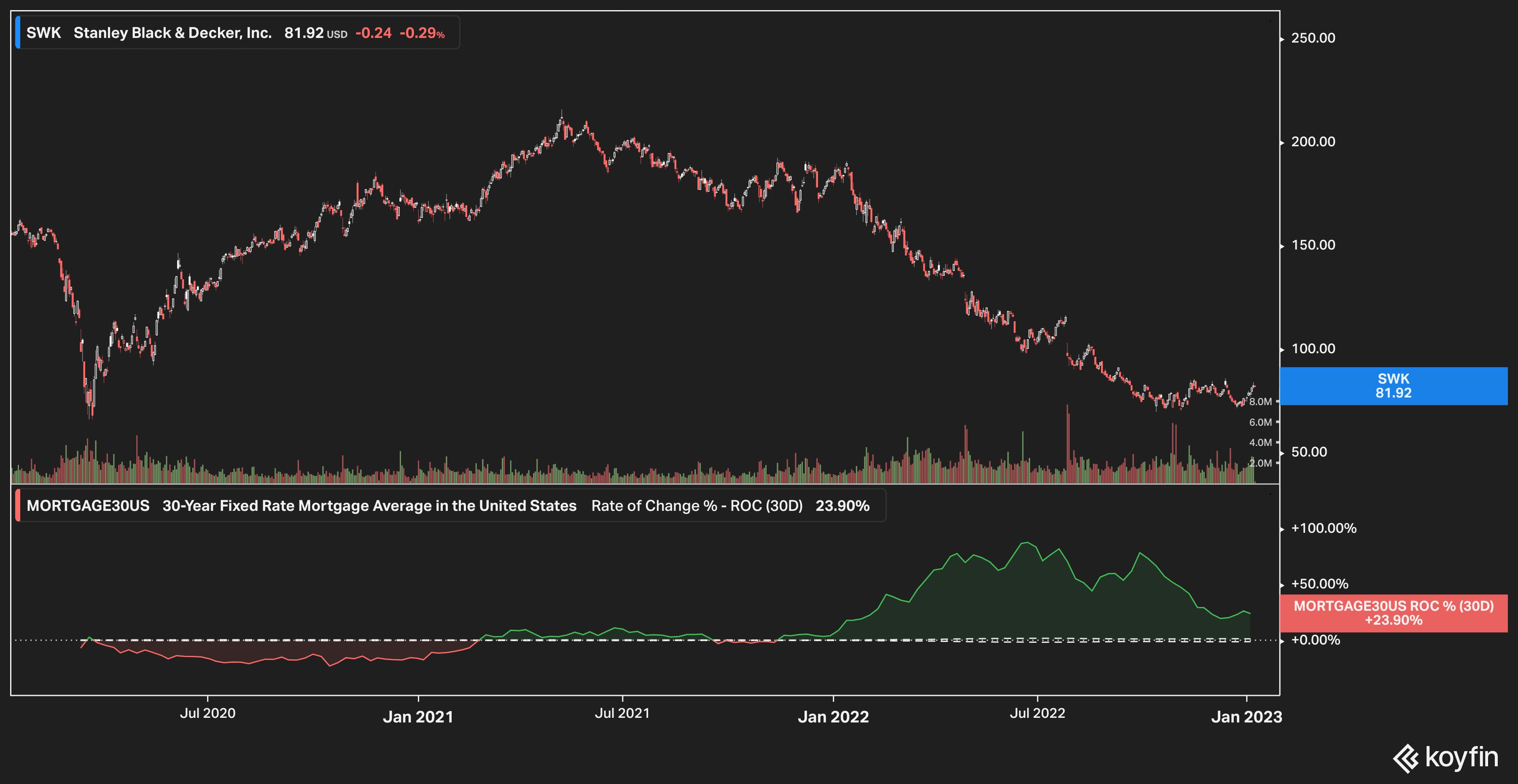

That the world is on the brink of recession and that businesses such as Home Depot (HD) who rely on free spending consumers are hurting as a result is no secret. What’s talked about less is the correlation between these companies and mortgage rates (see chart below).

SWK Price vs 30yr Mortgage ROC (Koyfin)

The above chart illustrates SWK’s historical price compared to the change in 30 year mortgage rates. Starting at the pandemic and the ‘flash recession’ of March 2020, SWK’s price rapidly climbed as lockdowns ensued, stimulus checks were issues, and the housing market took off to near-unprecedented heights as mortgage rates raced to their lowest point in history, bottoming out near 2.75%.

All good things must come to an end however, and as inflation loomed, the fed acted and raised rates, which in turn caused mortgages to rise. The rate of change on 30 year mortgages turned positive in April 2021, which coincided with SWK’s peaking at just over $200 per share. For several months the stock ranged between $180 and $200 as mortgage acceleration similarly stalled, but in January of 2022, the gas pedal was pushed.

In January 2022 the 30-day rate of change on mortgage rates spiked 17.8%, and SWK’s stock immediately took a hit, tumbling from $180 to $160. Since then, the story has largely remained unchanged—while the rate of change on mortgages remains elevated, SWK continues to fall.

This is interesting, because in previous cycles where mortgage rates have accelerated rapidly to the upside, Black & Decker was not similarly punished. So why has this time been different? One word: inflation.

Rising mortgage rates have a cooling effect on home buying activity, which is no surprise. In these times, people typically move less and begin to invest more into the homes they currently have since the prospects of leaving in the near future are lower. However, in those past times of rising mortgage rates, consumers did not have to battle the looming specter of inflation at the same time. As a result, not only are people not buying Black & Decker products to spruce up their new homes, but they’re also delaying improvement projects on existing homes to save money.

Yet, there is even more bad news. Even if mortgage rates de-accelerate and inflation suddenly cools as a result of steady-but-higher interest rates, Black & Decker’s business will still have to contend with a near-term recession arising from a likely spike in unemployment.

Is Black & Decker Fairly Valued?

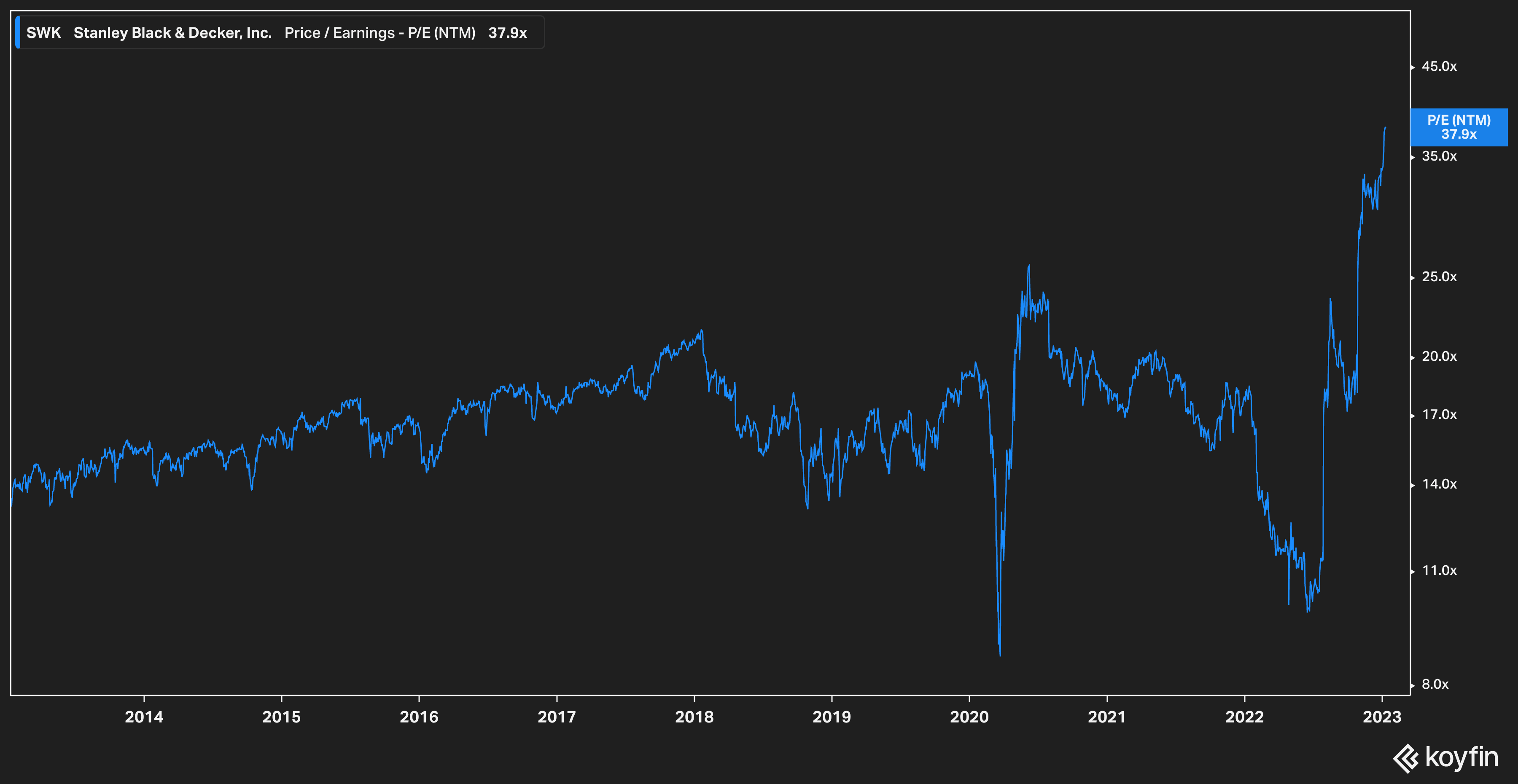

Despite its fall, we believe that Black & Decker remains slightly expensive. The company currently trades at a future P/E far above its historic average (see chart), but this is to be somewhat expected when management has slashed its profit targets for the year by almost 50%.

SWK FPE (Koyfin)

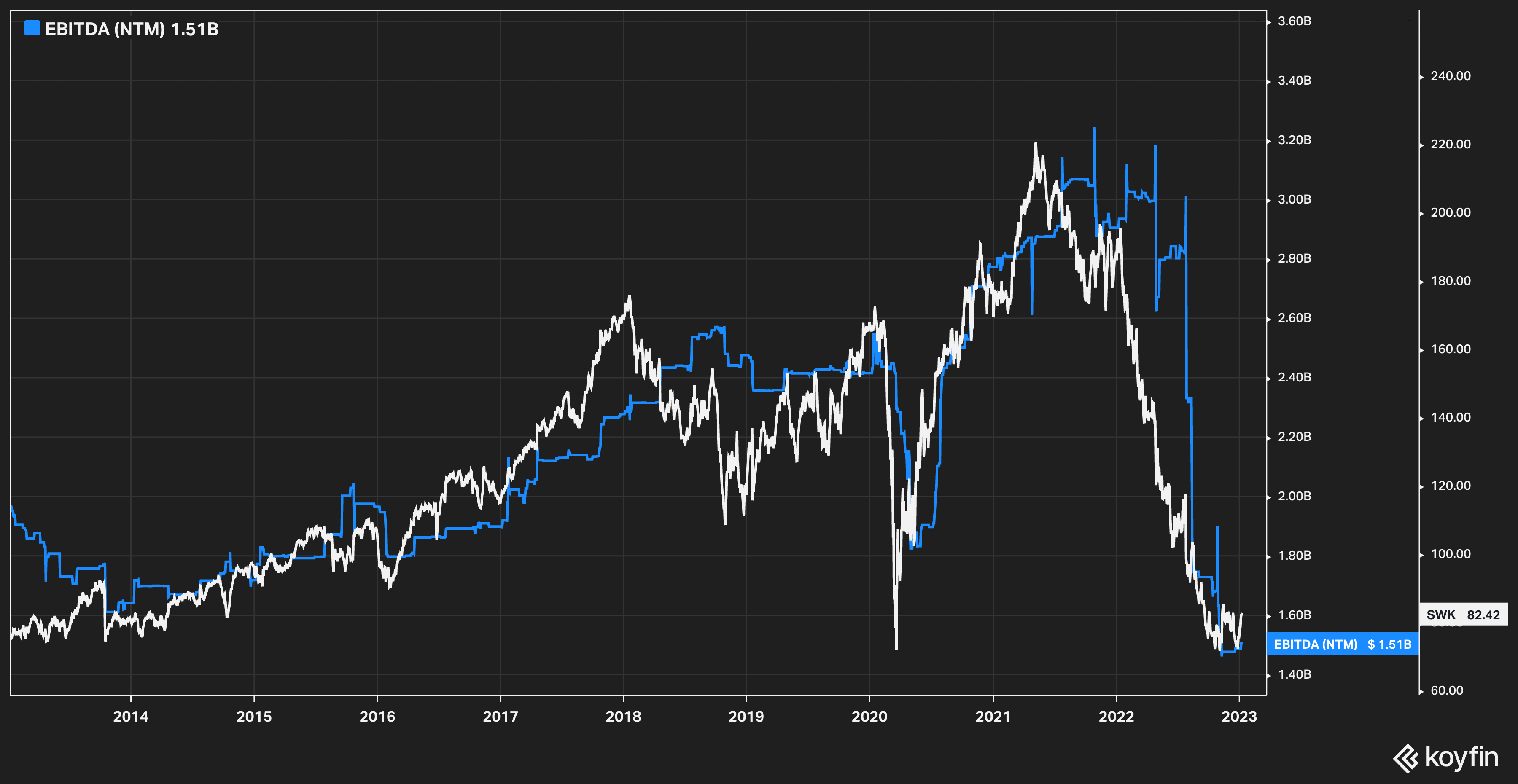

More interested in the question of valuation is how the stock stacks up against its historical EBITDA. Traditionally the stock has largely tracked its expected EBITDA, and the chart below shows that the current price is no exception.

SWK Price vs. EBITDA (Koyfin)

Nonetheless, we still believe that the stock could break through its flash-recession of March 2020 price of about $68 and fall to the $60 range as the uncertainty around its business prospects looms.

The Bottom Line

Again, there a lot of moving parts here, so we’ll cover them one-by-one. Each of these, we believe, are serious risks to the success of Black & Decker over the next 2-3 years.

- The management team is new and is currently executing a turnaround amidst a gaggle of macro headwinds. They want to return the company to a 35% gross margin, which up until 2016 was kind of the steady-state margin level.

- Elevated mortgage rates coupled with inflation present the most immediate concern. If either or both of these persist, management’s efforts could yield little result.

- A recession in 2023 will provide an additional headwind for SWK.

- Rising debt levels and an associated increased cost of servicing that debt could pose a risk to the dividend if management’s turnaround is not as successful as hoped.

On the flip side, if any of the four points made above fail to materialize or are less impactful to the overall economy than expected–say, if the a 2023 recession is particularly mild and affects housing less than other parts of the economy–then SWK could experience a positive bump. Furthermore, if management is able to accomplish their goals in spite of these headwinds, SWK may prove to be a good value stock.

At this time, however, we think there is still a significant risk in Black & Decker’s near-term future. We’ll be watching this stock closely, but today we believe investors will find better value elsewhere.

Be the first to comment