Khaosai Wongnatthakan

Stagwell (NASDAQ:STGW) is the result of the acquisition of hitherto private Stagwell and the public MDC Partners (MDC), which took place in August 2021. Stagwell brings a digital-first approach and expertise while MDC brought creative agencies like 72andSunny, Anomaly, Forsman & Bodenfors and Doner, with the whole company shifting to a digital focus.

Market

Global advertising is dominated by the big three agencies The Interpublic Group of Companies, Inc. (IPG), Omnicom Group Inc. (OMC), and WPP plc (WPP).

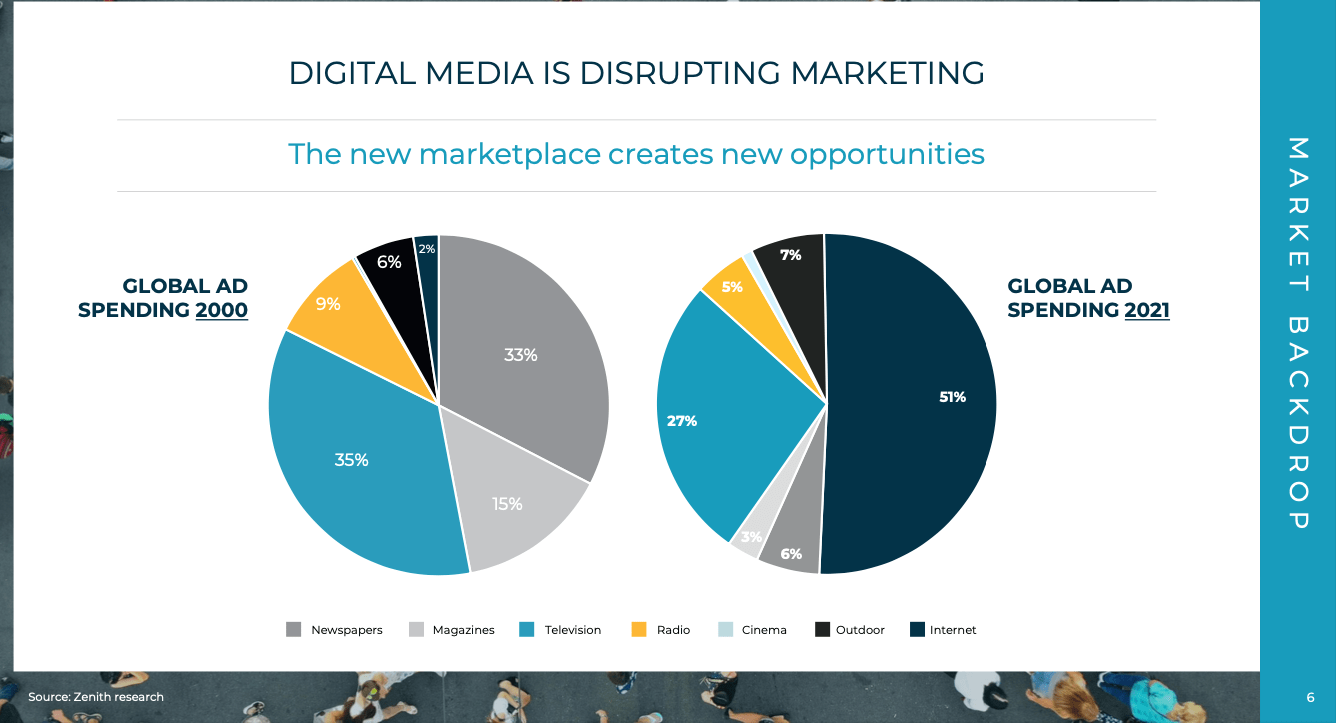

However, the market has been shifting, from the Sept/22 IR presentation:

Stagwell IR presentation

As that IR presentation no longer seems available on the company website, we plucked that from the excellent SA article by Courage & Conviction Investing who was able to interview the CEO personally. Required reading! From the 10-K:

The rapid rise of digital channels, convergence of advertising and commerce, explosion in addressable data and marketing technology created a paradigm shift in the industry.

The digital revolution is of course no surprise as it deals with the problem of addressability, that is, precision targeting. But these digital capabilities require a whole new set of capabilities, which was (and is) the premise on which Stagwell was founded to which they added a creative impulse through the merger with MDC Partners in August last year.

This creative side is an advantage they tend to have over new entrants who took advantage of the paradigm shift (10-K):

A number of large consulting firms with information technology implementation backgrounds have entered the marketing services market and, collectively, achieved significant market share. However, we believe these firms’ lack of creative and media expertise limits their long-term growth potential as true challengers to the legacy marketing holding companies.

Capabilities

The company has four broad categories of capabilities

- Digital Transformation

- Performance Media & Data

- Consumer Insights & Strategy

- Creativity & Communications.

The company reports in a number of segments:

- Integrated Agencies Network (the Anomaly Alliance, Constellation, the Code and Theory Network, and the Doner Partner Network).

- Media Network (omnichannel campaign strategies leveraging significant amounts of consumer data).

- Communications Network (providing strategic corporate communications, IR and PR online fundraising and other services to both corporations and political and advocacy organizations).

- All other (Company’s digital innovation group, and Stagwell Marketing Cloud products such as PRophet).

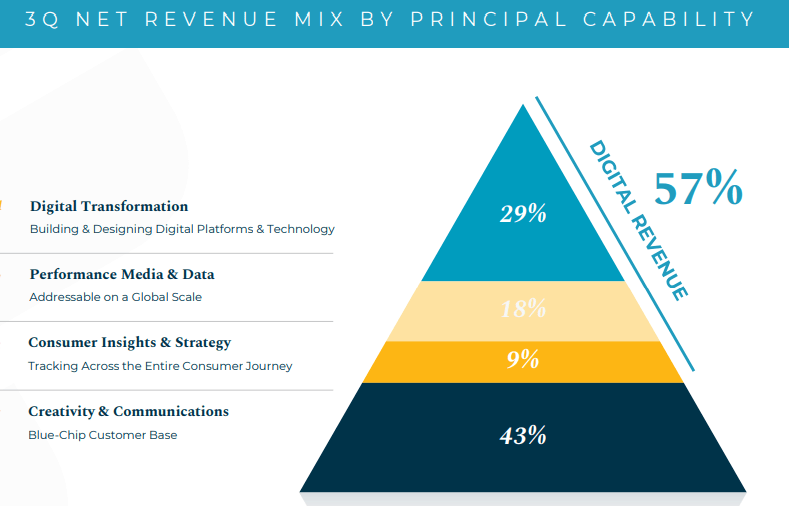

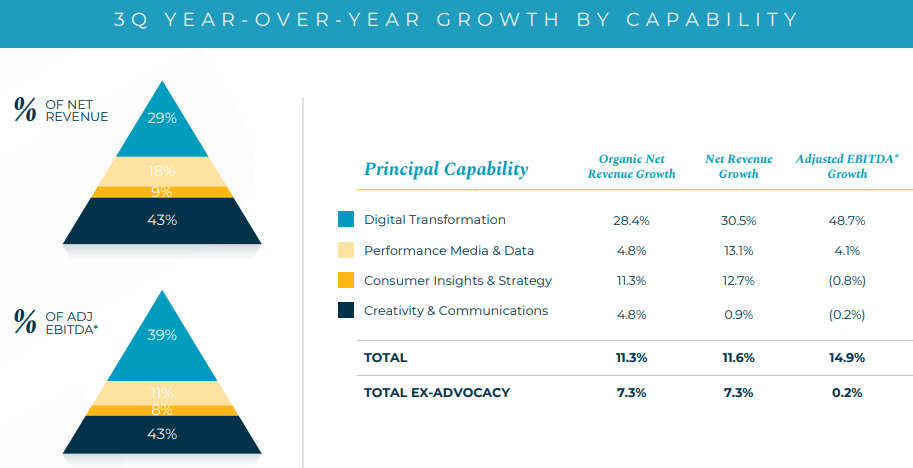

From the Q3 earnings deck:

Stagwell Q3 earnings deck

Apart from its own agencies, the company also has a network of Agencies, tech companies, and marketing services firms called Global Affiliates. Its Digital Marketing Cloud is (10-K):

A suite of technology products in development or early-stage commercialization spanning influencer marketing, audience segmentation, public relations, immersive experiences and brand insights. These products are licensed to our clients using subscription-based SaaS and DaaS models and distributed by Agencies across our network.

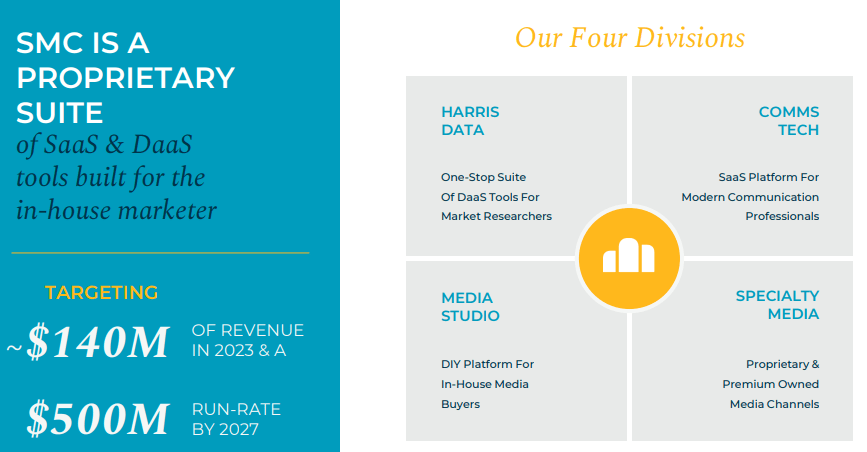

Their digital capabilities form the core of their competitive advantage, perhaps the most innovative part is SMC, or the Stagwell Marketing Cloud:

Stagwell Q3 earnings deck

These innovative services are introduced on fertile grounds providing a competitive advantage (Q3CC):

the fact that we have an infrastructure of a service business allows us for relatively small investments to get the cloud off the ground. And that is our unique advantage compared to a lot of the startups and the other companies out there that don’t have this full infrastructure or understanding of technology or ability to apply it in this way.

And they can do this with relatively little investment (Q3CC):

because we have the expertise, because we already buy $5 billion of media and therefore, have the proving ground for our technologies. But I’m really able to keep, we’re investing $5 million of OpEx, maybe we’ll invest $10 million of OpEx next year. We’re able to keep the level of investments in OpEx here, quite low.

If ‘digital capabilities’ is too abstract for your taste, the company website has extensive descriptions of a host of cutting-edge digital products like ARound (next-level fan engagement through social AR), The Harris Poll (a brand management software tool), Koalifyed (influencer marketing), Navigator (marketing platform for reaching travelers), PRophet (AI driven PR) and Telepia (customer data acquisition tool).

Growth

The company is certainly growing although keep in mind that these growth rates are hugely overstated as they are mostly the result of the merger with MDC which took place in Q2/21.

Their overall YTD organic growth was nevertheless a very respectable 17%, considerably beyond their long-term target of 10%-12%. The main growth drivers are (Q3CC):

Our digital layers, digital transformation, performance media and data and consumer insights and strategy continue their impressive performance. Combined, they grew net revenue 21% in the quarter on top of 38% growth in 3Q, ’21 and have grown 30% year-to-date.

Digital transformation alone grew 28% in Q3 and 38% YTD on an organic basis. No surprise it’s mostly their digital capabilities that provide the biggest growth impetus.

There were a few notable growth vectors with GALE, their digital agency and Targeted Victory (their fundraising business) experiencing triple-digit growth rates.

The market is getting more fragmented with relatively new entrants like TikTok, Amazon (AMZN) and Walmart (WMT) marketplaces, and especially Netflix (NFLX) in CTV. This offers the company additional outlets for digital ads (rather than just Facebook (META) and Google (GOOG) (GOOGL)) although this broadening of the market could exert downward pressures on CPMs.

Downturn?

Other companies in the ad space have been rather cautious, from analyst Laura Martin from Needham (Q3CC):

But you haven’t seen slowdowns in Q4 which is not what we’re hearing from Meta, Google, Roku, Paramount, all of them have said 4Q is horrible.

But not Stagwell:

- Great momentum with record $86M in new business in Q3 and $1B pf pitch opportunities.

- They rely more on digital solutions compared to competitors, and these are growing faster, leading them to take market share and grow about twice the rate of their competitors.

- They also have a largely variable cost business and can easily downsize if necessary, which became useful during the pandemic.

Of that $1B pitch opportunities, they will not be participating in some $200M of these and get a fair share of the $800M, and takes 2-6 months to be executed.

So there is both momentum and a buffer, but that’s no absolute guarantee that things can’t deteriorate.

Financials

Some core data, on a proforma basis (that is, organic growth):

- Net revenue excluding pass-through costs +12% to $556M

- Ex-Advocacy, revenue, and net revenue increased 10% and 7%, respectively (pro-forma)

- Digital transformation +28% in Q3 and +38% YTD organically

- Performance Media & Data +5% in Q3 and 13% YTD organically

- Consumer Insights and Strategy +11% in Q3 and 29%YTD organically

- Creativity and Communications +5% in Q3 and 6% YTD organically

- AEBITDA +15% to $115M or +60bp to 21%

- Pro Forma YTD AEBITDA growth of 19.4% (+50bp) versus the prior period and 12.9% ex-Advocacy

Stagwell Q3 earnings deck

It’s a little surprising they couldn’t narrow down the Advocacy guidance, which should have a good H2 due to the mid-term election cycle, but 18% growth at midpoint is very solid nevertheless.

Their digital services grew net revenue by 21% y/y (17% organic growth) and comprise nearly 60% of revenues.

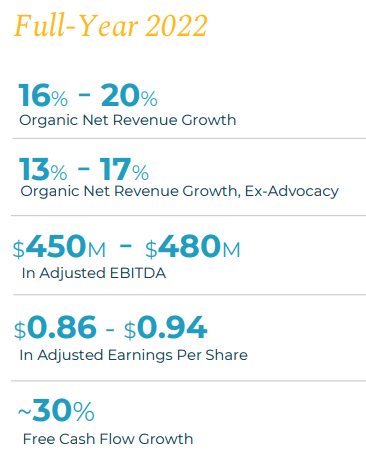

Guidance

From the Q3 earnings deck:

Stagwell Q3 earnings deck

Cash and balance sheet

The company enjoyed solid free cash flow Q3 enabling it to reduce net debt by $125M and the net leverage ratio to 2.7x towards its long-term goal of 2.5x. The company produced $73M of operational cash flow YTD and reaffirmed its proforma free cash flow growth for FY22 of 30%.

The company has $165M in cash and $1.3B in long-term debt.

Valuation

Something curious, on the front page of the 10-Q (our emphasis):

The number of common shares outstanding as of October 28, 2022 was 130,785,623 shares of Class A Common Stock, 3,946 shares of Class B Common Stock, and 164,375,682 shares of Class C Common Stock.

However, later in the same 10-Q:

There are 250,000 shares of Class C Shares authorized. There were 164,376 Class C Shares issued and outstanding as of September 30, 2022. The Class C Shares do not participate in the earnings of the Company and have a par value of $.00001.

We assume the first (164,375,682) figure to be the correct one (as it’s also used in the shareholders’ equity table in the 10-Q) so 295M shares outstanding and a market cap of $1.77B and an EV of $2.9B or an FY22 EV/S of 1.1x, really not expensive.

These are on GAAP measures, with management guiding non-GAAP EPS for 2022 at $0.90 (midpoint), the shares are downright cheap on an earnings basis.

Conclusion

- The company has remained financially disciplined through the merger with MDC Partners and some smaller acquisitions, infusing the creative agencies from MDC with the digital capabilities of Stagwell.

- They are managing to outgrow their competitors on the basis of these digital capabilities and they keep ahead through tuck-in acquisitions and development like SMC.

- So far, there is little sign of gathering macro headwinds, but this is definitely a risk, as is their organizational complexity (70+ agencies in 34 countries, etc.).

- We would argue that most of that risk is already priced in with the shares on very reasonable sales and earnings multiples for a company with 10%+ organic growth and a 20% AEBITDA margin.

Be the first to comment