Scott Olson

Author’s note: This article was released to CEF/ETF Income Laboratory members on January 16th.

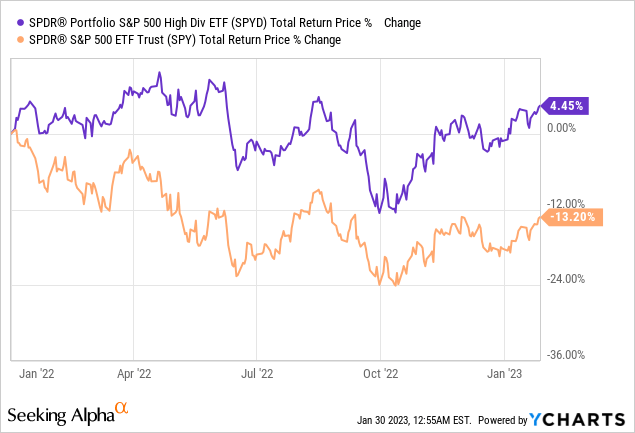

I’ve covered the SPDR Portfolio S&P 500 High Dividend ETF (NYSEARCA:SPYD), a high-yield equity index ETF, several times these past few years. I’ve been bullish, due to SPYD’s strong dividend yield and cheap valuation. SPYD has performed exceedingly well since I’ve started covering the fund, consistently outperforming the S&P 500, and by very healthy margins. Said outperformance has put pressure on the fund’s yield and valuation, reducing future expected returns.

In my opinion, SPYD is currently fairly valued. SPYD remains a buy, due to its diversified holdings and above-average, growing 4.1% forward yield, but I do not expect significant outperformance moving forward. Investors might do better by focusing on funds with stronger value propositions and expected returns that SPYD, although there is nothing inherently wrong with the fund itself.

SPYD – Overview and Benefits

Diversified Holdings

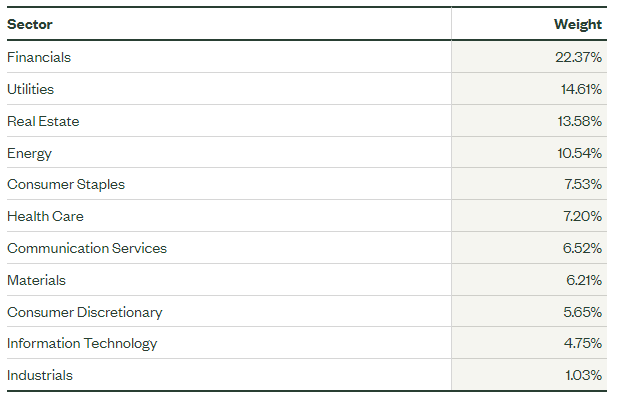

SPYD is a U.S. equity index ETF, tracking the S&P 500 High Dividend Index. Said index includes the 80 S&P 500 stocks with the highest dividend yields, subject to a set of inclusion and exclusion criteria. At the discretion of the index provider, companies with unsustainable dividends are excluded from the index. It is an equal-weighted index, with every stock having weight of 1.25%.

SPYD is a reasonably well-diversified fund, with exposure to most relevant industry segments.

SPYD

SPYD invests in 80 companies, equal-weighted. This is a reasonably large number of holdings, sufficient to ensure a good amount of diversification, although most broad-based equity indexes do have broader portfolios. The S&P 500, the most well-known U.S. equity index, invests in 500 stocks, much greater than SPYD’s 80.

SPYD’s diversified holdings reduce risk, volatility, and the possibility of significant losses and underperformance, all important benefits for the fund and its shareholders. Although SPYD is sufficiently diversified, investors looking for as much diversification as possible might wish to consider alternatives to the fund.

As with most dividend and / or value index ETFs, the fund is overweight old-economy industries like financials, utilities, and real estate, while being underweight tech. SPYD’s performance, especially its relative performance, is somewhat dependent on the performance of said industries, especially tech.

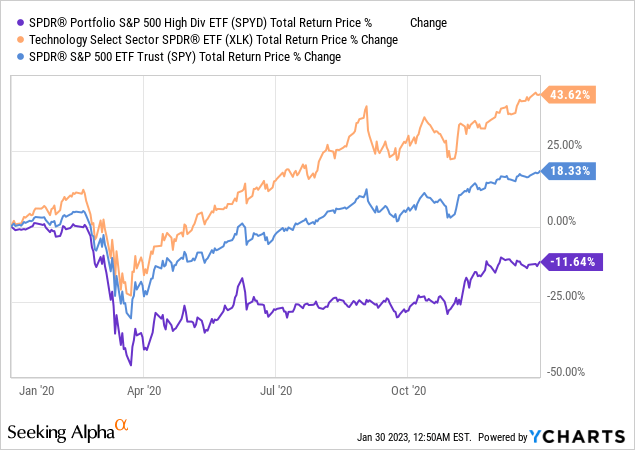

SPYD tends to underperform when tech outperforms, as was the case in 2020.

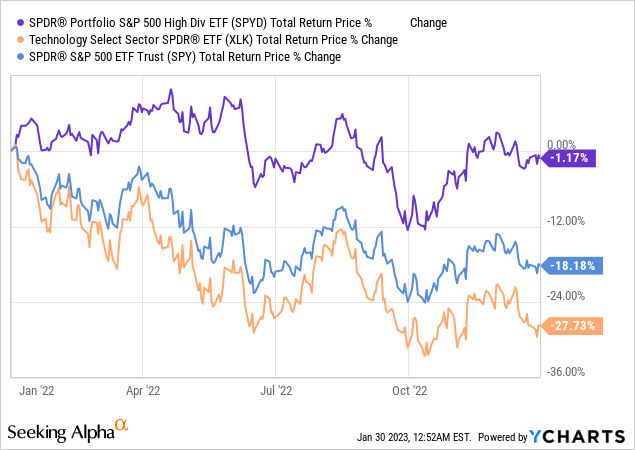

SPYD tends to outperform when tech underperforms, as was the case in 2022.

In my opinion, the above is neither a positive nor a negative, but it is an important fact that investors should consider. As an example, SPYD might be a more appropriate investment for tech bears, less so for tech bulls.

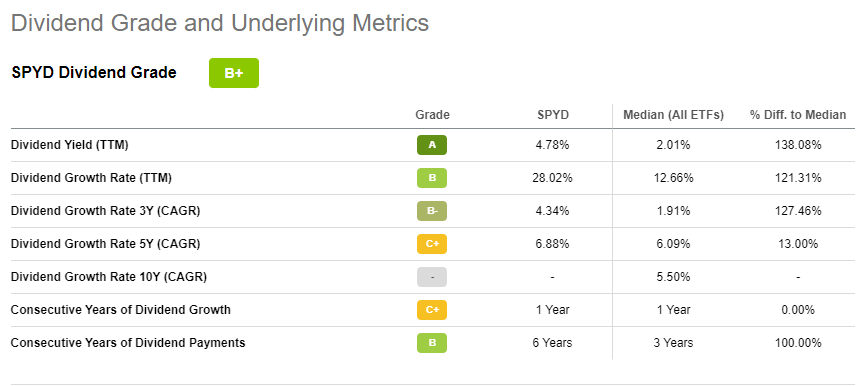

Above-Average Dividend Yield

SPYD focuses on S&P 500 stocks with above-average yields, which results in an above-average yield for the fund itself. SPYD currently yields 4.7%, but said yield includes an abnormally high dividend payment in early 2022. Disregarding said dividend payment, by annualizing the fund’s three most recent payments, I arrive at a dividend yield of 4.1%. SPYD also sports an SEC yield, a standardized measure of its short-term generation of income, of 4.1%. In my opinion, the latter figure is much more indicative of the dividends that investors should expect from the fund moving forward.

SPYD’s 4.1% forward yield is quite good, and higher than that of most broad-based U.S. equity index funds, and U.S. dividend equity index funds.

SPYD’s dividends have also seen reasonably good, albeit uneven, growth since inception.

SPYD

SPYD’s above-average yield and reasonable dividend growth track-record combine to create a good, steadily rising yield on cost for the fund’s investors. This is a benefit for all investors, and particularly impactful for long-term dividend growth investors.

SeekingAlpha

SPYD has an above-average dividend yield, a reasonable dividend growth track-record, and a steadily rising yield on cost. Although the fund does not excel in any dividend metric, all seem reasonably good, and all benefit the fund and its investors.

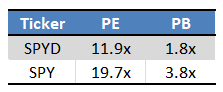

Cheap Valuation

SPYD focuses on S&P 500 stocks with above-average yields. As yields are something of a valuation metric, these stocks tend to trade with below-average valuations. SPYD itself current trades with a PE ratio of 11.9x, and a PB ratio of 1.8x. Both are reasonably low figures, and around half that of the S&P 500.

Fund Filings – Chart by Author

SPYD’s cheap valuation has led to strong, market-beating returns since early 2021, and counting.

SPYD’s cheap valuation could lead to further outperformance moving forward, but I don’t believe this to be all that likely. Let’s have a look as to why.

SPYD – Fairly Valued

Some context first.

Companies with strong growth prospects tend to focus on CAPEX and investments over distributing cash to shareholders, so their dividends tend to be low. These same companies tend to trade with premium share prices, due to strong investor demand and expectations of future growth, so their yields tend to be quite low.

Companies with weak growth prospects tend to focus on distributing excess cash to shareholders, as dividends or through buybacks, over CAPEX and other growth initiatives. These same companies tend to trade with relatively cheap valuations, due to weak investor demand on expectations of sluggish growth. Due to this, companies with weak growth prospects tend to have relatively high dividend yields.

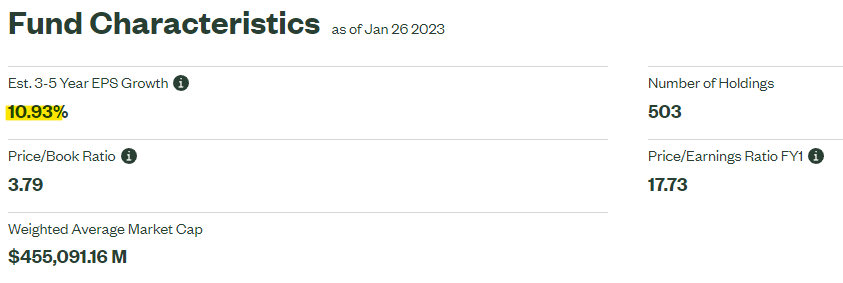

SPYD focuses on companies with above-average dividends yields which, considering the above, tend to have weak growth prospects. As per fund filings, SPYD’s underlying holdings have seen 3.6% in EPS growth these past few years, versus 10.9% for the S&P 500.

SPYD SPY

SPYD’s lower growth prospects means the fund should consistently trade with a cheap, below-average valuation. Due to this, a low PE and / or PB ratio does not necessarily mean that fund valuations are below fundamentals, or that the fund should see higher capital gains or returns moving forward. The fund should see said gains if its valuation were looking much cheaper than in the past, but that do not seem to be the case right now.

As per SeekingAlpha, SPYD trades with an average yield of 4.0%. Currently, the fund trades with a yield of 4.1%, excluding an abnormally large 1Q2022 dividend payment. Although the fund’s current yield is slightly higher than its historical average, the gap is quite small, and not terribly significant.

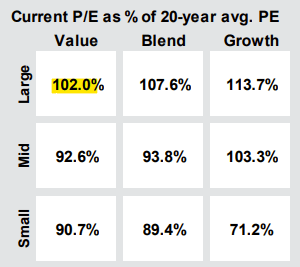

SPYD focuses on S&P 500 components with above-average yields, which can be characterized as large-cap value stocks (the fund does not explicitly target such stocks, but it does end up targeting them regardless). As per J.P. Morgan, large-cap value stocks are currently trading very slightly above their historical average valuations, slightly lower than large-cap stocks more broadly.

J.P. Morgan Guide to the Markets

From the above, it seems clear that SPYD is currently fairly valued, at least relative to the fund’s historically average valuations. One could argue for a very slight undervaluation on yield grounds, and relative to broader equity indexes, but the fund most certainly does not look significantly cheap right now. Under these conditions, I don’t believe that SPYD is likely to post significant, market-beating capital gains and total returns moving forward. Some gains are still quite likely, and the fund does sport a reasonably good yield, but the fund is not cheap enough for anything more than that.

Conclusion

SPYD’s diversified holdings and above-average, growing 4.1% dividend yield make the fund a buy. As the fund seems fairly valued relative to historical average, I do not expect significant outperformance moving forward.

Be the first to comment